Kansas hotel guest tax collections presented in an interactive visualization.

Cities and counties in Kansas may levy a transient guest tax collection on hotel guests. It is sometimes called a bed tax or guest tax. The tax is collected as a percentage of total room revenue, not the number of rooms or the rate charged for rooms. While the Kansas Department of Revenue collects the tax, the proceeds are returned to the cities or counties, except for a two percent processing fee. In Wichita the rate is six percent.

In some cases, jurisdictions may levy additional taxes that may not be paid to the Kansas Department of Revenue. This is the case with the Wichita city tourism fee, which took effect on January 1, 2015. This tax of 2.75% is paid directly to the city1, so it doesn’t appear in KDOR figures.

Also, jurisdictions may change the tax rate. The Kansas Department of Revenue maintains a list of taxes charged. 2

The visualization has three views of data. One is a table of collections, including percent change from the previous year. A line chart shows the dollar amount of collections. A second line chart shows collections indexed to a common starting point. This is useful for comparing the relative change in guest tax collections. These line charts show data as the average of the previous 12 months.

Examples of nondisclosure.This data does not represent all hotels in Kansas. Confidentiality rules prohibit disclosure when a jurisdiction has a small number of hotels. In the nearby example, the value “C” is reported for Sedgwick County, indicating such non-disclosure. Obviously, there are hotels in Sedgwick County. But considering hotels in Sedgwick County that are not located in cities like Wichita, the number is too small to report, based on confidentiality guidelines. Similarly, for small cities, data is probably not available to the public.

Of note, while Wichita is the largest city in Kansas, Overland Park collects the most hotel guest tax. Of the largest markets in Kansas, Wichita has experienced the least growth in hotel tax collections since 2010.

A look at actual spending on Kansas highways, apart from transfers.

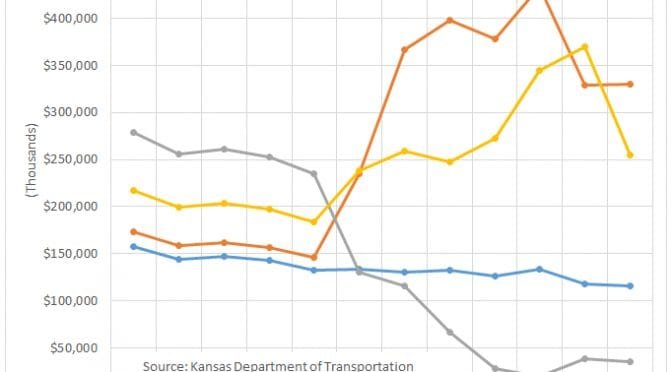

KDOT spending, major road programs. Click for larger.KDOT spending, total road programs. Click for larger.KDOT transfers. Click for larger.KDOT funding sources, partial. Click for larger.When we look at actual spending on Kansas roads and highways, we see something different from what is commonly portrayed. Kansas Department of Transportation publishes a Comprehensive Annual Financial Report that details spending in four categories. These figures represent actual spending on roads and highways, independent of transfers to or from the highway fund.

For fiscal year 2017, which ended June 30, 2017, spending on three categories (Maintenance, Preservation, and Modernization) was nearly unchanged from the year before, while spending on the category Expansion and Enhancement fell by 31 percent.

For these four categories — which represent the major share of KDOT spending on roads — spending in fiscal 2017 totaled $738.798 million. That’s down 14 percent from $857.133 million the year before, and up from a low of $698.770 million in fiscal 2010.

Again, these are dollars actually spent on highway programs. A common characterization of the way Kansas government is funded is called “robbing the bank of KDOT.” To the extent that characterization is accurate, there is a separate line item titled “Distributions to other state funds” that holds these values. It appears in the nearby table. A chart shows sales tax distributions from the general fund to KDOT, and transfers from KDOT.

Many also criticize Kansas government for slashing highway spending, letting our roads crumble. While total spending on these four programs has been falling (after adjusting for inflation), the decline is minor compared to the hysterical claims of those with vested interests in more government, and especially highway, spending.

Kansas law specifies how much sales tax revenue is transferred to the highway fund. Here are recent rates of transfer and dates they became effective: 1

July 1, 2010: 11.427%

July 1, 2011: 11.26%

July 1, 2012: 11.233%

July 1, 2013: 17.073%

July 1, 2015: 16.226%

July 1, 2016 and thereafter: 16.154%

A nearby chart shows the dollar amounts transferred to the highway fund from sales tax revenue. In 2006 the transfer was $98.914 million, and by 2016 it had grown to $514.519 million.

KDOT spending, major road programs. Click for larger.

Kansas Legislative Research Department, one of four nonpartisan agencies that provide support services for the Kansas Legislature, 1 has released its annual highlights of legislation document for the 2017 session.

This is a 12-page document that provides short summaries of each bill. KLRD also publishes lengthier summaries of legislation.

Click here to access Kansas Legislative Research Department publication page, or click here to directly access the 2017 highlights document.

A Kansas public policy group celebrates tax increases. But it isn’t enough, and more reform is required.

Kansas Center for Economic Growth has promoted higher taxes in Kansas for many years, and this year it got its wish. Here are a few remarks based on its self-congratulatory article titled “Happy Fiscal New Year, Kansas.”

KCEG wrote: “Kansas is now better positioned to provide great schools”

Wait a moment. I thought Kansas already has great schools. That’s what the Kansas public school establishment tells us.

And I think that the author made a mistake here. Instead of writing about “public schools,” the author mentions — simply — “schools.” Usually the Kansas public school establishment is careful to qualify their plea for more school spending with “public.” To them, spending on private schools or charter schools is money wasted, money that should have gone to public schools. Fortunately, and amazingly, the tax credit scholarship program, a program limited to students currently in low-performing schools, was expanded slightly. 1

If KCEG really wanted to promote great schools in Kansas, it would embrace school programs such as charter schools.

KCEG: “vibrant communities”

Here, KCEG believes that taking more money from the private sector through taxation and letting government spend it is “vibrant.” But how does government work? In a democracy, a majority forces its will on the minority. Or, special interest groups intensely lobby for benefits at the expense of everyone else. Or, a form of the precautionary principle tamps down sparks of innovation in government bureaucracies, like public schools. Government is the opposite of “vibrant,” which the dictionary defines as “full of energy and enthusiasm.”

KCEG: “It also phases in the restoration of an important tax credit and three deductions that were eliminated in 2012 to pay for tax breaks for the wealthy.”

In 2012 everyone’s taxes were cut. Aside from that, we don’t pay for tax cuts. We pay for the cost of government.

When someone says we must pay for tax cuts, it presumes that tax cuts have a cost. The only way this makes sense is if we believe that the state has first claim on our incomes. The state takes what it says it needs, and we get to keep the rest. If the government is ever persuaded to reduce its claim on our incomes, that has a cost that must be paid in some way.

But for those who believe in self-ownership, this is nonsense. It’s the people who “give” tax money to the government, not the government who “gives” it back in the form of tax cuts. If the government cuts taxes, the government gives us nothing. It simply takes less of what is ours in the first place.

But the attitude of many government officials is the opposite. In 2006 Kansas cut taxes on business equipment and machinery. At the time, the Wichita Eagle reported: “Gov. Kathleen Sebelius, a Democrat, who first proposed the business machinery tax cut, agreed. ‘We’re not giving away money for the sake of giving it away,’ she said. ‘I’m hoping that the economic growth will actually help fund the school plan that we just passed.’” (emphasis added)

(By the way, this sounds like Sebelius was planning for tax cuts to pay for themselves.)

KCEG: “This means looking beyond income tax reforms and rebalancing Kansas’ ‘three-legged stool’ by addressing problems with the state’s sales tax and property tax.”

The three-legged stool is one of the most inappropriate analogies ever coined. If the state of Kansas were to develop an additional source of tax revenue, say by slapping a tariff on Budweiser imported from Missouri or Coors imported from Colorado, we’d hear spending advocates like KCEG speaking of the virtue of a stable four-legged chair. Many states thrive without one of our three legs, the income tax. And if we’re looking for stability, as Hineman mentions, income taxes are quite volatile compared to the other legs. 2

KCEG: “To pay for the Governor’s irresponsible and steep income tax cuts”

Again, we don’t have to pay for tax cuts. But there was irresponsible behavior, that being to continue to spend and avoid serious attempts at spending reform.

KCEG: “In response to the ongoing budget crisis, the sales tax was increased in 2015 to offset lagging state revenue. This affected every Kansan in every county, but especially hurt low-income residents.”

Here, KCEG is correct. The state should not have raised the sales tax, and the state needs to work on lowering the sales tax rate on groceries. For more on this topic, see Wichita sales tax hike would hit low income families hardest and Kansas sales tax has disproportionate harmful effects.

(Actually, KCEG is not totally correct. The sentence should have ended with “… to continue to pay for wasteful state spending because the governor and legislature would not seriously consider spending reform.”)

KCEG: “And because of the gamble with income tax cuts”

There was no gamble with income tax cuts, the governor’s boastful claims notwithstanding. 3 The tax cuts did what tax cuts should do: Leave more money in the hands of the people it belongs to.

KCEG: “As a result, property taxes shot up as communities struggled to keep up with the demand for basic services.”

If taxation was shifted from the state level to local levels, that in itself is not bad. In fact, it keeps taxing and spending more closely controlled at the local level, without communities having to fight in Topeka for a share of the state budget pie.

KCEG: “If we want to fully recover from the past five years, tax reform must address sales and property tax problems in addition to income tax issues.”

KCEG doesn’t say what are the problems with sales and property taxes. But I think I know what they believe: These two forms of taxation are too low. They don’t raise enough money from the right people.

—

Notes

“On and after July 1, 2018, the bill amends the definition of “public school” within the TCLISS Program Act to mean a school identified by KSBE as one of the lowest 100 performing schools with respect to student achievement. It also amends the definition of “qualified school” to require accreditation on and after July 1, 2020. Accreditation must be by KSBE or a KSBE-recognized national or regional accrediting agency. Additionally, the bill expands eligibility for the tax credit to individuals and places an annual cap of $500,000 on contributions.” Kansas Legislature. SB 19: Creating the Kansas school equity and enhancement act, summary. Available at http://www.kslegislature.org/li/b2017_18/measures/sb19/. ↩

Another Kansas legislator explains why raising taxes was necessary. So he says.

Many members of the Kansas Legislature are writing pieces defending their decision to vote for higher taxes. Don Hineman is one. His explanation merits more than average attention, as he is the Majority Leader of the Kansas House of Representatives. This week the Topeka Capital-Journal published his op-ed Rep. Don Hineman: Why tax reform was necessary. It deserves comment.

Hineman wrote: “This return to common sense tax policy resulted from legislators listening to their constituents and fulfilling the promises they made during 2016 campaigns.”

There may have been some candidates who campaigned on a platform of higher taxes. But most used more subtle language, such as Hineman’s use of the phrase “common-sense tax policy.” Does anyone know what that means? Does it mean the same thing to everyone? Besides, raising taxes was just one issue for most candidates and campaigns. And, voters must vote for candidates, not specific policies. As Justice Antonin Scalia told us, “Campaign promises are, by long democratic tradition, the least binding form of human commitment.” An example comes from Hineman’s web page, which states one of his four core values is “Respect for private property rights.” He has respect for your property, unless that property happens to be your money. Then he wants more.

Hineman: “… restore our state to firmer fiscal ground.”

This could have been done with spending cuts, too.

Hineman: “… a group of 88 representatives and 27 senators from across the political spectrum voted to override the governor’s veto.”

Here, Hineman refers to the coalition of Republicans and Democrats that passed the tax bill notwithstanding the governor’s veto. Because members of both major parties voted the same way, it’s described as nonpartisan. It’s meant as a good thing. But most of the Republicans who voted for higher taxes qualify as Democrats in many ways. They dismiss the Republican Party platform and embrace most aspects of the Democratic Party and progressive goals. There is no “spectrum.” Regarding taxation and the size of government, they’re pretty much the same color. Kansas Policy Institute confirms: “The Freedom Index published by Kansas Policy Institute has repeatedly shown the legislative political division to not be about Democrats and Republicans but about legislators’ view of the role of government, and the above June 2 update of 2017 Freedom Index certainly bears that out. With a score of 50 percent being considered neutral, there are 13 Senators at the top of the list with positive scores and 13 Senators at the bottom of the list — and every one of them is a Republican.” 1

Hineman: “Brownback’s tax plan abandoned the ‘three-legged stool’ approach to funding government, which had served Kansas well for decades by relying on a stable balance of income, sales and property.”

The three-legged stool is one of the most inappropriate analogies ever coined. If the state of Kansas were to develop an additional source of tax revenue, say by slapping a tariff on Budweiser imported from Missouri or Coors from Colorado, we’d hear spenders like Hineman speaking of the virtue of a stable four-legged chair. Many states thrive without one of our three legs, the income tax. And if we’re looking for stability, as Hineman mentions, income taxes are quite volatile compared to the other legs. 2

As far as serving Kansas well: There are a variety of ways to look at the progress of Kansas compared to the nation, but here’s a startling fact: For the 73rd Congress (1933 to 1935) Kansas had seven members in the U.S. House of Representatives. (It had eight in the previous session.) Until 1992 Kansas had five. Today Kansas has four members, and may be on the verge of losing one after the next census. This is an indication of the growth of Kansas in comparison to the nation.

” … sweep from the highway fund … rejected the governor’s short-term fixes as being neither responsible nor conservative …”

In this (heavily edited) sentence, Hineman complains about sweeping money from the state’s highway fund. But: Even after raising taxes, the budget just passed by the legislature continues sweeps from the highway fund in the amount of $288,297,663 in fiscal year 2018. For fiscal year 2018, the total of the quarterly sweeps is $293,126,335. 3

Hineman: “The fiscal strain created by the 2012 tax cuts caused public schools to suffer, increasing class sizes and reducing program offerings.” Kansas school spending. See article for notes about 2015. Click for larger.The nearby chart shows Kansas school spending, per pupil, adjusted for inflation. It’s easy to see that since 2011, spending has been remarkable level. There was a change in 2015 that shifted the way some school funding was credited, but in total, not much changed.

Kansas school employment. Click for larger. Kansas school employment ratios. Click for larger.Some people will dismiss spending figures for a variety of reasons. They may say that inflation affects schools differently from everything else, or that these figures don’t include KPERS, or that they do include the cost of facilities. So let’s look at something else: The number of employees compared to the number of students. When we do this, we find that igures released by the Kansas State Department of Education show the number of certified employees rose slightly for the 2016-2017 school year.

The number of Pre-K through grade 12 teachers rose to 30,431 from 30,413, an increase of 0.06 percent. Certified employees rose to 41,459 from 41,405, or by 0.13 percent.4 These are not the only employees of school districts.5

Enrollment fell from 463,504 to 460,491, or 0.61 percent. As a result, the ratios of teachers to students and certified employees to students fell. The pupil-teacher ratio fell from 15.2 pupils per teacher to 15.1. The certified employee-pupil ratio fell from 11.2 to 11.1.

If we look at these ratios over time, we see they are remarkably consistent since 2012. These figures, at least on a state-wide basis, are contrary to the usual narrative, which is that school employment has been slashed, and class sizes are rising rapidly. The pupil-teacher ratios published by KSDE are not the same statistic as class sizes. But if the data shows that the ratio of pupils to teachers is largely unchanged for the past five years and class sizes are rising at the same time, we’re left to wonder what school districts are doing with teachers. And, why are programs being eliminated?

(The relative change in enrollment and employment is not the same in every district. To help Kansas learn about employment trends in individual school districts, I’ve gathered the numbers from the Kansas State Department of Education and present them in an interactive visualization. 67)

Hineman: “Though raising taxes is never easy …”

No. Spenders love to raise taxes. In fact, some legislators warned that the tax hikes are not enough, and that they’ll be back for more. Indeed, projections show spending outpacing revenue in just a few years.

Hineman: “… it was unfortunately the only responsible option available. State government has been cut to the point where there is no reasonable way to reduce spending enough to balance the budget.”

No. One example: The efficiency study commissioned by the legislature recommended savings in the method of acquiring health insurance for public school employees. This was not adopted. Therefore, $47,200,000 in general fund spending is added over what the governor recommended. 89 This was not cutting services or benefits. It was asking school employees to do something differently in order to save money. But, it didn’t happen.

Can Kansas cut spending? There are many states that spend less than Kansas on a per capita basis. 10

Hineman: “Those who parrot the phrase ‘we have a spending problem, not a revenue problem’ have repeatedly failed to offer realistic suggestions for further cuts.”

Hineman is correct in a small way. To balance the budget this year with cuts alone was probably impossible. The lust for spending other people’s money is just too great. But there have been proposals that should have been followed. First, the legislature should have commissioned the efficiency study in 2012 when taxes were cut. That didn’t happen. Then, the legislature should take the efficiency study seriously. But even simple things — like the recommendation of savings through school employee health insurance acquisition reform — are difficult to accomplish, because the spenders don’t want these reforms.

And, in the past there have been responsible plans for reforming spending and the budget. But these plans were not wanted, nor were they realized. 11

Hineman’s criticism shows that it is difficult to cut spending. People become accustomed to other people paying for their stuff. Legislators want to appear to be doing more for their constituents, providing seemingly free stuff while pushing aside the idea of paying for it. And so government grows, at the expense of our liberty and what might have been had the money been left in the productive private sector.

According to KSDE, certified employees include Superintendent, Assoc./Asst. Superintendents, Administrative Assistants, Principals, Assistant Principals, Directors/Supervisors Spec. Ed., Directors/Supervisors of Health, Directors/Supervisors Career/Tech Ed, Instructional Coordinators/Supervisors, All Other Directors/Supervisors, Other Curriculum Specialists, Practical Arts/Career/Tech Ed Teachers, Special Ed. Teachers, Prekindergarten Teachers, Kindergarten Teachers, All Other Teachers, Library Media Specialists, School Counselors, Clinical or School Psychologists, Nurses (RN or NP only), Speech Pathologists, Audiologists, School Social Work Services, and Reading Specialists/Teachers. Teachers include Practical Arts/Vocational Education Teachers, Special Education Teachers, Pre-Kindergarten Teachers, Kindergarten Teachers, Other Teachers, and Reading Specialists/Teachers. See Kansas State Department of Education. Certified Personnel.http://www.ksde.org/Portals/0/School%20Finance/reports_and_publications/Personnel/Certified%20Personnel%20Cover_State%20Totals.pdf. ↩

There are also, according to KSDE, non-certified employees, which are Assistant Superintendents, Business Managers, Business Directors/Coordinators/Supervisors, Other Business Personnel, Maintenance and Operation Directors/Coordinators/Supervisors, Other Maintenance and Operation Personnel, Food Service Directors/Coordinators/Supervisors, Other Food Service Personnel, Transportation Directors/Coordinators/Supervisors, Other Transportation Personnel, Technology Director, Other Technology Personnel, Other Directors/Coordinators/Supervisors, Attendance Services Staff, Library Media Aides, LPN Nurses, Security Officers, Social Services Staff, Regular Education Teacher Aides, Coaching Assistant, Central Administration Clerical Staff, School Administration Clerical Staff, Student Services Clerical Staff, Special Education Paraprofessionals, Parents as Teachers, School Resource Officer, and Others. See Kansas State Department of Education. Non-Certified Personnel Report.http://www.ksde.org/Portals/0/School%20Finance/reports_and_publications/Personnel/NonCertPer%20Cov_St%20Totals.pdf. ↩

“The FY 2018 budget assumes savings of $47.2 million from implementation of Alvarez & Marsal efficiency recommendations to include K-12 health benefit consolidation and sourcing select benefit categories on a statewide basis.” Budget Report, p. 17 ↩

“Add $47.2 million, all from the State General Fund, for removing savings associated with A&M recommendations for health insurance and procurement for FY 2018.” Bill Explanation For 2017 Senate Sub. For House Bill 2002, p. 10. ↩

When reading the writings of former Kansas State Budget Director Duane Goossen, it’s useful to have a guide grounded in reality.

In a look back at the Kansas Legislature this year, former state budget director Duane Goossen has a few opinions. Here are a few, as appeared in the Wichita Eagle, and some counter arguments.

“Kansans, we are done being kicked around.”

No, Kansans are just starting to be kicked around even harder. That’s what higher taxes represent.

“We became famous, the poster state for bad tax policy.”

No, Kansas became the poster state for bad spending policy. Our legislature and governor had several years to find ways to reform spending, but there was not the will to do so. One example: The budget for next year contains $47.2 million in spending because the legislature did not adopt a recommended plan to save money on purchasing health insurance for school employees. That number rises to $89.0 million the following year.

“Kansans wanted their government to work, and wanted public education adequately funded.”

But spending on schools, adjusted for inflation, on a per-student basis, varied very little the past six years. 1 Kansas school employment rose slightly for the current school year, and ratios of employees to pupils fell, also slightly. The ratios of teachers to pupils and certified employees to pupils has been nearly constant in recent years. 2

Another constant refrain is that the state was not spending on highway maintenance. But spending on actual road maintenance programs has risen, with a few ups and downs. (This is spending apart from the sweeps of highway funds.) Additionally, while groups claimed that the state could maintain only 200 miles of roads a year, data from KDOT show that the number of miles maintained has risen for three years, and is well above 2,000 miles per year. 3

“…a discredited ‘trickle down’ tax cut ideology.”

“Trickle down” is not a term that economists use. It has no meaning in economics.

“Certainly, kudos should go to the courageous legislators and legislative leaders who voted to override.”

It is not courageous to raise taxes on anyone, wealthy or not. Courage would have been starting to reform spending five years ago.

“Most citizens prefer not to spend their time thinking about budget and tax policy issues.”

Goossen is correct. Politicians and bureaucrats prefer to work out of the spotlight, especially when raising taxes while showing no resolve to reform spending.

“An even higher percentage of voters expressed concern that the state was not investing enough in education.”

The spending establishment does a very good job convincing people that spending on nearly everything, especially schools, is lower than the reality. As a result, surveys of people across the county, and in Kansas, repeatedly show that the average person has little knowledge of the level of spending in schools and whether spending is rising or falling. 4 This reinforces the previous point.

“Kansas will be climbing out of the Brownback experiment for years.”

Here, Goossen is probably referring to delayed KPERS payments and borrowing from the highway fund. Well. When Goossen was state budget director, the KPERS funding ratio fell year after year. 5 The general fund swept from the highway fund during those years, too. That’s at the same time KDOT was also issuing long-term debt, including some bonds that were interest-only payments for many years. 6 (The state still does this.) To top it off, the budget just passed by the legislature continues sweeps from the highway fund in the amount of $288,297,663 in fiscal year 2018. For fiscal year 2018, the total of the quarterly sweeps is $293,126,335. 7

Printable tables of voting on legislation that raised taxes in Kansas.

The legislation that implemented tax increases in Kansas in 2017 is SB 30, titled “Concerning taxation; income tax, determination of Kansas adjusted gross income, modifications, rates, itemized deductions and credits; sales and compensating use tax, collection and distribution thereof, STAR bonds.” 1

Important action on this bill took place on June 5 and 6. On the first day, each legislative chamber passed a conference committee report. That’s a version of the bill that’s produced by a committee of three members of each chamber. It resolves differences between the bills passed by each chamber. The report is then sent to each chamber for a vote where no amendments are allowed. This report passed both chambers and was sent to the governor.

The governor vetoed the bill, so each chamber then had a chance to override the governor’s veto with a vote of two-thirds of its members. The override was successful, and SB 30 became law.

For the first vote in the House, which passed with a fairly narrow margin of six votes over what is required, a number of Democrats voted Nay, presumably because they thought the tax increase was not large enough. On the vote to override, all Democrats except one voted in favor of higher taxes, and quite a few Republicans switched their votes from opposition to higher taxes to voting in favor of higher taxes.

In the Senate the vote was more consistent. The first vote passed with 26 votes. The second vote, which required 27 votes to be successful, achieved exactly that number, as one Republican senator switched to vote in favor of higher taxes.

In the downloadable and printable pdf tables, notable votes are indicated. For vote 2, the override vote which passed the bill into law, Republican votes are indicated. Additionally, those members who changed their support of higher taxes from vote 1 to vote 2 are indicated. For House of Representatives votes, click here. For an abridged version that prints on one page, click here.

To find who represents you in the Kansas Legislature and other offices, use Kansas Voter View, specifically this form.

Of note, the two votes mentioned above are not the only votes on SB 30. The bill started its legislative journey as a bill titled “An act concerning sales taxation; relating to the Kansas retailers’ sales tax act.” Later all language in the bill was deleted and an entirely new bill was created, although it retained the designation SB 30. Votes taken before that time are not relevant to the final purpose of the bill.

Even though the Kansas Legislature raised taxes, sweeps from the highway fund will continue.

Spending on major road programs in Kansas. Click for larger.Why did the legislature and governor raise taxes in Kansas? One reason cited by many is the need to stop “robbing the highway fund.” This refers to transferring (“sweeping”) money from a fund in the Kansas Department of Transportation to the state’s general fund, where the money is then spent on things besides highways. There was bipartisan agreement that this practice should stop. Highways were falling apart, it was said, even though spending on major road maintenance programs continued at about the same level. 1

The real danger in transferring money from the highway fund is that KDOT borrows money — a lot of money. And instead of that money being spent on long-lived assets like roads and bridges, that borrowed money is spent on current consumption.

But: Guess what? Transfers from the highway fund to the general fund are scheduled to continue for another two years, based on the budget passed by wide margins in both chambers of the legislature. 2

Language in the budget calls for quarterly sweeps totaling $288,297,663 in fiscal year 2018, with the first sweep on July 1, 2017. 3

For fiscal year 2018, the total of the quarterly sweeps is $293,126,335. 4

Transfers from sales tax to Kansas highway fund. Click for larger.There are several ways to look at these transfers. We might look at it as reclaiming from the highway fund some of the sales tax the state collects. That amount has grown. In 2006 the transfer of sales tax revenue to the highway fund was $98,914 million. In 2016 it was $517,698 million, an increase of $418,784 million or 423 percent. 5

But if the legislature wanted to alter the transfer of sales tax, it could have done so by altering the law that specifies the rate of transfer. That promotes transparency.

The budget authorizes the transportation department to borrow up to $400 million in each of the next two fiscal years. There will be pressure to issue those bonds.

Sec. 163 (i). On July 1, 2017, October 1, 2017, January 1, 2018, and April 1, 2018, or as soon thereafter each such date as moneys are available, the director of accounts and reports shall transfer $72,074,415.75 from the state highway fund (276-00-4100-4100) of the department of transportation to the state general fund: Provided, That the transfer of each such amount shall be in addition to any other transfer from the state highway fund of the department of transportation to the state general fund as prescribed by law: Provided further, That, in addition to other purposes for which transfers and expenditures may be made from the state highway fund during fiscal year 2018 and notwithstanding the provisions of K.S.A. 68-416, and amendments thereto, or any other statute, transfers may be made from the state highway fund to the state general fund under this subsection during fiscal year 2018. ↩

Sec. 164 (i). On July 1, 2018, October 1, 2018, January 1, 2019, and April 1, 2019, or as soon thereafter each such date as moneys are available, the director of accounts and reports shall transfer $73,281,583.75 from the state highway fund (276-00-4100-4100) of the department of transportation to the state general fund: Provided, That the transfer of each such amount shall be in addition to any other transfer from the state highway fund of the department of transportation to the state general fund as prescribed by law: Provided further, That, in addition to other purposes for which transfers and expenditures may be made from the state highway fund during fiscal year 2019 and notwithstanding the provisions of K.S.A. 68-416, and amendments thereto, or any other statute, transfers may be made from the state highway fund to the state general fund under this subsection during fiscal year 2019. ↩