-

Political Psychology & Rhetorical Analysis: Trump’s Punchbowl News “Flyout Day” Interview

Read more: Political Psychology & Rhetorical Analysis: Trump’s Punchbowl News “Flyout Day” InterviewA two-track psychological and rhetorical analysis of Trump’s Punchbowl News interview, decoding grandiosity, grievance framing, and the fear-appeal architecture behind his midterm messaging.

-

Trump Says He’d End the Filibuster, Calls Himself a “Great Blocker,” and Warns He Could Be “the Last Republican President”

Read more: Trump Says He’d End the Filibuster, Calls Himself a “Great Blocker,” and Warns He Could Be “the Last Republican President”In a Punchbowl News interview, Trump says he’d end the Senate filibuster, warns he could be the last Republican president, and claims MAGA Inc has $800 million for the midterms.

-

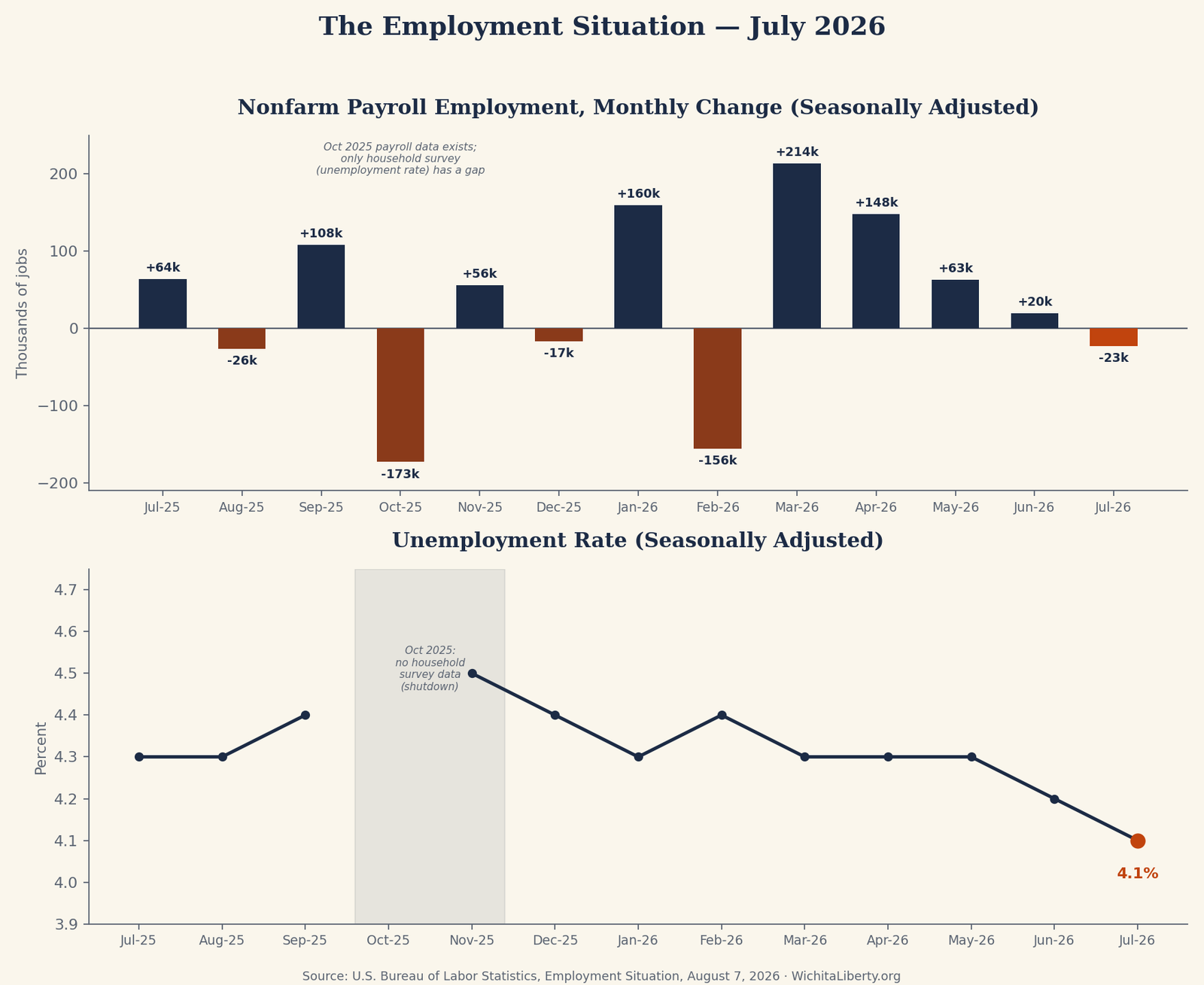

July Jobs Report: Payrolls Fall 23,000 as Labor Market Loses Momentum

Read more: July Jobs Report: Payrolls Fall 23,000 as Labor Market Loses MomentumThe economy lost 23,000 jobs in July, a stunning miss versus forecasts near 83,000. Add in 103,000 in downward revisions to May and June, and the labor market looks far weaker than it did a month ago.

-

Psychological and Rhetorical Analysis: Trump’s Military Spouse Commission Press Conference

Read more: Psychological and Rhetorical Analysis: Trump’s Military Spouse Commission Press ConferenceTrump’s ceremony for military spouses became a case study in grandiosity, victimhood, and press loyalty tests. This two-track analysis decodes the psychological patterns and persuasion techniques beneath the remarks.

-

Trump Signs Order Creating First-Ever Military Spouse Commission — Then Faces Questions on Iran, the Border, and a Fight Over a Leaky Reflecting Pool

Read more: Trump Signs Order Creating First-Ever Military Spouse Commission — Then Faces Questions on Iran, the Border, and a Fight Over a Leaky Reflecting PoolTrump signed an order creating the first-ever Presidential Military Spouse Commission on August 3, then took nearly an hour of questions on Iran, immigration, and DC crime. We break down who said what and fact-check the claims.

-

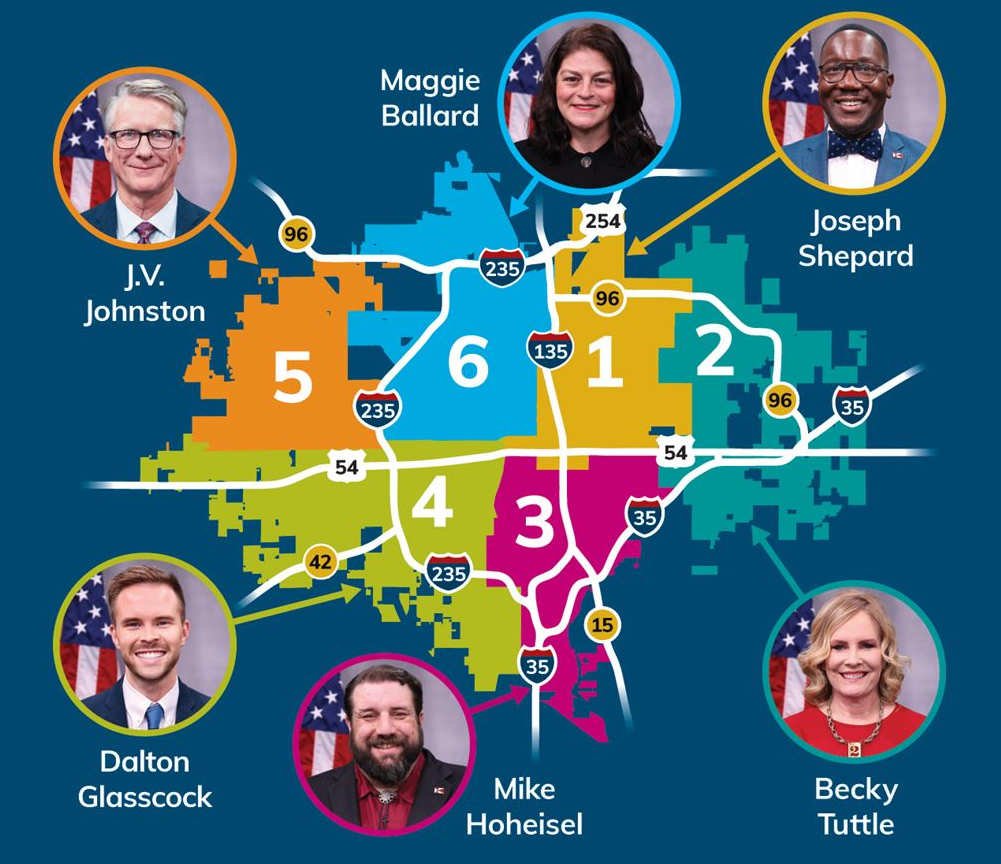

Wichita City Council, June 23, 2026: A Light Agenda, a Bid Question, and a Closed-Door Session

Read more: Wichita City Council, June 23, 2026: A Light Agenda, a Bid Question, and a Closed-Door SessionWichita’s council passed an eminent domain ordinance, nuisance-abatement assessments, and new airport debt in one 7-0 consent vote. Here’s what was authorized — and why the real business happened in the paperwork, not the discussion.

-

Wichita City Council, June 16, 2026: Fire Station Funding, New Panhandling-Adjacent Ordinances, and a Rugby Club Moves Into South Lakes

Read more: Wichita City Council, June 16, 2026: Fire Station Funding, New Panhandling-Adjacent Ordinances, and a Rugby Club Moves Into South LakesThe Wichita City Council approved three federal fire grants, advanced ordinances raising the felony theft threshold and domestic battery sentencing, and discussed encampment and panhandling enforcement. A rugby club also landed a South Lakes lease.

-

Wichita City Council, June 9, 2026: Boeing’s billion-dollar bond, a $233,000 dissent, and the fourth meeting without an answer on Flock cameras

Read more: Wichita City Council, June 9, 2026: Boeing’s billion-dollar bond, a $233,000 dissent, and the fourth meeting without an answer on Flock camerasWichita City Council approved industrial revenue bonds for Boeing’s $1 billion investment and two smaller manufacturers, but a College Hill CID drew the meeting’s only dissent. Flock camera oversight went unanswered for a fourth straight meeting.

-

Sunday Shows Recap: Iran Truce Wobbles, DOJ Turmoil Deepens, and Democrats Brace for a Michigan Reckoning

Read more: Sunday Shows Recap: Iran Truce Wobbles, DOJ Turmoil Deepens, and Democrats Brace for a Michigan ReckoningIran strikes are paused again, Trump’s Justice Department is in open revolt over a $1.8B fund, and Democrats brace for Tuesday’s Michigan Senate primary. Here’s what all five Sunday shows covered.

-

RFK Jr.’s CNN Interview: Fact-Checking His Claims on COVID, Measles

Read more: RFK Jr.’s CNN Interview: Fact-Checking His Claims on COVID, MeaslesHHS Secretary RFK Jr. clashed with CNN’s Dana Bash over COVID, measles, and autism research. We fact-check his most disputed claims, one by one, against the evidence.

-

Prosecutor, Not Panel: A Psychological and Rhetorical Analysis of the Republican Majority at the Fauci Hearing

Read more: Prosecutor, Not Panel: A Psychological and Rhetorical Analysis of the Republican Majority at the Fauci HearingEight Republican senators questioned Fauci at the July 2026 Senate hearing, ranging from document-driven skepticism to open contempt. This piece maps the shared psychological patterns and persuasion techniques across the group.

-

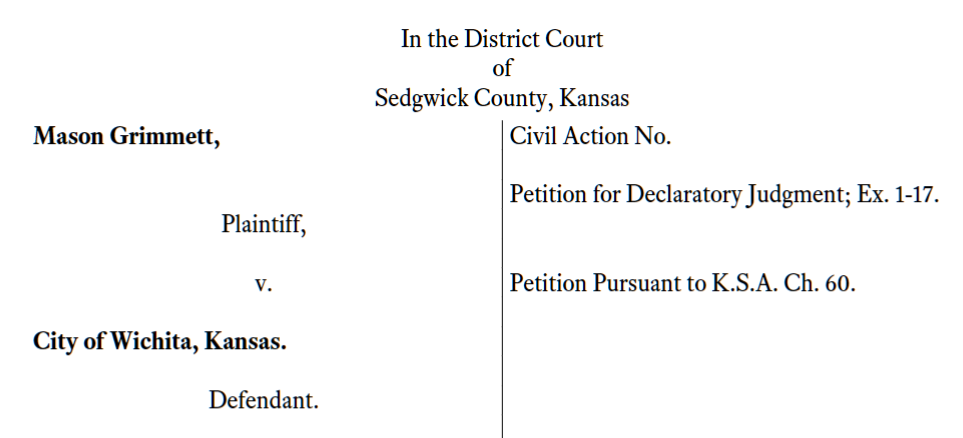

A Wichita Man Sues to Shut Down the City’s License Plate Camera Network: What the Lawsuit Says, and Whether It Can Win

Read more: A Wichita Man Sues to Shut Down the City’s License Plate Camera Network: What the Lawsuit Says, and Whether It Can WinMason Grimmett says Wichita’s warrantless license plate reader network tracks every driver in the city without a warrant. This analysis breaks down his legal theories, the precedents on both sides, and who is likely to win.