Tag: Taxation

-

Wichita Sales Tax Election, March 3, 2026

Precinct results for Wichita Sales Tax Election, March 3, 2026

-

Wichita City Council Elects Glasscock Vice Mayor Amid Sales Tax Controversy – January 13, 2026

Dalton Glasscock elected Wichita Vice Mayor for 2026 as Council debates delaying March 3 sales tax vote. Mayor Wu’s motion to hold special meeting fails 3-4. Full coverage of park funding, transit issues, and emergency communications.

-

The Biggest Mistake in the Wichita Sales Tax Proposal Is . . .

Dion Lefler argues that Wichita’s proposed sales tax fails as property tax relief because money collected from nonresidents would largely flow back out of the city to absentee property owners.

-

Wichita Forward Moves to Quiet Sales Tax Opposition, Won’t Release Survey Data

Wichita Forward limited public criticism of its proposed 1 percent sales tax by restricting discussion at a forum and refusing to release polling data, drawing complaints from residents and city council members about transparency.

-

Supreme Court Hears Historic Arguments on Trump Tariffs: Can Presidents Tax Without Congress?

Can a president tax Americans without Congress? The Supreme Court just heard explosive arguments on Trump’s tariffs – with justices asking if a future president could declare a climate emergency to impose massive taxes. One justice called it a “one-way ratchet” where Congress would never get its constitutional power back. The stakes: trillions in trade…

-

Fact-Check: Trump’s Claim About Eliminating Social Security Taxes

The claim contains a sweeping overgeneralization by stating “NO TAXES ON SOCIAL SECURITY” when the actual effect is far more limited and nuanced. The new senior deduction will benefit some seniors but not all, and even for those who benefit, the mechanism is not an elimination of Social Security taxation but rather a general deduction…

-

The Employment and Wage Effects of Trump’s Steel Tariffs

Research on the Trump administration’s 2018-2020 steel tariffs reveals significant negative net employment effects despite modest gains in steel production jobs. While steel workers experienced some wage increases, the broader economic impact included substantial job losses in steel-using industries and higher costs for consumers.

-

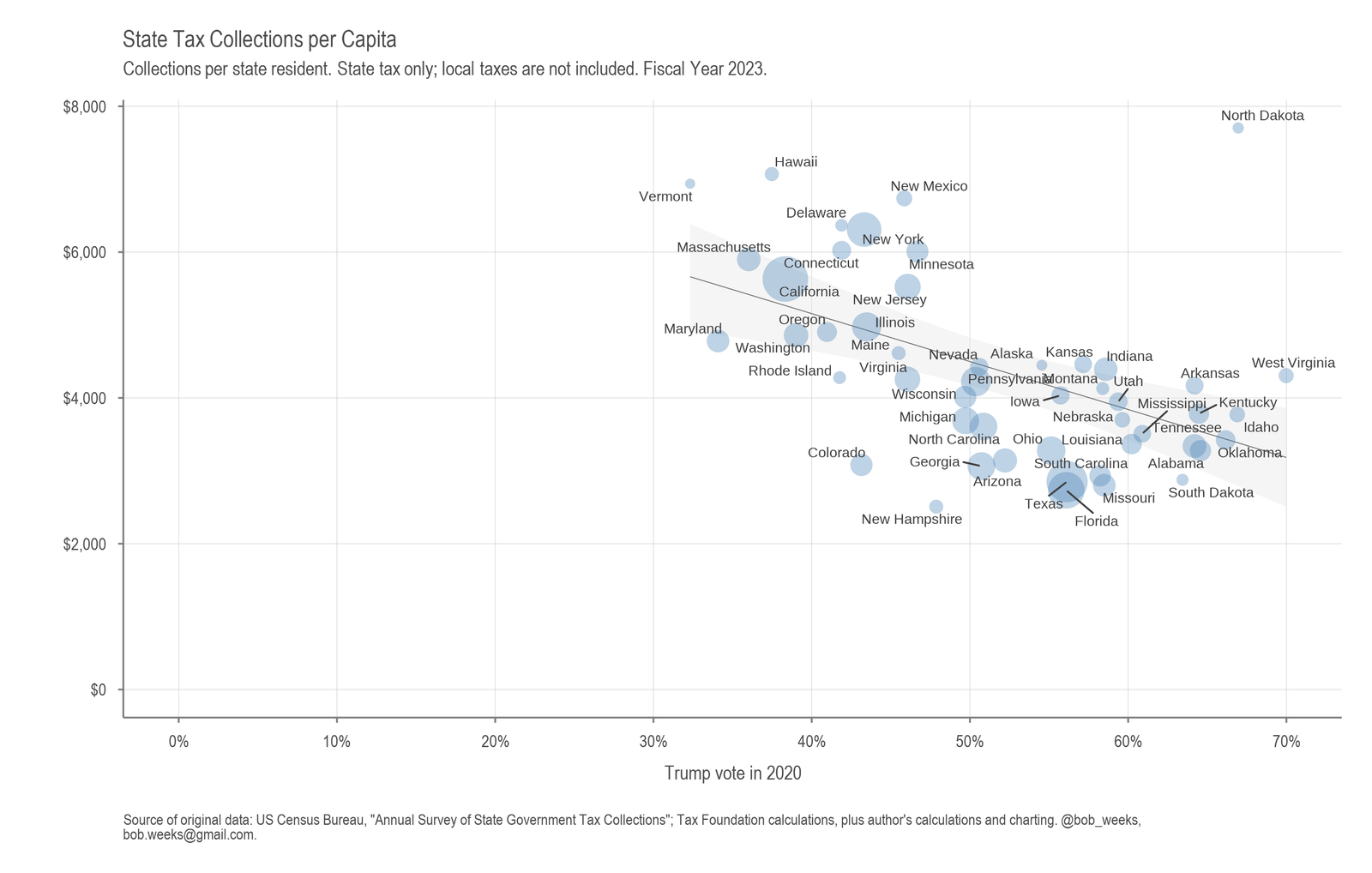

State Tax Collections

Using data from Tax Foundation, I examined state political sentiment and state tax collections.

-

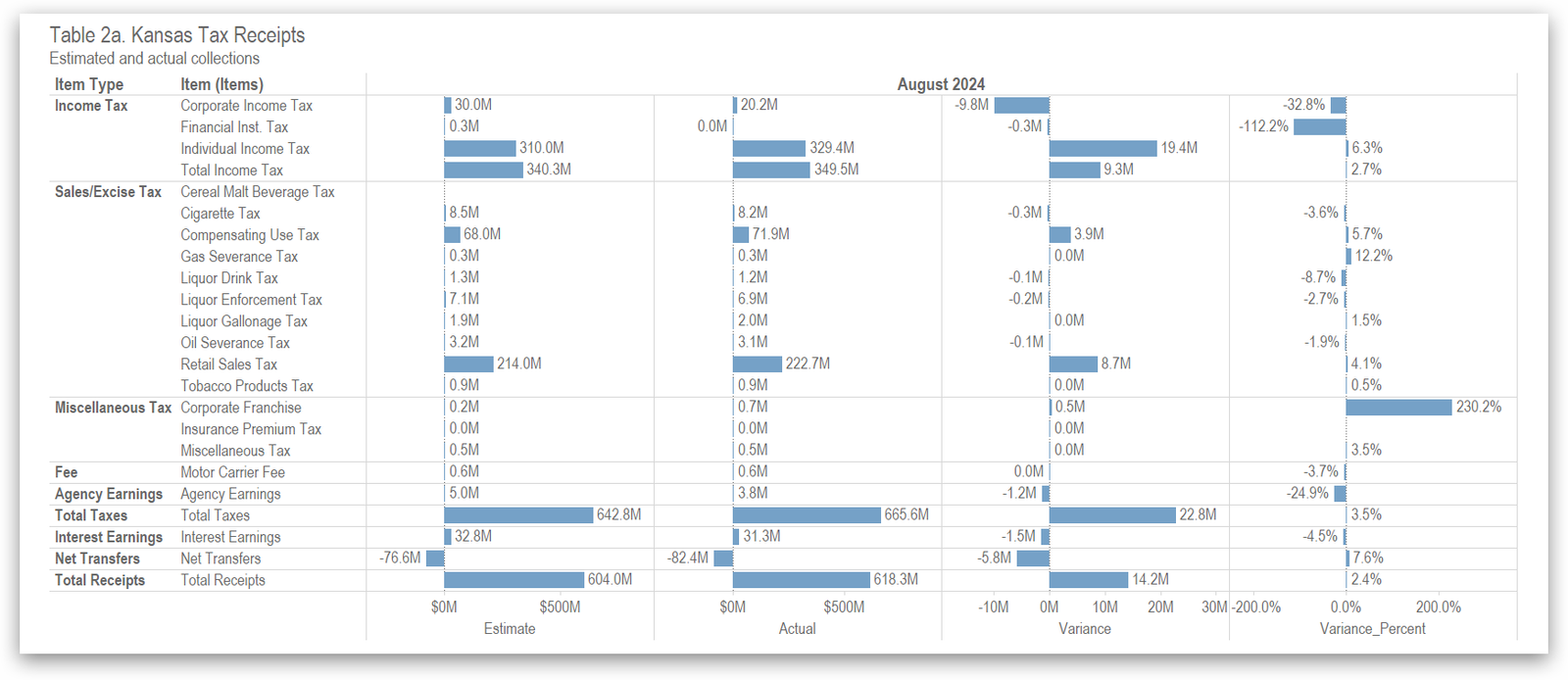

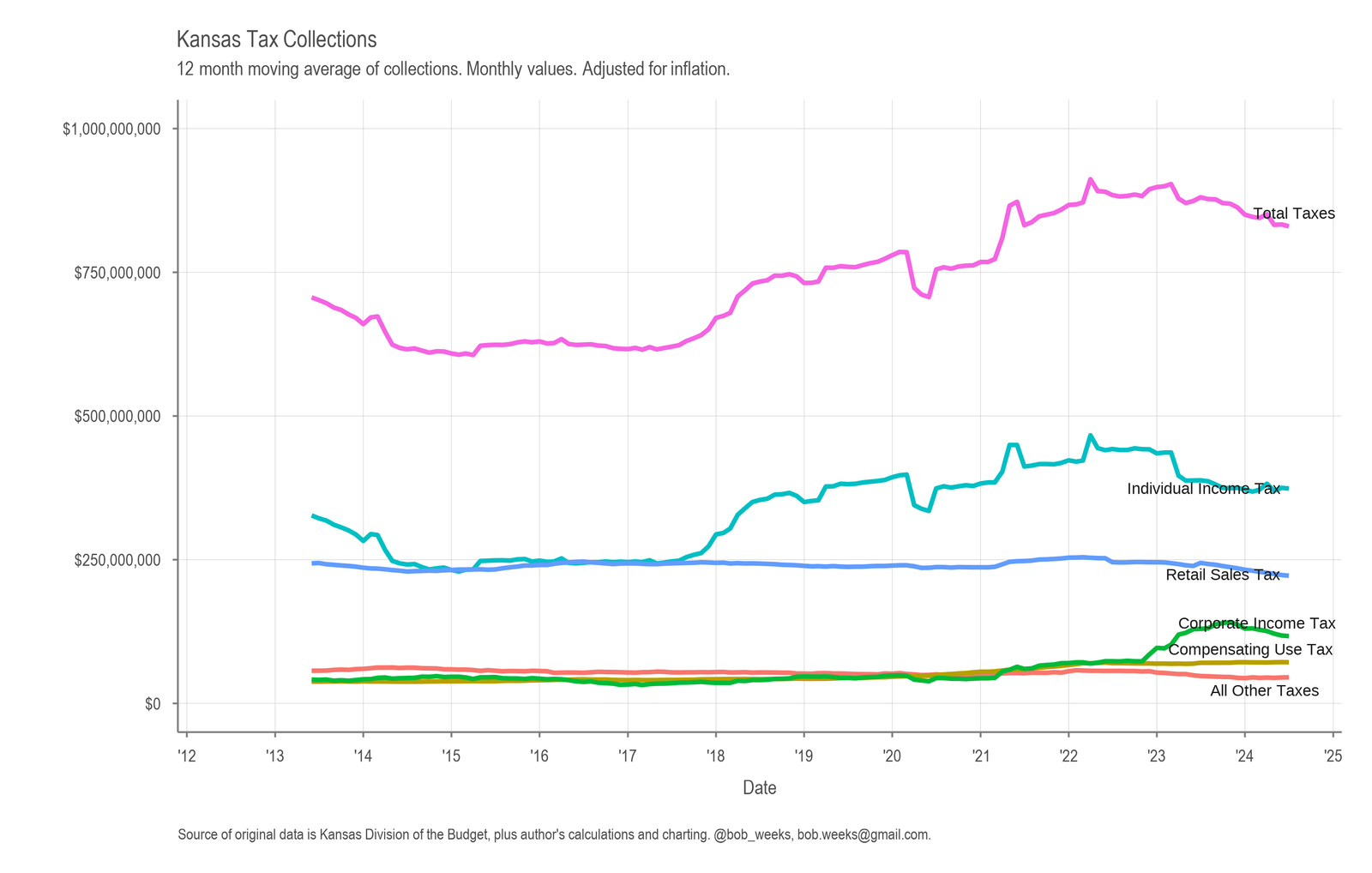

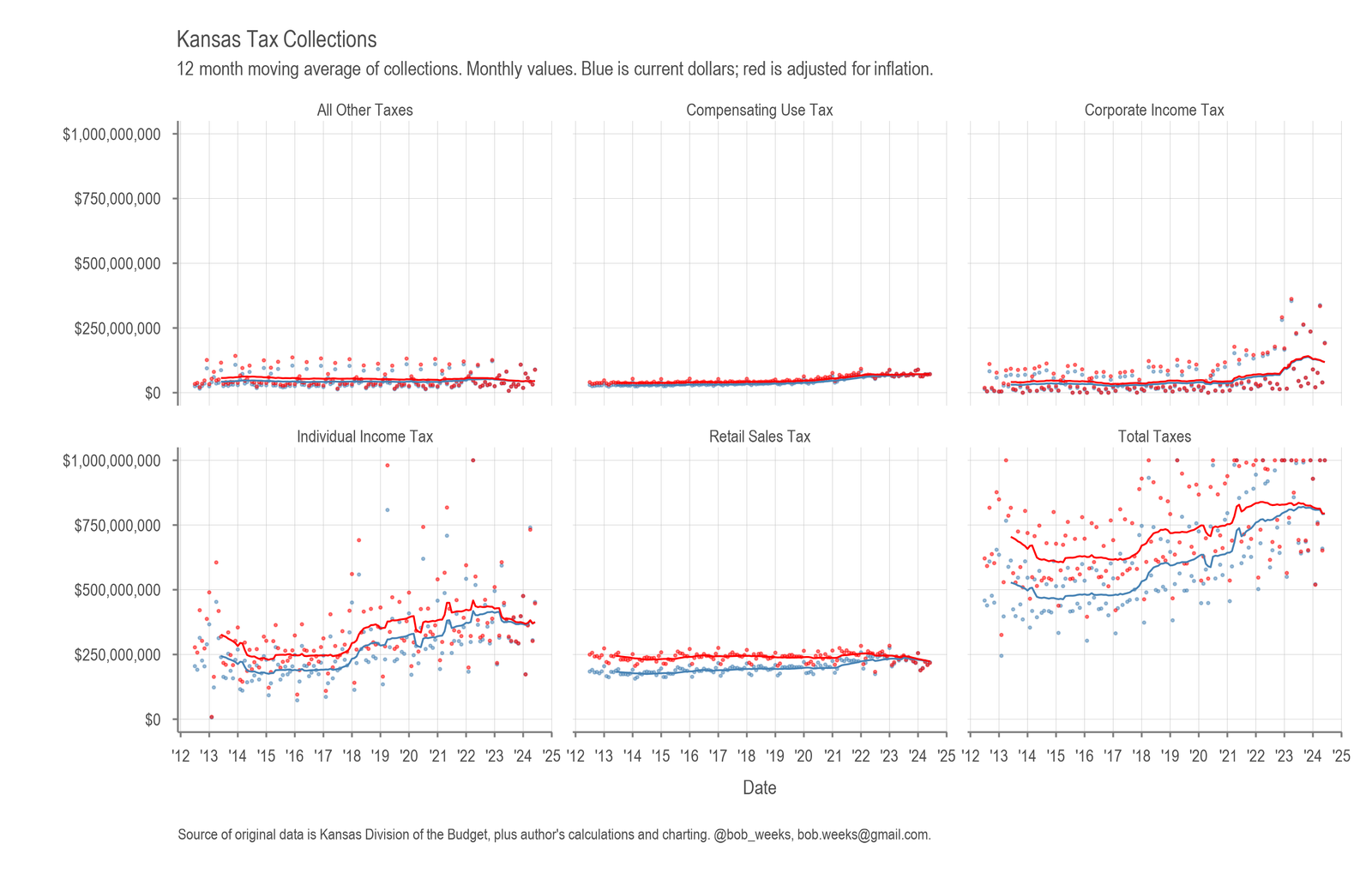

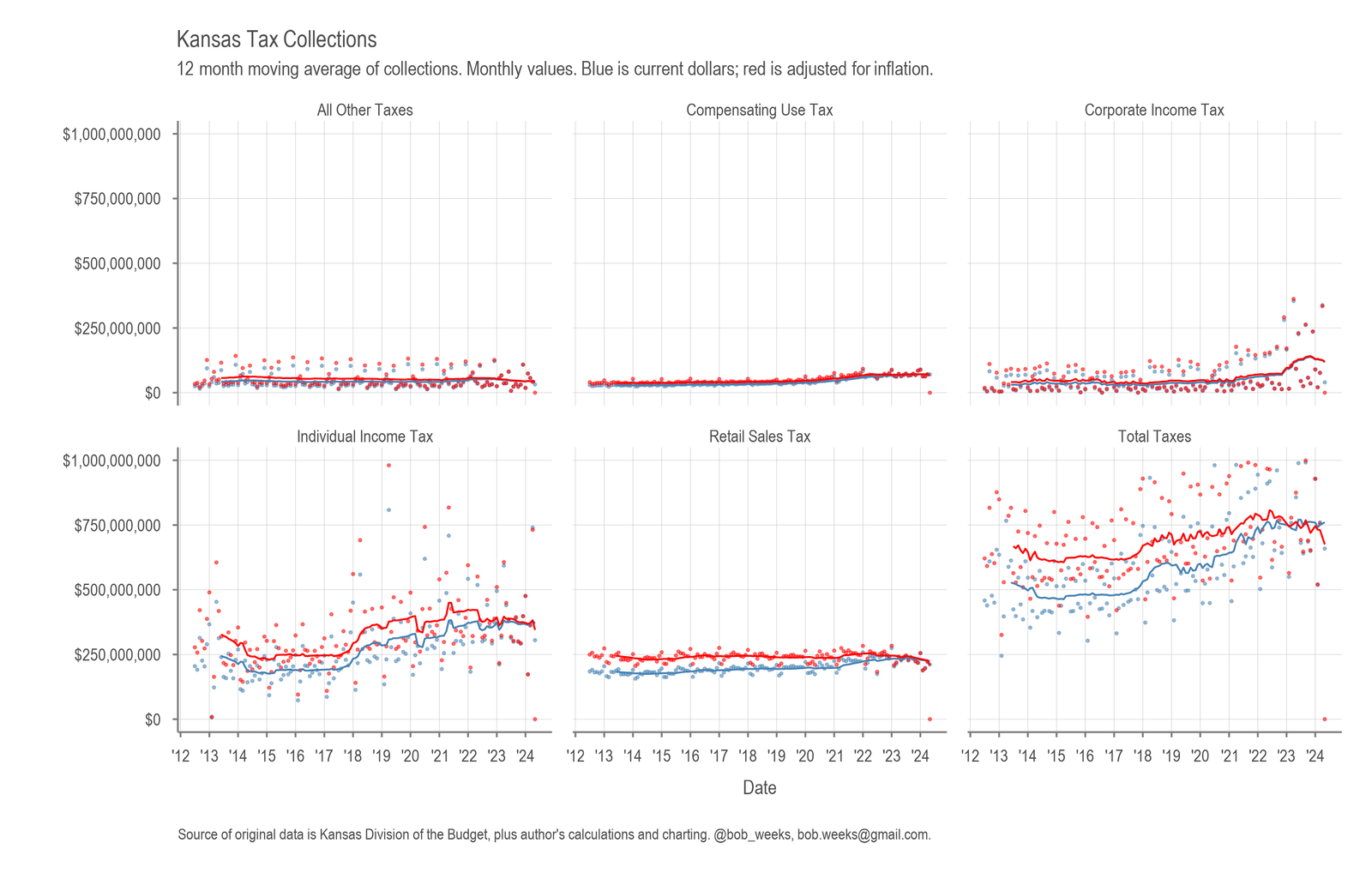

Kansas Tax Revenue, August 2024

For August 2024, Kansas tax revenue was 4.0 percent higher than August 2023, and 3.5 percent higher than estimated.

-

Kansas Tax Revenue, July 2024

For July 2024, Kansas tax revenue was 3.0 percent lower than July 2023, and 1.0 percent less than estimated.

-

Kansas Tax Revenue, June 2024

For June 2024, Kansas tax revenue was 3.9 percent higher than June 2023, and 2.4 percent higher than estimated. For the just-completed fiscal year, collections were lower by 1.5 percent than the previous year, and 2.0 percent lower than estimated.

-

Kansas Tax Revenue, May 2024

For May 2024, Kansas tax revenue was 23.1 percent lower than May 2023, and 22.7 percent lower than estimated.