The conversion of a medical facility should receive city scrutiny due to tax breaks granted based on its original use.

The Wichita Eaglereports that a freestanding emergency room in northeast Wichita has closed after two years. It will be converted to a cardiology office under the same ownership.

As I reported in Free standing emergency department about to open in Wichita, the facility received property tax abatements worth an estimated $61,882 per year in the first year. The abatement was scheduled to last for five years, with a likely extension for an additional five years. These abatements were obtained through the use of the industrial revenue bonds program.

The emergency room, also called a freestanding emergency department, qualified for tax abatements under a city policy that “requires medical facilities to attract at least 30% of patients from outside the Wichita MSA.” It is not known whether the shift from an emergency department to a cardiology office will meet this requirement.

Further, the ordinance the council passed refers specifically to “an emergency medical facility,” not a cardiology office.

These two significant changes ought to, at minimum, be brought to the attention of the Wichita City Council.

Also reported in Free standing emergency department about to open in Wichita, treatment in these emergency departments is expensive. While I do not have information on this specific ED, UnitedHealth Group found this in its analysis of freestanding emergency departments: “FSEDs largely treat non-emergent conditions: 2.3 percent of FSED visits in the U.S. are emergent or immediate and require services unique to an ED.” Also, “In Texas, the average cost of treating common conditions at an FSED ($3,217) is 22 times more than at a physician office ($146) and 19 times more than at an urgent care center ($167).” UnitedHealth Group is a large insurer.

The City of Wichita may spend to create a COVID-19 expense tracking project and to bypass normal purchasing processes.

At Tuesday’s meeting of the Wichita City Council, members will consider measures to help the city respond to the COVID-19 pandemic.

In the agenda packet for the meeting, the city advises that the pandemic will financially impact the city, and that the city needs to take steps to respond.

According to the city document, the city may experience extra costs and revenue shortfalls. There is the potential for the city to be compensated for these if the city can “aggregate and track relevant costs.” The city proposes a project with an initial budget of one million dollars to accomplish this. A proposed ordinance authorizes issuing general obligation bonds to provide funding.

Also, a proposed ordinance authorizes the city manager to bypass the regular city purchasing process. That, according to city code, requires public bidding for purchases over $50,000. The proposed ordinance authorizes the manager to use the “public exigency” exception. The ordinance also authorizes the manager to make necessary budget adjustments to this regard. Also, a person may be designated as the city’s authorized representative when dealing with federal or state agencies.

It would be simple for the City of Wichita to include additional relevant information regarding economic development incentive decisions.

When the Wichita City Council makes decisions regarding economic development incentives, the Center for Economic Development and Business Research at Wichita State University prepares an analysis for the city. The purpose of the analysis is to determine benefit-cost ratios for overlapping governmental jurisdictions, purporting to show that these jurisdictions will receive more in benefits than they pay in costs. An example of the analysis for a large project is here.

The city does not make this analysis document available to the public. It is a public record, though. Every time I have asked, they have been provided.

One thing, then, that the city could do to increase transparency is to simply make these analysis documents available. Perhaps not in the agenda packet, but as a supplement, such as the way the city provides Powerpoint presentations for council meetings.

Another thing the city could do is to include relevant data that would take just a little more effort.

Consider sales tax exemptions. For a recent industrial revenue bond decision, city documents stated: “The project will also qualify for a sales tax exemption on bond-financed purchases.” 1 But the document doesn’t state the dollar value of the sales tax exemption, even though the CEDBR analysis includes this number. 2 That value, for this recent project, is $1,111,264.

Is that information relevant to decision-makers? City documents estimate the value of the property tax abatements in the first year as $773,604. So for the total tax forgiveness received in the first year, the sales tax exemption is larger than the property tax abatement, accounting for 59.0 percent of the total. 3 That is relevant.

Even over the ten-year life of the property tax abatement, the sales tax exemption is still 11.8 percent of the total tax forgiveness. That — the duration of the property tax abatement — is another opportunity to increase transparency. The CEDBR analysis gives the total cost of the incentives for ten years. (A nearby table summarizes.) These totals are speculative, as the city council must revisit the matter in five years to determine whether the company deserves the property tax abatement for an additional five years. (This is known as a “five-plus-five year tax exemption.”)

But the total value of the exemptions is relevant, as it flows into the benefit-cost ratio calculations.

Given all the numbers the city presently reports from the CEDBR analysis documents, not including the value of the sales tax exemption is a significant omission, and one easy to correct.

—

Notes

Wichita city council agenda packet for January 21, 2020, item V-1 ↩

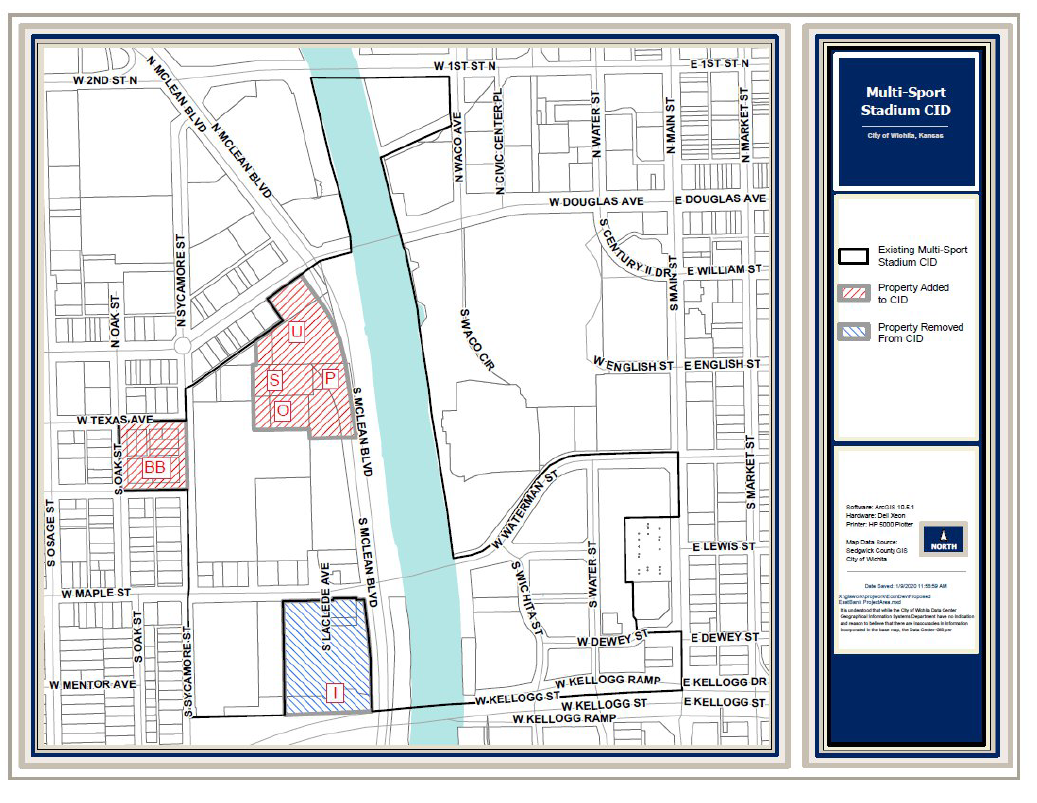

The City of Wichita plans to expand a special tax district.

Next week the Wichita City Council will consider expanding an existing CID, or Community Improvement District, in the Delano neighborhood near downtown Wichita. A map provided by the city is nearby.

Community Improvement Districts are a mechanism whereby extra sales tax is collected within a district. For this CID, the city asks to collect an extra two cents per dollar, which is the maximum allowed in Kansas.

CIDs are distinguished from STAR bonds, in which incremental sales tax revenue in a district is captured and handled differently from the base sales tax. The sales tax rate remains as before. The ballpark and surrounding area use both CID and STAR bonds, as well as other public funding.

In its analysis appearing in the agenda packet for the February 11, 2020 meeting, the city provides this:

The expanded boundaries will permit the collection of additional CID revenues and the application thereof to development opportunities as well as the design and construction of the Stadium, utilities, parking, and other improvements related to the Stadium and river corridor improvements. The expansion further permits the use of funds to support the construction of public auditoriums and convention centers.

The CID petition included the $83,000,000 stadium project, which includes both the $75,000,000 stadium and $8,000,000 in supporting infrastructure. The amended petition has an estimated project costs of $210,200,000, which includes the additional $127,200,000 in project costs related to the Riverfront Partners project.

Project costs originally included costs related to the development of a multi-sport stadium, related infrastructure and adjacent commercial, retail residential and parking structures. The amendment has been expanded to include public auditoriums and convention centers as well as the additional commercial construction on the Development Site.

In this context, “Development Site” refers to the Riverfront Partners site north of the ballpark, southwest of Douglas and McClean Boulevard.

Of note, the CID includes a portion of the land included in the Riverfront Legacy Master Plan. The city contemplates that CID funds might be used there: “The petition also requests that the uses of CID revenues be expanded to include uses contemplated by the DA to be made on the Development Site, costs for additional parking and costs that may be associated with for potential development on the east side of the Arkansas River that is within the Stadium CID.”

The item the council will consider also includes a correction, as explained by the city: “The petition also requests removal of certain City-owned property that was inadvertently included in the Stadium CID.”

The city plans to borrow funds to be repaid by the CID tax collections: “The City anticipates issuing up to $13,000,000 in bonds, based on a pledge of CID revenue.”

Don’t want to pay? Don’t go there.

Does the use of CID mean the city has raised taxes? Certainly, the sales tax within the CID is higher (9.5 percent) than outside (7.5 percent). But that extra tax can be avoided. It is common for city council members to advise citizens that if they don’t want to pay the higher sales tax, just don’t go there.

On the surface, this reasoning is correct. But as explained in city documents, the city is borrowing money to be repaid by CID tax collections. If enough people take this advice and avoid patronizing merchants within the CID, there may be a shortfall of money to make bond payments. Since the city’s policy is that CID bonds are not backed by the full faith and credit of the city, Wichita as a city is not on the hook. 1 But should this happen and the city defaulted on CID bonds, it would be a severe blow to the city’s reputation.

A similar situation exists for the STAR bonds the city has issued to fund the ballpark and related spending. If the district fails to generate enough incremental sales tax revenue to make bond payments, city taxpayers are not liable. 2 But the failure of these bonds would, again, severely damage the city’s reputation.

Further, the city expects property tax revenue to pay off tax increment financing (TIF) bonds issued in favor of the project.

Even more, the city expects the economic activity generated by the ballpark and surrounding development to spin-off associated economic activity that will generate further tax revenue. If this does not happen, and happen in a big way, the project threatens to be a burden on the city budget, and by extension, taxpayers.

From the agenda for the February 11, 2020 council meeting, showing area to be added and removed from the CID. Click for larger.

—

Notes

City Of Wichita Community Improvement District Policy. “While the CID Act permits the issuance of either full-faith and credit general obligation bonds or special obligation bonds, payable solely from the CID revenue, it is the policy of the City of Wichita to issue only special obligation CID bonds.” ↩

$42,140,000 City Of Wichita, Kansas Sales Tax Special Obligation Revenue Bonds (River District Stadium Star Bond Project) Series 2018. “The series 2018 bonds are not general obligations of the city and neither the full faith and credit nor the general taxing power of the city, the state, or any political subdivision thereof is pledged to the payment of the series 2018 bonds. The series 2018 bonds shall not constitute an indebtedness of the city, the state, or any political subdivision thereof within the meaning of any constitutional or statutory debt limitation or restriction.” ↩

The City of Wichita property tax mill levy rose for 2019.

In 1994 the City of Wichita mill levy rate — the rate at which real and personal property is taxed — was 31.290. In 2019 it was 32.721, based on the Sedgwick County Clerk. That’s an increase of 1.431 mills, or 4.57 percent, since 1994. (These are for taxes levied by the City of Wichita only, and do not include any overlapping jurisdictions.)

Wichita mill levy rates. This table holds only the taxes levied by the City of Wichita and not any overlapping jurisdictions. Click for larger version.

The rate for 2019 was up by 0.17 percent from 2018 and follows three years of virtually no change.

Wichita mill levy rates. Click for larger version.

The Wichita City Council does not set the mill levy rate. Instead, the rate is set by the county based on the city’s budgeted spending and the assessed value of taxable property subject to Wichita taxation.

While the city council doesn’t have direct control over the assessed value of property in its jurisdiction, it does have control over the amount it decides to spend. 1 As can be seen in the chart of changes in the mill levy, the city usually decides to spend more than the mill levy is likely to generate in taxes. Therefore, the mill levy usually rises. 2

Change in Wichita mill levy rates, year-to-year and cumulative. Click for larger version.

It is more common for the mill levy to rise rather than to fall. In those years, the council does not take responsibility for the increase, insisting that the rate has not gone up, or that the rate is stable, or that an increase isn’t the council’s fault.

An increase of 4.57 percent over more than two decades may not seem like much of an increase. But this is an increase in a rate of taxation, not tax revenue. As such, it is not appropriate to adjust for inflation.

Inflation, however, does play a role in tax revenue. As property values rise, property tax bills also rise, even if the mill levy rate is unchanged. In Wichita, the taxes on a hypothetical home worth $100,000

The total amount of property tax levied is the mill levy rate multiplied by the assessed value of taxable property. This amount usually rises each year, due to these factors:

Appreciation in the value of existing property

An increase in the amount of property

Spending decisions made by the Wichita City Council

Application of tax revenue has shifted

Wichita mill levy, percent dedicated to debt service. Click for larger version.

The allocation of city property tax revenue has shifted over the years. According to the 2010 City Manager’s Policy Message, page CM-2, “One mill of property tax revenue will be shifted from the Debt Service Fund to the General Fund. In 2011 and 2012, one mill of property tax will be shifted to the General Fund to provide supplemental financing. The shift will last two years, and in 2013, one mill will be shifted back to the Debt Service Fund. The additional millage will provide a combined $5 million for economic development opportunities.”

In 2018 the city budget held this regarding the debt service fund: “In both 2013 and 2014, 0.5 mills were shifted back to the Debt Service Fund.”

Taxes a homeowner pays

Following, a chart showing the taxes paid to the City of Wichita for a hypothetical home. This includes changes in the value of the home (based on U.S. Federal Housing Finance Agency, All-Transactions House Price Index for Wichita, KS (MSA) [ATNHPIUS48620Q]) and inflation (based on Consumer Price Index Series II: CUUR0000SA0, U.S. city average, All items, Base Period 1982-84=100, Bureau of Labor Statistics). Click for larger versions.

—

Notes

Although the city often grants property tax abatements at its discretion, thereby effectively removing that property from the tax rolls. ↩

Mill Levy Facts, City of Wichita 2020 — 2021 Proposed Budget. “First, the City (the taxing district) arrives at a total amount for expenditures in the taxing funds. In Wichita these funds are the General Fund and the Debt Service Fund. After expenditure totals are known, all other revenue sources (non-property taxes and fees) are subtracted. The remainder is the amount to be raised from ad valorem (property) taxes. … The tax levy rate is calculated by dividing the total revenue to be obtained from property taxes by the total assessed value for the taxing district.” ↩

The profit-sharing agreement for Naftzger Park event management contains ambiguity that could lead to disputes.

Today the Wichita City Council approved an agreement with Wave Old Town LLC for event management in Naftzger Park in downtown Wichita. The agreement was approved unanimously.

While there was controversy over the awarding of the contract (Wichita Eagle reporting is here), others have noticed that the contract is imprecise in a way that could lead to problems.

The city and Wave will share profits and losses based on a schedule in the management agreement contained in the agenda packet for today’s meeting, Item V-2. The issue is when the profit-sharing is calculated.

Profit-sharing agreement for City of Wichita and Wave. Click for larger.

Based on the way the profit-sharing is calculated, different profit-sharing results could be obtained from the same event history. The management services agreement the city council passed today does not speak to this issue. Neither does the request for proposal for event management.

The issue is when the profit-sharing calculation is performed and using which data, as follows:

Profit-sharing could be calculated independently for each event, using data for just the current event. This is illustrated in example 1.

Profit-sharing could be calculated once at the end of the year (or another period) using the sum of events during the period. This is shown in example 2.

Profit-sharing could be calculated independently for each event, using cumulative data for the year (or another period). Example 3 illustrates.

As the following examples show, the differences between these three methods of calculation could be substantial. These three examples assume two events, one with an event profit of $49,999, and the second with an event loss of $49,999. Notice that depending on how and when the same calculation is performed, Wave’s share of profits could be $0, or $25,000, or $49,999. The city could either lose $25,000 or $0.

While these examples are contrived and use extreme values, they illustrate that the agreement the council passed is ambiguous. There could be disputes that could be avoided with careful attention to detail by the city when constructing contracts.

Wichitans carry a “Taxpayer Burden” of $1,200 per taxpayer, which is not as bad as many cities.

Truth in Accounting is an organization that works to improve the reliability and transparency of governmental financial information. 1 Annually, it produces a report titled Financial State of the Cities that examines the fiscal health of cities. The report does not take into account economic factors like economic growth, but instead compares a city’s assets with the bills it has accumulated.

Most cities, Wichita included, have a shortfall. The primary reasons for a shortfall are unfunded pension liabilities and unfunded post-employment benefits, called OPEB. TIA explains: “When cities do not have enough money to pay their bills, TIA takes the money needed to pay bills and divides it by the estimated number of city taxpayers. We call the resulting number a Taxpayer Burden and rank cities based on this measure.” 2 The report released this month is based on comprehensive annual financial reports (CAFR) for fiscal year 2018.

In the net, Wichita has a taxpayer burden of $1,200 per person, meaning “If retirement benefits or other costs are not reduced, then taxpayers could have to pay $1,200 in future taxes without receiving any related services or benefits. According to TIA, “Wichita’s financial problems stem mostly from unfunded retirement obligations that have accumulated over the years. Of the $1.5 billion in retirement benefits promised, the city has not funded $257.4 million in pension and $34.9 million in retiree health care benefits.”

Wichita ranks eighteenth among the nation’s 75 largest cities (the rank of one is best.) Wichita earned a grade of “C” along with 27 other cities.

In the previous year, Wichita ranked tenth, having a surplus of $800 per taxpayer.

By the way, the Government Financial Officers Association (GFOA) standard is for cities to publish their CAFRs 180 days after the end of the fiscal year. TIA says it is ideal for cities to publish within 100 days. Wichita published in 179 days.

—

Notes

“The nonpartisan mission of TIA is to educate and empower citizens with understandable, reliable, and transparent government financial information. TIA is a 501(c)(3) nonprofit, nonpartisan organization composed of business, community, and academic leaders interested in improving government financial reporting.” See https://www.truthinaccounting.org/about/page/faqs-2. ↩

The Wichita city council will consider a tax giveaway for an economic development project that does not meet its stated policy.

Tomorrow the Wichita City Council will consider issuing up to $33 million in Industrial Revenue Bonds in relation to a project at the Wichita State University Innovation Campus.

Despite its name, in the IRB program the city does not purchase bonds or lend money. The city does not guarantee the payment of the bond interest or principle. Instead, the IRB program allows the city to grant tax forgiveness, both property tax and sales tax. 1 City documents explain: “MWCB is also requesting a sales tax exemption on items purchased for the project and a 100% five-year tax exemption on the IRB-financed real property improvements plus a second five-year exemption subject to City Council approval.” 2 (emphasis added)

How much tax is being forgiven? For property tax, $773,604 annually for up to ten years, again from city documents:

Based on the latest available mill levy, and assuming that the real property improvements are valued at 80% of the actual capital investment, the estimated value of the property tax abatement for the first full year is approximately $773,604. The value of a 100% real property tax exemption as applicable to the taxing jurisdictions is:

City $215,767

State $9,900

County $193,927

USD 259 (Wichita Public School District) $354,010

City documents don’t estimate the amount of sales tax savings, but if all the bond proceeds were spent on taxable items, the savings would be $2,475,000.

This project fails to meet standards set by the city and county for payback from economic development incentives. According to the city’s economic development pages, “City benefit/cost ration must be at least 1.3 to 1.” 3 This requirement is repeated in the Sedgwick County/City of Wichita Economic Development Policy: “The ratio of public benefits to public costs, each on a present value basis, should not be less than 1.3 to one for both the general and debt service funds for the City of Wichita; for Sedgwick County should not be less than 1.3 overall.” 4

The benefit-cost ratios supplied for this project don’t meet the city and county standards, again from city documents:

A benefit/cost analysis was performed by Wichita State University’s Center for Economic Development and Business Research based upon the proposed Letter of Intent, with the following ratio of benefits to costs:

City of Wichita 1.18 to 1.00

City General Fund 1.10 to 1.00

City Debt Service 1.37 to 1.00

Sedgwick County 1.11 to 1.00

USD 259 1.34 to 1.00

State of Kansas 5.08 to 1.00

While the 1.3 to one threshold is met for the city’s debt service fund, it is not met for the city as a whole. Additionally, it doesn’t meet the 1.3 to one threshold for Sedgwick County. The Sedgwick County/City of Wichita Economic Development Policy specifies mitigating factors that can be used to bypass the 1.3 to one requirement, but city documents do not mention these.

Pieter Brueghel the Younger. The tax-collector’s office.

Even over the ten-year life of the property tax abatement, the sales tax exemption is still 11.8 percent of the total tax forgiveness. That — the duration of the property tax abatement — is another opportunity to increase transparency. The CEDBR analysis gives the total cost of the incentives for ten years. (A nearby table summarizes.) These totals are speculative, as the city council must revisit the matter in five years to determine whether the company deserves the property tax abatement for an additional five years. (This is known as a “five-plus-five year tax exemption.”)

Even over the ten-year life of the property tax abatement, the sales tax exemption is still 11.8 percent of the total tax forgiveness. That — the duration of the property tax abatement — is another opportunity to increase transparency. The CEDBR analysis gives the total cost of the incentives for ten years. (A nearby table summarizes.) These totals are speculative, as the city council must revisit the matter in five years to determine whether the company deserves the property tax abatement for an additional five years. (This is known as a “five-plus-five year tax exemption.”)