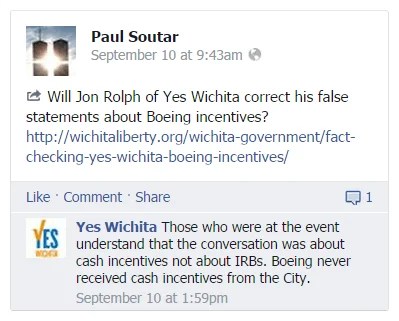

Supporters of the proposed Wichita sales tax contend that the millions in incentives Boeing received were not cash. That’s true — they were more valuable than cash.

At a forum on the proposed Wichita sales tax on September 9, 2014, “Yes Wichita” co-chair Jon Rolph told the audience “The Boeing incentive thing? The city never gave Boeing incentives. They didn’t take our incentive money and run.” As explained at Fact-checking Yes Wichita: Boeing incentives, the claim that the ?city never gave Boeing incentives? must be astonishing news to the Wichita city officials who dished out over $600 million in subsidies and incentives to the company.

First, it’s interesting that the person commenting on behalf of “Yes Wichita” was able to read the minds of the audience members. That’s a neat trick. But let’s talk about something more important — the confusion that often surrounds economic development incentives.

“Yes Wichita” contends that although Boeing received an estimated $657,992,250 in property tax abatements over several decades, this doesn’t count as “cash incentives” because it wasn’t given to Boeing in the form of cash.

“Yes Wichita” is correct, in a way. As a result of the City of Wichita’s issuance of industrial revenue bonds, Boeing didn’t receive cash from the city. Instead, the benefits the city initiated on Boeing’s behalf are more valuable to the company than receiving an equivalent amount of cash.

![]() According to IRS guidelines, “tax incentives, whether in the form of an abatement, credit, deduction, rate reduction or exemption, simply reduce the tax imposed by state or local governments.” The IRS says these incentives do not count as income. Therefore, Boeing did not pay income taxes on these benefits, as it would have if the city gave the company cash.

According to IRS guidelines, “tax incentives, whether in the form of an abatement, credit, deduction, rate reduction or exemption, simply reduce the tax imposed by state or local governments.” The IRS says these incentives do not count as income. Therefore, Boeing did not pay income taxes on these benefits, as it would have if the city gave the company cash.

The claim by the “Yes Wichita” group — that tax abatements don’t count as cash incentives — is characteristic of the way economic development incentives are justified. Instead of passing out cash, it’s more common that government uses abatements, credits, tax increment financing, investment in training and infrastructure, or exemptions. Many of these programs are confusing to citizens, and perhaps also to the elected officials who approve them. This allows government to shroud the economic realities of the transaction, and “Yes Wichita” is contributing to this confusion.