Tag: Subsidy

-

Sedgwick County WATC funding trajectory following manager’s recommendations

Sedgwick County taxpayers have been generous with funding for Wichita Area Technical College, and the former county manager has recommended reducing its funding.

-

Cash incentives in Wichita

Wichita city leaders are proud to announce the end of cash incentives, but they were only a small portion of the total cost of incentives.

-

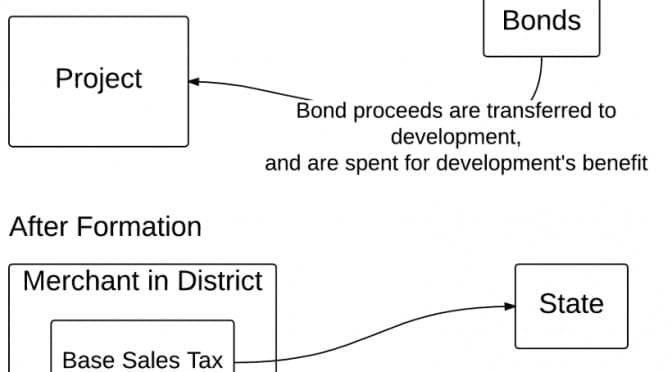

In Wichita, benefitting from your sales taxes, but not paying their own

A Wichita real estate development benefits from the sales taxes you pay, but doesn’t want to pay themselves.

-

Kansas senators vote to advance Ex-Im Bank

Kansas senators vote to advance Ex-Im Bank

-

Friedman: The fallacy of the welfare state

A simple classification of government spending shows why the process leads to undesirable results, explain Milton and Rose Friedman.

-

A big-picture look at the EDA

While praising the U.S. Economic Development Administration for a small grant to a local institution, the Wichita Eagle editorial board overlooks the big picture.

-

The candlemakers’ petition

The arguments presented in the following essay by Frederic Bastiat, written in 1845, are still in use in city halls, county courthouses, school district boardrooms, state capitals, and probably most prominently, Washington

-

Cash incentives in Wichita still in use

Wichita is moving away from the use of cash incentives for economic development, except for this.

-

With tax exemptions, what message does Wichita send to existing landlords?

As the City of Wichita prepares to grant special tax status to another new industrial building, existing landlords must be wondering why they struggle to stay in business when city hall sets up subsidized competitors with new buildings and a large cost advantage.

-

WichitaLiberty.TV: Arts funding, property taxes, uninformed officials, tax increment financing, and social security

Is Wichita risking a Soviet-style future? A look at Wichita property taxes, uninformed and misinformed elected officials, tax increment financing, and social security.

-

In Kansas and Wichita, there’s a reason for slow growth

If we in Kansas and Wichita wonder why our economic growth is slow and our economic development programs don’t seem to be producing results, there is data to tell us why: Our tax rates are too high.

-

Wichita city council member Jeff Longwell should not have voted

A sequence of events involving Jeff Longwell should concern citizens as they select the next Wichita mayor. Based on Wichita law, Longwell should not have voted on a matter involving the Ambassador Hotel, either for or against it.