In this excerpt from WichitaLiberty.TV: Analysis of household expenditure data shows that a proposed sales tax in Wichita affects low income families in greatest proportion, confirming the regressive nature of sales taxes. View below, or click here to view on YouTube. For more on this, see Wichita sales tax hike would hit low income families hardest.

Wichita city council member Lavonta Williams (district 1, northeast Wichita) is a supporter of the proposed one cent per dollar Wichita sales tax. She has also spoken of her concern for Wichita’s low-income families, as she did in November 2013 when the Wichita City Council voted to increase water rates. City documents indicated that the average residential bill would rise by $1.33 per month for those who use modest amounts of water.

Wichita City Council Member Lavonta WilliamsAccording to the meeting minutes, Williams said this:

Council Member Williams stated she realizes that some may think that $1.33 is not that big of an increase, but for so many of our constituents, it is quite an increase for them especially those who are on a fixed income. Stated this is concerning to her and appreciates staff looking at all options and are kicking off a program that will help those who need assistance from the City. Stated she realizes as a City that we have to continue moving forward and look at our infrastructure.

I wonder: When Williams voted in favor of the Wichita sales tax ballot placement, did she understand that anyone who spends $133.00 per month on taxable purchases will see a $1.33 rise in their monthly sales tax expense? Recall that Kansas applies sales tax to food, although there is a possibility of receiving a rebate. The rebate is implemented through a nonrefundable income tax credit.

Here’s something else: Since Williams applauded the formation of a payment assistance program for those who can’t afford their water bills, I wonder if she will propose a similar program for those who can’t afford a higher sales tax?

Supporters of a proposed sales tax in Wichita promise there will be no conflicts of interest when making spending decisions. That would be a welcome departure from present city practice.

“Yes Wichita” website.In November Wichita voters will decide on a new one cent per dollar sales tax, part to be used for economic development, specifically job creation. “Yes Wichita” is a group that supports the sales tax. Language on its website reads: “Conflict-of-interest policies will prohibit anyone from participating in decisions in which there is any self-interest.” The page is addressing the economic development portion of the proposed sales tax. It’s part of an effort to persuade Wichita voters that millions in incentives will be granted based on merit instead of cronyism or the self-interest of politicians, bureaucrats, and committee members.

The problem is that while the city currently has in place laws regarding conflicts of interest, the city does not seem willing to observe them. If the proposed sales tax passes, what assurances do we have that the city will change its ways?

Following, from October 2013, is one illustration of Wichita city hall’s attitude towards conflicts of interest and more broadly, government ethics.

Wichita contracts, their meaning (or not)

Is the City of Wichita concerned that its contracts contain language that seems to be violated even before the contract is signed?

No member of the City’s governing body or of any branch of the City’s government that has any power of review or approval of any of the Developer’s undertakings shall participate in any decisions relating thereto which affect such person’s personal interest or the interests of any corporation or partnership in which such person is directly or indirectly interested.

At Tuesday’s meeting I read this section of the contract to the council. I believe it is relevant for these reasons:

Wichita Mayor Carl Brewer is a member of a governing body that has power of approval over this project.

Bill Warren is one of the parties that owns this project.

Bill Warren also owns movie theaters.

Wichita Mayor Carl Brewer owns a company that manufactures barbeque sauce.

Brewer’s sauce is sold at Warren’s theaters.

The question is this: Does the mayor’s business relationship with Warren fall under the prohibitions described in the language of section 11.06? Evidently not. After I read section 11.06 I asked the mayor if he sold his sauce at Warren’s theaters. He answered yes. But no one — not any of the six city council members, not the city manager, not the city attorney, not any bureaucrat — thought my question was worthy of discussion.

(While the agreement doesn’t mention campaign contributions, I might remind the people of Wichita that during 2012, parties to this agreement and their surrogates provided all the campaign finance contributions that council members Lavonta Williams and James Clendenin received. See Campaign contributions show need for reform in Wichita. That’s a lot of personal interest in the careers of politicians.)

I recommend that if we are not willing to live up to this section of the contract that we strike it. Why have language in contracts that we ignore? Parties to the contract rationalize that if the city isn’t concerned about enforcing this section, why should they have to adhere to other sections?

While we’re at it, we might also consider striking Section 2.04.050 of the city code, titled “Code of ethics for council members.” This says, in part, “[Council members] shall refrain from making decisions involving business associates, customers, clients, friends and competitors.”

That language seems pretty clear to me. But we have a city attorney that says that this is simply advisory. If the city attorney’s interpretation of this law is controlling, I suggest we strike this section from the city code. Someone who reads this — perhaps a business owner considering Wichita for expansion — might conclude that our city has a code of ethics that is actually observed by the mayor and council members and enforced by its attorneys.

Claims by boosters of a proposed Wichita sales tax that the city will be transparent in how money is spent must be examined in light of the city’s attitude towards citizens’ right to know.

When a city council member apologizes to bureaucrats because they have to defend why their agencies won’t disclose how taxpayer money is spent, we have a problem. When the mayor and most other council members agree, the problem is compounded. Carl Brewer won’t be mayor past April, but the city council member that apologized to bureaucrats — Pete Meitzner (district 2, east Wichita) — may continue serving in city government beyond next year’s elections. Wichita City Manager Robert Layton will likely continue serving for the foreseeable future.

Why is this important? Supporters of the proposed Wichita sales tax promise transparency in operations and spending. But requests for spending records by the city’s quasi-governmental agencies are routinely rebuffed. The city supports their refusal to comply with the Kansas Open Records Act. Many of the people presently in charge at city hall and at agencies like Greater Wichita Economic Development Coalition will still be in charge if the proposed sales tax passes. What assurances do we have that they will change their attitude towards citizens’ right to know how taxpayer funds are spent?

Following, from December 2012, an illustration of the city’s attitude towards citizens’ right to know.

Wichita, again, fails at open government

The Wichita City Council, when presented with an opportunity to increase the ability of citizens to observe the workings of the government they pay for, decided against the cause of open government, preferring to keep the spending of taxpayer money a secret.

In the past I’ve argued that Go Wichita is a public agency as defined in the Kansas Open Records Act. But the city disagreed. And astonishingly, the Sedgwick County District Attorney agrees with the city’s interpretation of the law.

So I asked that we put aside the law for now, and instead talk about good public policy. Let’s recognize that even if the law does not require Go Wichita, WDDC, and GWEDC to disclose records, the law does not prohibit them from fulfilling records requests.

Once we understand this, we’re left with these questions:

Why does Go Wichita, an agency funded almost totally by tax revenue, want to keep secret how it spends that money, over $2 million per year?

Why is this city council satisfied with this lack of disclosure of how taxpayer funds are spent?

For that matter, why isn’t Wichita’s check register online?

It would be a simple matter for the council to declare that the city and its taxpayer-funded partner agencies believe in open government. All the city has to have is the will to do this. It takes nothing more.

Only Wichita City Council Member Michael O’Donnell (district 4, south and southwest Wichita) gets it, and yesterday was his last meeting as a member of the council. No other council members would speak up in favor of citizens’ right to open government.

But it’s much worse than a simple failure to recognize the importance of open government. Now we have additional confirmation of what we already suspected: Many members of the Wichita City Council are openly hostile towards citizens’ right to know.

In his remarks, Wichita City Council Member Pete Meitzner (district 2, east Wichita) apologized to the Go Wichita President that she had become “a pawn in the policy game.” He said it was “incredibly unfair that you get drawn into something like this.”

He added that this is a matter for the Attorney General and the District Attorney, and that not being a lawyer, she shouldn’t be expected to understand these issues. He repeated the pawn theme, saying “Unfortunately there are occasions where some people want to use great people like yourself and [Wichita Downtown Development Corporation President] Jeff Fluhr as pawns in a very tumultuous environment. Please don’t be deterred by that.”

Mayor Brewer added “I would have to say Pete pretty much said it all.”

We’ve learned that city council members rely on — as Randy Brown told the council last year — facile legal reasoning to avoid oversight: “It may not be the obligation of the City of Wichita to enforce the Kansas Open Records Act legally, but certainly morally you guys have that obligation. To keep something cloudy when it should be transparent I think is foolishness on the part of any public body, and a slap in the face of the citizens of Kansas. By every definition that we’ve discovered, organizations such as Go Wichita are subject to the Kansas Open Records Act.”

But by framing open government as a legal issue — one that only lawyers can understand and decide — Wichita city government attempts to avoid criticism for their attitude towards citizens.

It’s especially absurd for this reason: Even if we accept the city’s legal position that the city and its quasi-governmental taxpayer-funded are not required to fulfill records request, there’s nothing preventing from doing that — if they wanted to.

In some ways, I understand the mayor, council members, and bureaucrats. Who wants to operate under increased oversight?

What I don’t understand is the Wichita news media’s lack of interest in this matter. Representatives of all major outlets were present at the meeting.

I also don’t understand what Council Member Lavonta Williams (district 1, northeast Wichita) suggested I do: “schmooze” with staff before asking for records. (That’s not my word, but a characterization of Williams’ suggestion made by another observer.)

I and others who have made records requests of these quasi-governmental taxpayer-funded organizations have alleged no wrongdoing by them. But at some point, citizens will be justified in wondering whether there is something that needs to be kept secret.

The actions of this city have been noticed by the Kansas Legislature. The city’s refusal to ask its tax-funded partners to recognize they are public agencies as defined in the Kansas Open Records Act is the impetus for corrective legislation that may be considered this year.

Don’t let this new law be known as the “Wichita law.” Let’s not make Wichita an example for government secrecy over citizens’ right to know.

Unfortunately, that bad example has already been set, led by the city’s mayor and city council.

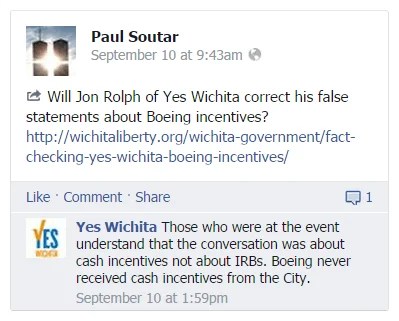

Supporters of the proposed Wichita sales tax contend that the millions in incentives Boeing received were not cash. That’s true — they were more valuable than cash.

At a forum on the proposed Wichita sales tax on September 9, 2014, “Yes Wichita” co-chair Jon Rolph told the audience “The Boeing incentive thing? The city never gave Boeing incentives. They didn’t take our incentive money and run.” As explained at Fact-checking Yes Wichita: Boeing incentives, the claim that the “city never gave Boeing incentives” must be astonishing news to the Wichita city officials who dished out over $600 million in subsidies and incentives to the company.

“Yes Wichita” Facebook page.In response, “Yes Wichita” posted this on its Facebook page: “Those who were at the event understand that the conversation was about cash incentives not about IRBs. Boeing never received cash incentives from the City.”

First, it’s interesting that the person commenting on behalf of “Yes Wichita” was able to read the minds of the audience members. That’s a neat trick. But let’s talk about something more important — the confusion that often surrounds economic development incentives.

“Yes Wichita” contends that although Boeing received an estimated $657,992,250 in property tax abatements over several decades, this doesn’t count as “cash incentives” because it wasn’t given to Boeing in the form of cash.

“Yes Wichita” is correct, in a way. As a result of the City of Wichita’s issuance of industrial revenue bonds, Boeing didn’t receive cash from the city. Instead, the benefits the city initiated on Boeing’s behalf are more valuable to the company than receiving an equivalent amount of cash.

According to IRS guidelines, “tax incentives, whether in the form of an abatement, credit, deduction, rate reduction or exemption, simply reduce the tax imposed by state or local governments.” The IRS says these incentives do not count as income. Therefore, Boeing did not pay income taxes on these benefits, as it would have if the city gave the company cash.

The claim by the “Yes Wichita” group — that tax abatements don’t count as cash incentives — is characteristic of the way economic development incentives are justified. Instead of passing out cash, it’s more common that government uses abatements, credits, tax increment financing, investment in training and infrastructure, or exemptions. Many of these programs are confusing to citizens, and perhaps also to the elected officials who approve them. This allows government to shroud the economic realities of the transaction, and “Yes Wichita” is contributing to this confusion.

Supporters of a proposed Wichita sales tax contend there is only one alternative for paying for a new water supply, and it is presented as unwise.

The major component of the proposed Wichita one cent per dollar sales tax is to pay for a new water supply. Controversy surrounds how the water should be supplied (ASR? El Dorado? New reservoir?) and its urgency. But according to sales tax boosters, there is no controversy about how to pay for a new water supply.

“Yes Wichita” campaign material. Click for larger version.The City of Wichita and the “Yes Wichita” group present two alternatives to Wichita voters: Either (a) approve a sales tax to pay for a new water supply, or (b) the city will borrow to pay for the water supply and water users will pay a lot of interest. Campaign material from “Yes Wichita” states that without a sales tax, “we end up paying 50% more over 25 years because of financing costs.”

Are there other alternatives? Here’s one: If the water supply project costs $250 million, let’s raise water bills by that amount over five years. In this way, water users pay for the new water supply, and we avoid the long-term debt that city council members and “Yes Wichita” seem determined to avoid.

It’s best to have those who use something pay for it directly.Water bills would have to rise by quite a bit in order to raise $50 million per year. But it’s important to have water users pay for water. Also, Wichitans need to be aware — acutely aware — of the costs of a new water supply. Many citizens are surprised to learn that the city has spent $247 million over the past decade on a water project, the ASR program. That money was mostly borrowed, much of it by the same mayor, council members, and city hall bureaucrats that now shun long-term debt.

It will be easier to let people know how much a new water supply costs and how it affects them personally when its cost appears on their water bills. The money that is collected through water bills can be placed in a dedicated fund instead of flowing to the city’s general fund. Then, after the necessary amount is raised, water bills can be immediately adjusted downwards. That’s more difficult to do with a sales tax.

If we pay for a new water supply through a general retail sales tax, the linkage between cost and benefit is less obvious. There is less transparency, and ultimately, less accountability.

Sales tax supporters like “Yes Wichita” claim that one-third of the sales tax collected in Wichita is paid by non-Wichitans. It’s smart, they say, to have visitors to Wichita pay for a portion of the costs of a new water supply. But don’t retail stores pass along their costs — including water bills — to their customers?

Consider this: What is probably the most expensive item sold on a routine basis by a Wichita water utility customer? A good guess would be a Boeing 737 fuselage manufactured by Spirit Aerosystems and sold to Boeing. This item isn’t subject to sales tax. But Spirit can pass along higher water bills to Boeing. (This assumes that shifting costs to outsiders is desirable. I’m not convinced it is.)

According to the Wichita budget, the Wichita water utility provides water to 425,000 customers. As the population of Wichita is about 385,000, there are some 40,000 Wichita water utility customers outside the city. How best to have them help pay for a new water supply: Through their water bills, or hoping that residents of Derby drive past their local Wal-Mart and Target stores to shop at identical stores in Wichita so they can pay sales tax to the city?

There are alternatives for paying for a new water supply other than a sales tax and long-term debt. As has been illustrated by sales tax opponents, water is important, but the need for a new water supply is not as urgent as sales tax supporters portray. There is time to consider other alternatives.

The cost of the proposed Wichita sales tax to households is a matter of dispute. I present my figures, and suggest that “Yes Wichita” do the same.

At a forum on the proposed Wichita sales tax on September 9, 2014, Jennifer Baysinger told the audience that “the average family bringing in about $50,000 a year would pay about $240 a year tax.” She was speaking on behalf of Coalition for a Better Wichita, a group that opposes the one cent per dollar sales tax that Wichita voters will see on their November ballots.

In his rebuttal, “Yes Wichita” co-chair Jon Rolph disputed these figures, saying that Baysinger’s claim would mean that the average family spends $24,000 per year on “groceries and sweaters and socks.” He said a family would need to make $200,000 per year to spend that much on taxable items.

So who is correct? It’s relatively easy to gather figures about sales taxes and households. Here’s what I found.

According to a report from the Kansas Department of Revenue, in fiscal year 2013 the City of Wichita generated $372,843,844 in retail sales tax collections. With a population of 385,577 (2012 value), the tax collected per Wichita resident was $966.98.

Supporters of the proposed sales tax say that one-third of the sales tax collected in Wichita is paid by non-Wichitans. If true, that leaves $248,562,563 in sales tax paid by 385,577 Wichita residents, or $645 per person. This figure is from sales tax being collected at a rate of 7.15 percent, which implies that one cent per dollar of sales tax generates $90 per person. (This assumes that people do not change their purchases because of higher or lower sales taxes, which does not reflect actual behavior. But this is an estimate.)

According to the U.S. Census Bureau, there are 2.49 persons per household in Wichita. That means that a one cent per dollar sales tax has a cost of $224 per household. That’s close to Baysinger’s figure of $240.

We could also take sales tax collections of $248,562,563 and divide by the 151,309 households in Wichita to get a figure of $1,642.75 in sales tax paid per household. Again, since that is tax paid at the rate of 7.15 percent, it implies that one cent per dollar of sales tax generates $230 per household, subject to the same caveats as above. Again, this is close to Baysinger’s figure.

These results are close to my estimation of the cost of the proposed sales tax derived in an entirely different way. I took Census Bureau figures for the amount spent in various categories by families of different income levels. For each category of spending, I judged whether it was subject to sales tax in Kansas. The result was that the average household spent $22,287 per year on taxable items. One percent of that is $223, which is an estimate of the cost of a one cent per dollar sales tax per household. For households in the middle quintile of income, the value was $194. See Wichita sales tax hike would hit low income families hardest for details and charts.

How can the claims of Baysinger and Rolph be so far apart? I’ve presented my reasoning and calculations. The results are figures very close to what Coalition for a Better Wichita is using. Wichita voters might ask that Jon Rolph or one of the other co-chairs of “Yes Wichita” do the same.

The claim that the “city never gave Boeing incentives” will come as news to the Wichita city officials who dished out over $600 million in subsidies and incentives to the company.

At a forum on the proposed Wichita sales tax on September 9, 2014, “Yes Wichita” co-chair Jon Rolph told the audience “The main reason I’m here, I need to educate folks on this. There’s been a lot of misinformation out there.”

The proposed one cent per dollar Wichita sales tax will be voted on by Wichita voters in November. The city plans to use the proceeds for four areas: A new water supply, bus transit, street maintenance and repair, and economic development, specifically job creation. It is the last area that is the most controversial. Sales tax boosters make the case that Wichita has a limited budget for incentives, generally pegged at $1.65 million per year. They say that other cities have much larger budgets, and unless Wichita steps up with additional incentives, Wichita will not be able to compete for jobs.

Wichita has, however, many available incentive programs that are worth much more than $1.65 million per year. Just this week the city extended property tax abatements to one company that are valued at $108,541 per year. The company will receive this benefit annually for five years, with a likely extension for another five years. The city will also apply for a sales tax exemption on behalf of the company. City documents estimate its value at $126,347.

None of this money counts against the claimed $1.65 million annual budget for incentives, as these incentive programs have no cash cost to the city. There is a cost to other taxpayers, however, as the cost of government is spread over a smaller tax base. To the recipient companies, these benefits are as good as receiving cash. I’ve detailed other incentive programs and some recent awards at Contrary to officials, Wichita has many incentive programs.

The nature of, and value of, available incentive programs is important to understand. “Yes Wichita” co-chair Jon Rolph is correct. There is much misinformation. Here’s what he told the audience of young Wichitans after warning about misinformation: “The Boeing incentive thing? The city never gave Boeing incentives. They didn’t take our incentive money and run.”

The claim that the “city never gave Boeing incentives” will come as news to the Wichita city officials who dished out the subsidies and incentives. In a written statement at the time of Boeing’s announcement that it was leaving Wichita, Mayor Carl Brewer wrote “Our disappointment in Boeing’s decision to abandon its 80-year relationship with Wichita and the State of Kansas will not diminish any time soon. The City of Wichita, Sedgwick County and the State of Kansas have invested far too many taxpayer dollars in the past development of the Boeing Company to take this announcement lightly.”

Along with the mayor’s statement the city released a compilation of the industrial revenue bonds authorized for Boeing starting in 1979. The purpose of the IRBs is to allow Boeing to escape paying property taxes, and in many cases, sales taxes. According to the city’s compilation, Boeing was granted property tax relief totaling $657,992,250 from 1980 to 2017. No estimate for the amount of sales tax exemption is available. I’ve prepared a chart showing the value of property tax abatements in favor of Boeing each year, based on city documents. There were several years where the value of forgiven tax was over $40 million.

Boeing Wichita tax abatements, annual value, from City of Wichita.Kansas Representative Jim Ward, who at the time was Chair of the South Central Kansas Legislative Delegation, issued this statement regarding Boeing and incentives:

Boeing is the poster child for corporate tax incentives. This company has benefited from property tax incentives, sales tax exemptions, infrastructure investments and other tax breaks at every level of government. These incentives were provided in an effort to retain and create thousands of Kansas jobs. We will be less trusting in the future of corporate promises.

Not all the Boeing incentives started with Wichita city government action. But the biggest benefit to Boeing, which is the property tax abatements through industrial revenue bonds, starts with Wichita city council action. By authorizing IRBs, the city council cancels property taxes not only for the city, but also for the county, state, and school district.

We’re left wondering, as we have wondered before, whether the “Yes Wichita” campaign is uninformed, misinformed, or intentionally deceptive in making its case to Wichita voters.

Kansas Policy Institute is hosting a conference titled “Fostering Economic Growth in Wichita.” This is the second in a series of events looking at issues surrounding the proposed sales tax in Wichita. Voters will see the sales tax question on the ballot in November.

This event focuses on the economic development, or jobs, portion of the sales tax. The other areas sales tax funds would be spent on are a new water supply, street maintenance and repair, and bus transit.

This is event on Friday September 19, from 7:30 am to noon, held in room 132 of the Wichita State University MetroPlex. the event is free, and you may register here.

Here is the lineup of speakers and topics:

Nuts and Bolts of the “Jobs Fund” Proposal: Wichita Metro Chamber of Commerce with:

Paul Allen, Allen Gibbs & Houlik, Leadership Council Jobs Task Force

Jeff Finkle, President/CEO, International Economic Development Council

Dr. John Tomblin, Vice President for Research and Technology Transfer, Wichita State University

Examining Kansas’ Incentive History:

Nathan Jensen, Ph.D., Associate Professor at George Washington University

Trends of Wichita’s Economy:

Jeremy Hill, Director of Wichita State University’s Center for Economic Development and Business Research

Creating a Dynamic Local Economy:

Pamela Villarreal, Senior Fellow at the National Center for Policy Analysis

This is the second in a series of KPI-sponsored forums covering the various aspects of the 1% sales tax proposal. A forum on the water proposal was held in July, and a forum on the street and transit portion will be held in the near future. Kansas Policy Institute is hosting these events to give citizens the opportunity to hear experts address all sides of the issues, and is not taking a position on the individual aspects of the 1% sales tax proposal.

According to IRS guidelines, “tax incentives, whether in the form of an abatement, credit, deduction, rate reduction or exemption, simply reduce the tax imposed by state or local governments.” The IRS says these incentives do not count as income. Therefore, Boeing did not pay income taxes on these benefits, as it would have if the city gave the company cash.

According to IRS guidelines, “tax incentives, whether in the form of an abatement, credit, deduction, rate reduction or exemption, simply reduce the tax imposed by state or local governments.” The IRS says these incentives do not count as income. Therefore, Boeing did not pay income taxes on these benefits, as it would have if the city gave the company cash.

The claim that the “city never gave Boeing incentives” will come as news to the Wichita city officials who dished out the subsidies and incentives. In a written statement at the time of Boeing’s announcement that it was leaving Wichita, Mayor Carl Brewer wrote “Our disappointment in Boeing’s decision to abandon its 80-year relationship with Wichita and the State of Kansas will not diminish any time soon. The City of Wichita, Sedgwick County and the State of Kansas have invested far too many taxpayer dollars in the past development of the Boeing Company to take this announcement lightly.”

The claim that the “city never gave Boeing incentives” will come as news to the Wichita city officials who dished out the subsidies and incentives. In a written statement at the time of Boeing’s announcement that it was leaving Wichita, Mayor Carl Brewer wrote “Our disappointment in Boeing’s decision to abandon its 80-year relationship with Wichita and the State of Kansas will not diminish any time soon. The City of Wichita, Sedgwick County and the State of Kansas have invested far too many taxpayer dollars in the past development of the Boeing Company to take this announcement lightly.”