Tag: Wichita city council

-

Wichita City Council June 2, 2026: Parking Ban Repealed

Wichita City Council June 2, 2026: the council repealed its 2008 backing-into-parking ban 7-0 (with an on-street exception), while two residents delivered pointed testimony alleging police accountability failures.

-

Wichita City Council May 12, 2026: Police Crash, Flock Cameras & Housing

A resident called for a police officer’s firing after a 100-mph crash injured four civilians. A privacy advocate documented gaps in Flock camera oversight. And the council unanimously approved a mixed-income housing bond that could bring 38 new homes to District IV.

-

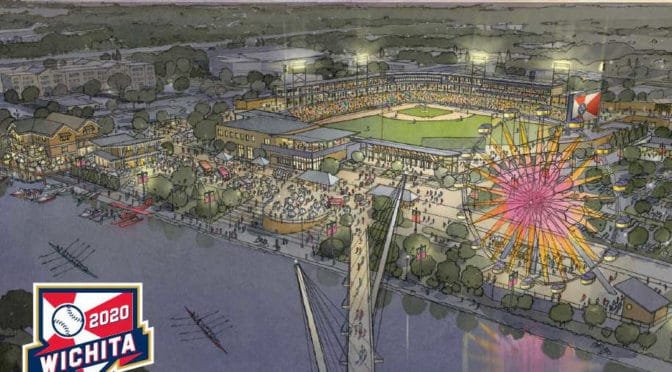

Wichita City Council May 5, 2026: STAR Bond, Baby Box & CDBG

The May 5 Wichita City Council session ran nearly seven hours — approving a $191.7M STAR Bond, a Safe Haven Baby Box, and a $5M first-responder wellness center, then spending two hours on a CDBG grant fight that overrode the council’s own Grant Review Committee.

-

Wichita City Council, April 28, 2026: Flock Camera Concerns, Affordable Home Sales, and Infrastructure Approvals

A citizen raised documented concerns about Flock Safety license-plate cameras at Wichita’s April 28 City Council meeting — citing weak authentication, uncertain data retention, and proven misuse by regional officers. The council also approved three affordable home sales and twelve infrastructure resolutions.

-

Wichita City Council Meeting — April 21, 2026: Transit Overhaul, Nomar Plaza Improvements, Flock Camera Debate, and a City Grappling With Public Safety

The Wichita City Council approved a comprehensive transit network redesign on April 21, 2026. The overhaul restructures bus routes to serve riders more efficiently while addressing equity gaps, second-shift worker access, and future downtown growth.

-

Wichita City Council April 14, 2026: Parking Garage Debate

The Wichita City Council’s April 14, 2026 meeting tackled some of the city’s most contested issues: a $9.6M parking garage purchase tied to the riverfront ballpark project, a revamped ethics ordinance, and new zoning notification rights for renters.

-

Wichita City Council April 7, 2026: Robot Dog Vote, Parking Garage Delay, Land Bank Dissolution

The April 7 Wichita City Council meeting ran nearly seven hours, producing a split 4-3 vote to purchase one SPOT robotic dog for WPD, a unanimous delay on the EPC downtown parking garage deal over contractual concerns, and a 4-3 vote to begin dissolving the Wichita Land Bank.

-

Wichita City Council, October 14, 2025: Transit Failures, Public Art Funding, and the Convention Center Gap

The Wichita City Council met October 14, 2025, approving infrastructure funding, a public art maintenance plan, and the Visit Wichita contract. Public speakers raised urgent concerns about transit failures and water privatization. All votes were unanimous at 7-0.

-

Wichita City Council October 21, 2025: Housing Reform Delayed, Rental Registry Rejected

Wichita City Council met for nearly ten hours on October 21, 2025, taking up a landmark housing and property maintenance reform package that drew 38 public speakers. The council unanimously referred the core code reform to a new task force but voted 4–3 to reject both a rental registry and a source-of-income nondiscrimination ordinance.

-

Wichita City Council Recap: October 28, 2025

The Wichita City Council met October 28, 2025, approving nine consent agenda items, a Board of Bids report, and airport electrical study contracts. The council also created a Property Maintenance Advisory Task Force and scheduled a special meeting on November 10 to review city manager candidates in executive session.

-

Wichita City Council November 6, 2025: Lodging Licenses, Foster Youth Housing, and Event Center Capacity

The Wichita City Council met November 6, 2025, passing a new lodging establishment license ordinance targeting problem motels on South Broadway, deferring a foster youth housing project using shipping containers, and approving a modified event center capacity amendment at 3207 East Douglas. Full coverage inside.

-

Wichita City Council March 24, 2026: Road Project $3.9M Over Budget, Board Appointments, and Civility Resolution Proposed

The Wichita City Council met March 24, 2026, debating a 143rd Street reconstruction project that came in $3.92 million over budget with only one bidder. The council approved it 5-2 over Mayor Wu’s objection, made dozens of civic board appointments, and discussed a proposed civility resolution. #ICT