Once embraced by Wichita officials as heroes, real estate listings for two floors of a downtown Wichita office building illustrate the carnage left behind by two developers.

A decade ago the “Minnesota Guys” were the darlings of downtown Wichita. With a controversial form of real estate ownership — tenancy in common — they promised to revive downtown Wichita. City officials and civic leaders praised them. The city council found them so endearing that it awarded the Minnesota Guys over $10 million in tax increment financing — later increased at their request — although the developers were never able to tap into those funds. Now the two developers are facing numerous felony charges relating to securities violations.

This week the Wichita Business Journalreports that two floors of a prominent downtown office building are for sale at very low prices. The building is Broadway Plaza at 105 S. Broadway.

In 2007 the fourth floor of this building had an appraised value of $388,000, according to Sedgwick County records. The value fell to $210,900 the next year and stayed at that value for five years. Now the appraised value is $98,000.

The value of the eleventh floor followed a similar trajectory, being valued at $399,000 in 2007, falling to $160,100 for four years, and now appraised at $82,300.

Now the asking price for each floor is $65,000. At attempt at sale at auction earlier this year failed to produce any bids. The asking price represents a cost of about $13 per square foot. That’s less than the annual rent for class A office space in Wichita, downtown and suburban.

In 2011 I reported on how some downtown Wichita properties are plummeting in value:

<

blockquote>A strategy of Real Development — the “Minnesota Guys” — in Wichita has been to develop and sell floors of downtown office buildings as condominiums. Some of these floors have been foreclosed upon and have come back on the market. Some once carried mortgages of $400,000 or more, meaning that at one point a bank thought they were worth at least that much. But now four floors in the Broadway Plaza Building, three floors of the Petroleum Building, two floors of Sutton Place, and one floor of the Orpheum Office Center are available for sale at prices not much over $100,000, ranging from $14 to $25 per square foot. Other downtown office buildings — very plain properties — are listed at much higher prices. For example, one downtown property is listed at $82 per square foot. … Some of these floors have had declining appraisals. According to the Sedgwick County Treasurer, the fifth floor of Sutton Place, which is listed for sale at $135,000, was appraised in 2008 for $530,900. In 2009 the appraised value dropped to $215,000.

The depreciation expense of Intrust Bank Arena in downtown Wichita recognizes and accounts for the sacrifices of the people of Sedgwick County and its visitors to pay for the arena. But no one wants to talk about this.

The true state of the finances of the Intrust Bank Arena in downtown Wichita are not often a subject of public discussion. Arena boosters promote a revenue-sharing arrangement between the county and the arena operator, referring to this as profit or loss. But this arrangement is not an accurate and complete accounting, and hides the true economics of the arena. What’s missing is depreciation expense.

In February the Wichita Eaglereported: “The arena’s net income for 2014 came in at $122,853, all of which will go to SMG, the company that operates the facility under contract with the county, Assistant County Manager Ron Holt said Wednesday.” A reading of the minutes for the February 11 meeting of the Sedgwick County Commission finds Holt mentioning depreciation expense not a single time. Strike one.

Last December, in a look at the first five years of the arena, its manager told the Wichita Eagle this: “‘We know from a financial standpoint, the building has been successful. Every year, it’s always been in the black, and there are a lot of buildings that don’t have that, so it’s a great achievement,’ said A.J. Boleski, the arena’s general manager.” Strike two.

I didn’t notice the Eagle opinion page editorializing this year on the release of the arena’s profitability figures. So here’s an example of incomplete editorializing from Rhonda Holman, who opined “Though great news for taxpayers, that oversize check for $255,678 presented to Sedgwick County last week reflected Intrust Bank Arena’s past, specifically the county’s share of 2013 profits.” (Earlier reporting on this topic in the Eagle in 2013 did not mention depreciation expense, either.) Strike three in the search for truthful accounting of the arena’s finances.

The problem with the reporting of Intrust Bank Arena profits

There are at least two ways of looking at the finance of the arena. Most attention is given to the “profit” (or loss) earned by the arena for the county according to an operating and management agreement between the county and SMG, a company that operates the arena.

This agreement specifies a revenue sharing mechanism between the county and SMG. For 2103, the accounting method used in this agreement produced a profit of $705,678, to be split (not equally) between SMG and the county. The county’s share, as Holman touted in her Eagle op-ed, was $255,678. (Presumably that’s after deducting the cost of producing an oversize check for the television cameras.)

For 2014, the arena’s profit was $122,853. All that goes to SMG, based on the revenue-sharing agreement.

While described as “profit” by many, this payment does not represent any sort of “profit” or “earnings” in the usual sense. In fact, the introductory letter that accompanies these calculations warns readers that these are “not intended to be a complete presentation of INTRUST Bank Arena’s financial position and results of operations and are not intended to be a presentation in conformity with accounting principles generally accepted in the United States of America.”

That bears repeating: This is not a reckoning of profit and loss in any recognized sense. It is simply an agreement between Sedgwick County and SMG as to how SMG is to be paid, and how the county participates.

A much better reckoning of the economics of the Intrust Bank Arena can be found in the 2014 Comprehensive Annual Financial Report for Sedgwick County. This document holds additional information about the finances of the Intrust Bank Arena. The CAFR, as described by the county, “… is a review of what occurred financially last year. In that respect, it is a report card of our ability to manage our financial resources.”

Regarding the arena, the CAFR states:

The Arena Fund represents the activity of the INTRUST Bank Arena. The facility is operated by a private company; the county incurs expenses only for certain capital improvements or major repairs and depreciation, and receives as revenue only a share of profits earned by the operator, if any, and naming rights fees. The Arena had an operating loss of $5.0 million. The loss can be attributed to $5.2 million in depreciation expense.

Financial statements in the same document show that $5,157,424 was charged for depreciation in 2014, bringing accumulated depreciation to a total of $26,347,705.

Depreciation expense is not something that is paid out in cash. Sedgwick County didn’t write a check for $5,157,424 to pay depreciation expense. Instead, depreciation accounting provides a way to recognize and account for the cost of long-lived assets over their lifespan. It provides a way to recognize opportunity costs, that is, what could be done with our resources if not spent on the arena.

But not many of our public leaders recognize this. In years past, Commissioner Dave Unruh made remarks that show the severe misunderstanding that he and almost everyone labor under regarding the nature of the spending on the arena: “I want to underscore the fact that the citizens of Sedgwick County voted to pay for this facility in advance. And so not having debt service on it is just a huge benefit to our government and to the citizens, so we can go forward without having to having to worry about making those payments and still show positive cash flow. So it’s still a great benefit to our community and I’m still pleased with this report.”

Earlier in this article we saw examples of the Sedgwick County Assistant Manager, the Intrust Bank Arena manager, and several Wichita Eagle writers making the same mistake.

Intrust Bank Arena commemorative monumentThe contention — witting or not — of all these people is that the capital investment of $183,625,241 (not including an operating and maintenance reserve) in the arena is merely a historical artifact, something that happened in the past, something that has no bearing today. There is no opportunity cost, according to this view. This attitude, however, disrespects the sacrifices of the people of Sedgwick County and its visitors to raise those funds. Since Kansas is one of the few states that adds sales tax to food, low-income households paid extra sales tax on their groceries to pay for the arena — an arena where they may not be able to afford tickets.

Any honest accounting or reckoning of the performance of Intrust Bank Arena must take depreciation into account. While Unruh is correct that depreciation expense is not a cash expense that affects cash flow, it is an economic fact that can’t be ignored — except by politicians, apparently. The Wichita Eagle aids in promoting this deception.

We see our governmental and civic leaders telling us that we must “run government like a business.” Without frank and realistic discussion of numbers like these and the economic facts they represent, we make decisions based on incomplete and false information.

Despite a policy change, the Wichita city council still votes for no-bid contracts paid for with taxpayer funds.

In the current campaign for Wichita mayor, one candidates says he never has voted for no-bid contracts: “[Longwell] also takes issue with the claim he has ever voted for any no-bid contract, something he says his voting record will back up. ‘That’s the beauty of having a voting record,’ he says.” Mayoral candidate Williams decries ‘crony capitalism’ of critics, Wichita Business Journal, March 12, 2015

We don’t have to look very hard to find an example that contradicts Longwell’s claim of never voting for a no-bid contract. Minutes from the August 9, 2011 meeting of the city council show that there was discussion about the no-bid contract for the garage benefiting the Ambassador Hotel. Then-council member Michael O’Donnell questioned if the city was getting the best deal for taxpayers, since the garage was to be built with public funds. O’Donnell was told that the no-bid contract was at “the developer’s request.” These developers include principals and executives of Key Construction and Dave Burk, all who have been generous and consistent funders of Longwell’s campaigns.

But we don’t have to go back that far to find voting for no-bid contracts paid for with taxpayer funds. Longwell has voted several times in favor of the Exchange Place project, starting when it was a project of the Minnesota Guys. The latest such vote was on March 3, 2015, when Longwell voted in favor of a project that contained this benefit, according to city documents: “The City will also provide TIF funding in an amount not to exceed $12,500,000 for the acquisition of land and construction of the parking structure.”

This garage, to be paid for through public funds, was not competitively bid. Despite the garage being pitched as a public good, most parking spaces are for the exclusive benefit of Exchange Place.

Impetus for change

The votes by Longwell and others for no-bid contracts sparked the city manager to ask for a change in policy. The Wichita Eagle reported in 2012:

The days of awarding construction projects without taking competitive bids might be numbered at City Hall if City Manager Robert Layton has his way, especially with public projects such as parking garages that are part of private commercial development.

Layton said last week that he intends to ask the City Council for a policy change against those no-bid contracts.

Three years later, Longwell and others are still voting to spend taxpayer funds on no-bid contracts.

— Minutes from August 8, 2011 meeting

Council Member O’Donnell stated and we will not being going out to bid to find the best

deal on that and are just awarding.

Allen Bell Urban Development Director stated that is the developer’s request. Council Member O’Donnell asked if that is City precedent and that with a government project in the tune of $6 million dollars, does not have to be sent out for bid?

Gary Rebenstorf Director of Law stated we have Charter Ordinance No. 203 that has been adopted by the City Council, which provides a procedure to exempt these types of projects from the bidding requirements from the City and has to meet certain requirements in order for it to be used by the Council. Stated the most significant is that there has to be a public hearing and has to be a 2/3 vote by the Council to approve this development agreement that sets up this type of project.

Council Member O’Donnell stated he is glad the media is here to pick up on that because he thinks that $6 million dollars is a lot of money and to just award that to a contractor that has special ties to campaign finance reports of everyone on the City Council except himself, seems questionable.

Based on events in Wichita, the Wall Street Journal wrote “What Americans seem to want most from government these days is equal treatment. They increasingly realize that powerful government nearly always helps the powerful …” But Wichita’s elites don’t seem to understand this.

Three years ago from today the Wall Street Journal noted something it thought remarkable: a “voter revolt” in Wichita. Citizens overturned a decision by the Wichita City Council regarding an economic development incentive awarded to a downtown hotel. It was the ninth layer of subsidy for the hotel, and because of our laws, it was the only subsidy that citizens could contest through a referendum process.

In its op-ed, the Journal wrote:

The elites are stunned, but they shouldn’t be. The core issue is fairness — and not of the soak-the-rich kind that President Obama practices. One of the leaders of the opposition, Derrick Sontag, director of Americans for Prosperity in Kansas, says that what infuriated voters was the veneer of “political cronyism.”

What Americans seem to want most from government these days is equal treatment. They increasingly realize that powerful government nearly always helps the powerful, whether the beneficiaries are a union that can carve a sweet deal as part of an auto bailout or corporations that can hire lobbyists to write a tax loophole.

The “elites” referred to include the Wichita Metro Chamber of Commerce, the political class, and the city newspaper. Since then, the influence of these elites has declined. Last year all three campaigned for a sales tax increase in Wichita, but voters rejected it by a large margin. It seems that voters are increasingly aware of the cronyism of the elites and the harm it causes the Wichita-area economy.

Last year as part of the campaign for the higher sales tax the Wichita Chamber admitted that Wichita lags in job creation. The other elites agreed. But none took responsibility for having managed the Wichita economy into the dumpster. Even today the local economic development agency — which is a subsidiary of the Wichita Chamber — seeks to shift blame instead of realizing the need for reform. The city council still layers on the levels of subsidy for its cronies.

Following, from March 2012:

A Wichita shocker

“Local politicians like to get in bed with local business, and taxpayers are usually the losers. So three cheers for a voter revolt in Wichita, Kansas last week that shows such sweetheart deals can be defeated.” So starts today’s Wall Street Journal Review & Outlook editorial (subscription required), taking notice of the special election last week in Wichita.

The editorial page of the Wall Street Journal is one of the most prominent voices for free markets and limited government in America. Over and over Journal editors expose crony capitalism and corporate welfare schemes, and they waste few words in condemning these harmful practices.

The three Republican members of the Wichita City Council who consider themselves fiscal conservatives but nonetheless voted for the corporate welfare that voters rejected — Pete Meitzner (district 2, east Wichita), James Clendenin (district 3, southeast and south Wichita), and Jeff Longwell (district 5, west and northwest Wichita) — need to consider this a wake up call. These members, it should be noted, routinely vote in concert with the Democrats and liberals on the council.

For good measure, we should note that Sedgwick County Commission Republicans Dave Unruh and Jim Skelton routinely — but not always — vote for these crony capitalist measures.

Hopefully this election will convince Wichita’s political and bureaucratic leaders that our economic development policies are not working. Combined with the startling findings by a Tax Foundation and KMPG study that finds Kansas lags near the bottom of the states in tax costs to business, the need for reform of our spending and taxing practices couldn’t be more evident. It is now up to our leaders to find within themselves the capability to change — or we all shall suffer.

In this episode of WichitaLiberty.TV: We’ll examine the city council’s action regarding a downtown Wichita development project and how it is harmful to Wichita taxpayers and the economy. View below, or click here to view at YouTube. Episode 77, broadcast March 8, 2015.

A problem with wasteful spending in downtown Wichita is gradually curing itself, creating another problem in its place.

A bench at the heart of downtown Wichita should be illuminated at night by four lights. Only one light works, probably because the others have been left switched on 24 hours per day.

So wasteful spending on street lights during the day is being replaced by unlit streets at night.

What message does wasteful spending on street lights during the day send?

it’s difficult to show three nonfunctioning lights next to one that works, I’m afraid.Perhaps more importantly, what impression does nonfunctioning lights at night create — three of four at this bench? And at one of our major downtown intersections? Across the street from our nice boutique hotel?

Is this the “walkable” downtown we’re trying to create?

I suppose that Wichita city leaders want to be seen taking care of our larger problems, and of those, we have a few. But this long-running problem with lights at this downtown street side bench needs to be taken care of soon. Visitors to our town may not be aware of the lofty and sweeping rhetoric of our mayor, bureaucrats, and civic leaders.

An incentives agreement the Wichita city council passed on first reading is missing several items that city policy requires. How the council and city staff handle the second reading of this ordinance will let us know for whose interests city hall works: citizens, or cronies.

My presentation centered on the lack of an agreement by the developer to forgo appeals of the tax valuation of the property. The applicant had done this in the past, and it caused a shortfall of TIF revenue that the city had to makeup. The city manager had said that taxpayers would be protected in future deals, but the city did not include this protection in the Mosely agreement.

The omission of this taxpayer protection was not all that was missing. The Downtown Development Incentives Policy, revised by the council on June 10, 2014, calls for several items to be supplied when seeking incentives, including tax increment financing, which was the incentive requested for the Mosely project. As I show below, many significant items related to taxpayer protection were missing.

The council approved the project on first reading, noting that the development agreement would be finalized in time for second reading.

This is insufficient. The second reading of an ordinance is usually handled as part of the consent agenda. This is a grouping of items that are voted on as a group, in bulk. There is no discussion unless a council member specifically requests. The practice of the city is that the text of the ordinances on second reading is not made available in the agenda packet, even though changes may have been made between first reading and second reading. That will certainly be the case with this ordinance, as many things are missing from the development agreement.

It’s not clear why there is a first reading and a second reading of an ordinance. It may be so that details may be corrected. Or, perhaps council members would like to have a chance to reconsider their first vote. City code seems to give no guidance as to how much change to an ordinance is allowable between first and second reading.

The problem we face in Wichita is that the approval of a development plan in a TIF district has a mandated public hearing. It is not optional. But the motion passed by the council this week closed the public hearing. Yet, the city will need to make substantial changes to the ordinance and development agreement if it intends to follow the downtown incentives policy that it created. But the public will have no chance to comment on the new material. If past city practice is followed, the new material will not be made available to the public, and perhaps not to council members.

This is a conflict that I do not believe can be resolved unless the city reopens the public hearing for consideration of the revised ordinance and developer agreement on first reading. Anything else disrespects procedures that are designed to benefit and protect the public.

Except. As with many city council policies, there are loopholes. As outlined below, the council can simply vote to waive the requirements of the downtown incentives policy. That gives the council an easy out. But that makes another mockery of the city’s policies, if the council waives them whenever they are inconvenient.

When I presented the defect in the development agreement to the council I asked: Is this lack of taxpayer protection an oversight, or is it by design? There was no answer.

I did not ask this question, but didn’t any city council member notice the omission of significant items needed to comply with its own policies? What about the city manager? Economic development director? City attorney?

Section D of the incentives policy states “parties requesting Downtown Development Incentives must submit the information listed below.” Significant missing items included the following:

CEDBR Fiscal Impact Model

The idea behind the city’s use of economic development incentives is that the city receives more than it spends or forgoes in future tax revenue. An analysis performed by the Center for Economic Development and Business Research (CEDBR) at Wichita State University is used to make this decision. This appears to have not been done for this project.

Guarantee for a proportional share of public revenue shortfall

This was not present in the developer agreement.

Economic analysis confirms that the project is infeasible “but for” public investment

This was not present in the developer agreement.

Minimum private to public capital investment ratio of 2 to 1

Information necessary to make this judgment was not included in the agenda presentation.

Pro Forma

The incentives policy states: “Pro Forma — The project pro forma will be evaluated on the following criteria:

a. Rate of private investment return

b. Rents/prices consistent with performance of comparables

c. Projected rate of absorption consistent with performance of comparables

d. Long-term project solvency”

It appears that this analysis was not performed.

“Gap” Financing Requirement

The downtown incentives policy states: “Approval of Downtown Development Incentives will require a financial analysis demonstrating that the project would not otherwise be possible without the use of the requested development incentive (“gap” analysis). Parties requesting Downtown Development Incentives will be required to provide the City pro forma cash flow analyses and sources and uses of funds in sufficient detail to demonstrate that reasonably available conventional debt and equity financing sources are not available to fund the entire cost of the project and still provide the developer a reasonable market rate of return on investment.”

There is no evidence that this analysis was performed and made available to the council.

Waiver

The incentives policy contains a loophole. If the council believes it is “inappropriate to evaluate a particular request for Downtown Development Incentives” using the policy, it may vote to waive the requirements.

Tax increment financing disrupts the usual flow of tax dollars, routing funds away from cash-strapped cities, counties, and schools back to the TIF-financed development. TIF creates distortions in the way cities develop, and researchers find that the use of TIF means lower economic growth.

The consideration this week by the Wichita City Council of two project plans in tax increment financing districts offers an opportunity to examine the issues surrounding TIF.

How TIF works

A TIF district is a geographically-defined area.

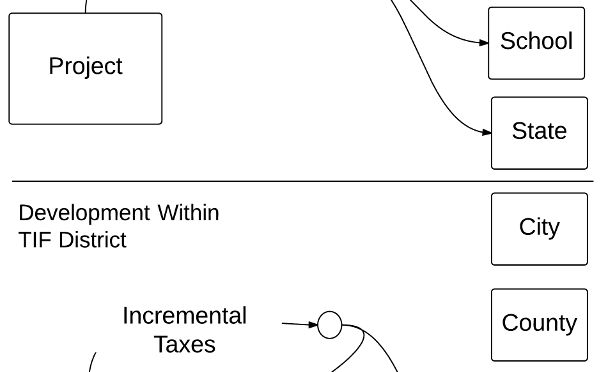

In Kansas, TIF takes two or more steps. The first step is that cities or counties establish the boundaries of the TIF district. After the TIF district is defined, cities then must approve one or more project plans that authorize the spending of TIF funds in specific ways. (The project plan is also called a redevelopment plan.) In Kansas, overlapping counties and school districts have an opportunity to veto the formation of the TIF district, but this rarely happens. Once the district is formed, cities and counties have no ability to object to TIF project plans.

Figure 1.Before the formation of the TIF district, the property pays taxes to the city, county, school district, and state as can be seen in figure 1. Because property considered for TIF is purportedly blighted, the amount of tax paid is usually small. Whatever it is, that level is called the “base.”

Figure 2.After approval of one or more TIF project plans the city borrows money and gives it to the project or development. The city now has additional debt in the form of TIF bonds that require annual payments. Figure 2 illustrates. (There is now another form of TIF known as “pay-as-you-go” that works differently, but produces much the same economic effect.)

Figure 3.Figure 3 shows the flow of tax revenue after the formation of the TIF district and after the completion of a project. Because buildings were built or renovated, the property is worth more, and the property tax is now higher. The development now has two streams of property tax payments that are handled in different ways. The original tax — the “base” — is handled just like before, distributed to city, state, school district, and the state, according to their mill levy rates. The difference between the new tax and the base tax — the “increment” — is handled differently. It goes to only two destinations (mostly): The State of Kansas, and repayment of the TIF bonds.

Figure 4.Figure 4 highlights the difference in the flow of tax revenues. The top portion of the illustration shows development outside of TIF. We see the flows of tax payments to city, county, school district, and the state. In the bottom portion, which shows development under TIF, the tax flows to city, county, and school district are missing. No longer does a property contribute to the support of these three units of government, although the property undoubtedly requires the services of them. This is especially true for a property in Old Town, which consumes large amounts of policing.

(Cities, counties, and school districts still receive the base tax payments, but these are usually small, much smaller than the incremental taxes. In non-TIF development, these agencies still receive the base taxes too, plus whatever taxes result from improvement of the property — the “increment,” so to speak. Or simply, all taxes.)

The Kansas law governing TIF, or redevelopment districts as they are also called, starts at K.S.A. 12-1770.

TIF and public policy

Originally most states included a “but for” test that TIF districts must meet. That is, the proposed development could not happen but for the benefits of TIF. Many states have dropped this requirement. At any rate, developers can always present proposals that show financial necessity for subsidy, and gullible government officials will believe.

Similarly, TIF was originally promoted as a way to cure blight. But cities are so creative and expansive in their interpretation of blight that this requirement, if it still exists, has little meaning.

The rerouting of property taxes under TIF goes against the grain of the way taxes are usually rationalized. We use taxation as a way to pay for services that everyone benefits from, and from which we can’t exclude people. An example would be police protection. Everyone benefits from being safe, and we can’t exclude people from benefiting from police protection.

So when we pay property tax — or any tax, for that matter — people may be comforted knowing that it goes towards police and fire protection, street lights, schools, and the like. (Of course, some is wasted, and government is not the only way these services, especially education, could be provided.)

But TIF is contrary to this justification of taxes. TIF allows property taxes to be used for one person’s (or group of persons) exclusive benefit. This violates the principle of broad-based taxation to pay for an array of services for everyone. Remember: What was the purpose of the TIF bonds? To pay for things that benefited the development. Now, the development’s property taxes are being used to repay those bonds instead of funding government.

One more thing: Defenders of TIF will say that the developers will pay all their property taxes. This is true, but only on a superficial level. We now see that the lion’s share of the property taxes paid by TIF developers are routed back to them for their own benefit.

It’s only infrastructure

In their justification of TIF in general, or specific projects, proponents may say that TIF dollars are spent only on allowable purposes. Usually a prominent portion of TIF dollars are spent on infrastructure. This allows TIF proponents to say the money isn’t really being spent for the benefit of a specific project. It’s spent on infrastructure, they say, which they contend is something that benefits everyone, not one project specifically. Therefore, everyone ought to pay.

This attitude is represented by a comment left at Voice for Liberty, which contended: “The thing is that real estate developers do not invest in public streets, sidewalks and lamp posts, because there would be no incentive to do so. Why spend millions of dollars redoing or constructing public streets when you can not get a return on investment for that”

This perception is common: that when we see developers building something, the City of Wichita builds the supporting infrastructure at no cost to the developers. But it isn’t quite so. About a decade ago a project was being developed on the east side of Wichita, the Waterfront. This project was built on vacant land. Here’s what I found when I searched for City of Wichita resolutions concerning this project:

Figure 5. Waterfront resolutions.Note specifically one item: $1,672,000 for the construction of Waterfront Parkway. To anyone driving or walking in this area, they would think this is just another city street — although a very nicely designed and landscaped street. But the city did not pay for this street. Private developers paid for this infrastructure. Other resolutions resulted in the same developers paying for street lights, traffic signals, sewers, water pipes, and turning lanes on major city streets. All this is infrastructure that we’re told real estate developers will not pay for. But in order to build the Waterfront development, private developers did, with a total cost of these projects being $3,334,500. (It’s likely I did not find all the resolutions and costs pertaining to this project, and more development has happened since this research.)

In a TIF district, these things are called “infrastructure” and will be paid for by the development’s own property taxes — taxes that must be paid in any case. Outside of TIF districts, developers pay for these things themselves.

If not for TIF, nothing will happen here

Generally, TIF is justified using the “but-for” argument. That is, nothing will happen within a district unless the subsidy of TIF is used. Paul F. Byrne explains:

“The but-for provision refers to the statutory requirement that an incentive cannot be awarded unless the supported economic activity would not occur but for the incentive being offered. This provision has economic importance because if a firm would locate in a particular jurisdiction with or without receiving the economic incentive, then the economic impact of offering the incentive is non-existent. … The but-for provision represents the legislature’s attempt at preventing a local jurisdiction from awarding more than the minimum incentive necessary to induce a firm to locate within the jurisdiction. However, while a firm receiving the incentive is well aware of the minimum incentive necessary, the municipality is not.”

“This paper conducts a comprehensive assessment of the effectiveness of Chicago’s TIF program in creating economic opportunities and catalyzing real estate investments at the neighborhood scale. This paper uses a unique panel dataset at the block group level to analyze the impact of TIF designation and investments on employment change, business creation, and building permit activity. After controlling for potential selection bias in TIF assignment, this paper shows that TIF ultimately fails the ‘but-for’ test and shows no evidence of increasing tangible economic development benefits for local residents.” (emphasis added)

In the paper, the author clarifies:

“To clarify these findings, this analysis does not indicate that no building activity or job crea-tion occurred in TIFed block groups, or resulted from TIF projects. Rather, the level of these activities was no faster than similar areas of the city which did not receive TIF assistance. It is in this aspect of the research design that we are able to conclude that the development seen in and around Chicago’s TIF districts would have likely occurred without the TIF subsidy. In other words, on the whole, Chicago’s TIF program fails the ‘but-for’ test.

Later on, for emphasis:

“While the findings of this paper are clear and decisive, it is important to comment here on their exact extent and external validity, and to discuss the limitations of this analysis. First, the findings do not indicate that overall employment growth in the City of Chicago was negative or flat during this period. Nor does this research design enable us to claim that any given TIF-funded project did not end up creating jobs. Rather, we conclude that on-average, across the whole city, TIF was unsuccessful in jumpstarting economic development activity — relative to what would have likely occurred otherwise.” (emphasis in original)

The author notes that these conclusions are specific to Chicago’s use of TIF, but should “should serve as a cautionary tale.”

The paper reinforces the problem of using tax revenue for private purposes, rather than for public benefit: “Essentially, Chicago’s extensive use of TIF can be interpreted as the siphoning off of public revenue for largely private-sector purposes. Although, TIF proponents argue that the public receives enhanced economic opportunity in the bargain, the findings of this paper show that the bargain is in fact no bargain at all.”

TIF is social engineering

TIF represents social engineering. By using it, city government has decided that it knows best where development should be directed. In particular, the Wichita city council has decided that Old Town and downtown development is on a superior moral plane to other development. Therefore, we all have to pay higher taxes to support this development. What is the basis for saying Old Town developers don’t have to pay for their infrastructure, but developers in other parts of the city must pay?

TIF doesn’t work

Does TIF work? It depends on what the meaning of “work” is.

If by working, do we mean does TIF induce development? If so, then TIF usually works. When the city authorizes a TIF project plan, something usually gets built or renovated. But this definition of “works” must be tempered by a few considerations.

Does TIF pay for itself?

First, is the project self-sustaining? That is, is the incremental property tax revenue sufficient to repay the TIF bonds? This has not been the case with all TIF projects in Wichita. The city has had to bail out two TIFs, one with a no-interest and low-interest loan that cost city taxpayers an estimated $1.2 million.

The verge of corruption

Second, does the use of TIF promote a civil society, or does it lead to cronyism? Randal O’Toole has written:

“TIF puts city officials on the verge of corruption, favoring some developers and property owners over others. TIF creates what economists call a moral hazard for developers. If you are a developer and your competitors are getting subsidies, you may simply fold your hands and wait until someone offers you a subsidy before you make any investments in new development. In many cities, TIF is a major source of government corruption, as city leaders hand tax dollars over to developers who then make campaign contributions to re-elect those leaders.”

We see this in Wichita, where the regular recipients of TIF benefits are also regular contributors to the political campaigns of those who are in a position to give them benefits. The corruption is not illegal, but it is real and harmful, and calls out for reform. See In Wichita, the need for campaign finance reform.

The effect of TIF on everyone

Third, what about the effect of TIF on everyone, that is, the entire city or region? Economists have studied this matter, and have concluded that in most cases, the effect is negative.

“TIF districts grow much faster than other areas in their host municipalities. TIF boosters or naive analysts might point to this as evidence of the success of tax increment financing, but they would be wrong. Observing high growth in an area targeted for development is unremarkable.”

So TIF districts are good for the favored development that receives the subsidy — not a surprising finding. What about the rest of the city? Continuing from the same study:

“If the use of tax increment financing stimulates economic development, there should be a positive relationship between TIF adoption and overall growth in municipalities. This did not occur. If, on the other hand, TIF merely moves capital around within a municipality, there should be no relationship between TIF adoption and growth. What we find, however, is a negative relationship. Municipalities that use TIF do worse.

We find evidence that the non-TIF areas of municipalities that use TIF grow no more rapidly, and perhaps more slowly, than similar municipalities that do not use TIF.” (emphasis added)

In a different paper (The Effects of Tax Increment Financing on Economic Development), the same economists wrote “We find clear and consistent evidence that municipalities that adopt TIF grow more slowly after adoption than those that do not. … These findings suggest that TIF trades off higher growth in the TIF district for lower growth elsewhere. This hypothesis is bolstered by other empirical findings.” (emphasis added)

“This article addresses the claim by examining the impact of TIF adoption on municipal employment growth in Illinois, looking for both general impact and impact specific to the type of development supported. Results find no general impact of TIF use on employment. However, findings suggest that TIF districts supporting industrial development may have a positive effect on municipal employment, whereas TIF districts supporting retail development have a negative effect on municipal employment. These results are consistent with industrial TIF districts capturing employment that would have otherwise occurred outside of the adopting municipality and retail TIF districts shifting employment within the municipality to more labor-efficient retailers within the TIF district.” (emphasis added)

These studies and others show that as a strategy for increasing the overall wellbeing of a city, TIF fails to deliver prosperity, and in fact, causes harm.

In this episode of WichitaLiberty.TV: While chair of the Wichita Metro Chamber of Commerce, a Wichita business leader strikes a deal that’s costly for taxpayers. A Kansas University faculty member is under attack from groups that don’t like his politics. Then, how can classical liberalism help us all get along with each other? View below, or click here to view at YouTube. Episode 68, broadcast December 14, 2014.

A decade ago the “Minnesota Guys” were the darlings of downtown Wichita. With a controversial form of real estate ownership — tenancy in common — they promised to revive downtown Wichita. City officials and civic leaders praised them. The city council found them so endearing that it awarded the Minnesota Guys over $10 million in tax increment financing — later increased at their request — although the developers were never able to tap into those funds. Now the two developers are facing numerous felony charges relating to securities violations.

A decade ago the “Minnesota Guys” were the darlings of downtown Wichita. With a controversial form of real estate ownership — tenancy in common — they promised to revive downtown Wichita. City officials and civic leaders praised them. The city council found them so endearing that it awarded the Minnesota Guys over $10 million in tax increment financing — later increased at their request — although the developers were never able to tap into those funds. Now the two developers are facing numerous felony charges relating to securities violations.

Three years ago from today the Wall Street Journal noted something it thought remarkable: a “voter revolt” in Wichita. Citizens overturned a decision by the

Three years ago from today the Wall Street Journal noted something it thought remarkable: a “voter revolt” in Wichita. Citizens overturned a decision by the