Tag: Wichita city council

-

Wichita City Council Meeting February 27, 2026: ParkMobile Controversy, Microsoft Contract, and Economic Justice Debate

The Wichita City Council convened in regular session with all seven members present. Business included a pointed public comment about the City’s transition to ParkMobile for City Hall parking, a discussion about the City’s Microsoft Office 365 contract and the limitations of negotiating with large tech vendors, a series of unanimous consent agenda votes, council…

-

Wichita City Council Meeting — February 17, 2026: Full Coverage

Full coverage of the Wichita City Council meeting on February 17, 2026, including Q4 financial report warnings, fire station mold crisis, stormwater rate increase, affordable housing funding, and summer youth employment.

-

Claude AI Looks at an Election

On March 3, 2026, the City of Wichita held a special election. I asked Claude, a popular AI platform, to examine the election results.

-

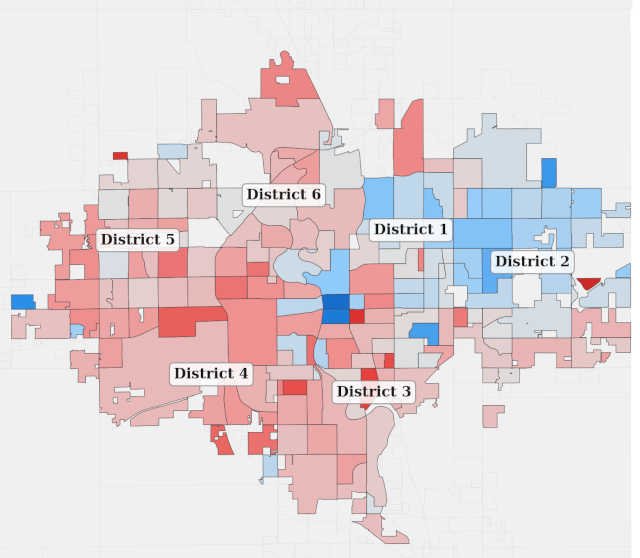

Wichita Sales Tax Election, March 3, 2026

Precinct results for Wichita Sales Tax Election, March 3, 2026

-

Wichita City Council Adopts Sales Tax Guardrails in Marathon Evening Session | February 10, 2026

The Wichita City Council held a marathon evening session February 10, adopting a unanimous framework of financial guardrails for the proposed 1% sales tax before the March 3 vote. Twenty-three residents testified, and the Webb Road widening passed 6-1.

-

Wichita City Council Feb. 3, 2026: Ad Controversy, Zoning Fight on 37th Street, Water Meter Project

Full coverage of the February 3, 2026 Wichita City Council meeting — including a heated public comment over a campaign advertisement, a contentious 37th Street zoning decision, water meter replacement funding, and community announcements.

-

Wichita Council January 20, 2026: Water Plant Issues Dominate

The Wichita City Council convened on January 20, 2026, for a marathon session that lasted from 9:00 AM until adjournment at 12:27 PM. The meeting was dominated by extensive discussion of the troubled Wichita Water Works project, revealing that liquidated damages were not extended past the September 2024 substantial completion date—a detail not previously disclosed…

-

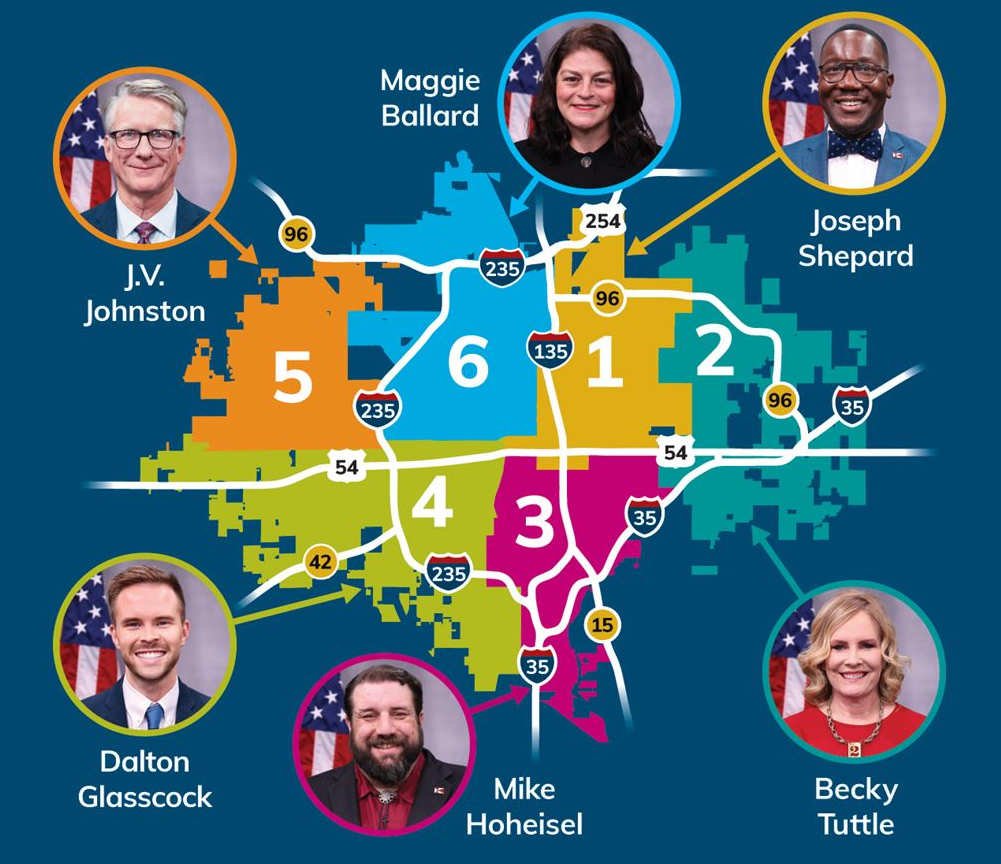

Wichita City Council Elects Glasscock Vice Mayor Amid Sales Tax Controversy – January 13, 2026

Dalton Glasscock elected Wichita Vice Mayor for 2026 as Council debates delaying March 3 sales tax vote. Mayor Wu’s motion to hold special meeting fails 3-4. Full coverage of park funding, transit issues, and emergency communications.

-

Wichita Council Votes 5-2 to Keep March Sales Tax Election

On January 14, 2026, the Wichita City Council voted 5-2 to proceed with a March 3 sales tax election despite new information about increased costs and polling disruptions. The special meeting, called by Mayor Lily Wu, featured passionate testimony from 22 speakers about the proposed $850 million, 7-year sales tax. Election Commissioner Laura Rainwater revealed…

-

Wichita City Council Selects New City Manager After 16-Year Era: November 25, 2025 Meeting Analysis

In a historic November 25, 2025 session, Wichita City Council voted 5-2 to negotiate with Dennis Marstall as next City Manager, ending Robert Layton’s 16-year tenure. Council Member Johnson raised process concerns while supporting future search. Meeting also featured housing safety advocacy and cemetery preservation updates.

-

New City Manager, Settlement Drama, and Student Advocates: Wichita City Council’s First Meeting of 2026

Wichita City Council’s first 2026 meeting featured dramatic settlement negotiations, powerful homelessness testimony, impressive student healthcare advocacy, and the introduction of new City Manager Dennis Marstall. The council successfully negotiated to recover the full $219,000 owed by Genesis Health Club.

-

Wichita City Council Meeting: December 2, 2025

The Wichita City Council convened on Tuesday, December 2, 2025, for a comprehensive session addressing critical issues including the approval of a new City Manager, significant water and sewer rate adjustments, union contract negotiations, and affordable housing initiatives. The meeting featured passionate public testimony on food deserts and homelessness, the approval of Dennis Marstall as…