Tag: Tax abatements

-

Wichita presents industrial revenue bonds

A presentation by the City of Wichita regarding IRBs is good as far as it goes, which is not far enough.

-

Freestanding emergency room in Wichita closes

The conversion of a medical facility should receive city scrutiny due to tax breaks granted based on its original use.

-

Missing from Wichita city documents: Sales tax

It would be simple for the City of Wichita to include additional relevant information regarding economic development incentive decisions.

-

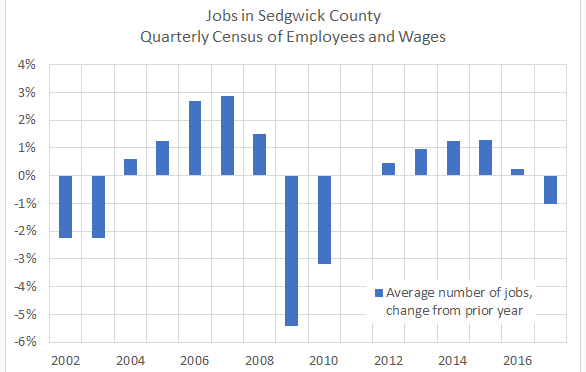

Sedgwick County tax exemptions

Unlike the City of Wichita, Sedgwick County has kept track of its tax exemptions.

-

Wichita business press needs to step up

If a newspaper is going to write a news story, it might as well take a moment to copy and paste information from a city council agenda packet. Especially when what is missing from the story is perhaps the most important information.

-

How much will this cost Wichita taxpayers?

How much, if anything, do tax abatements cost?

-

Sedgwick County’s David Dennis on economic development

Following the Wichita Mayor, the Chair of the Sedgwick County Commission speaks on economic development.

-

Spirit expands in Wichita

It’s good news that Spirit AeroSystems is expanding in Wichita. Let’s look at the cost.

-

Sales tax incentives yes, but no relief on grocery sales tax

Is it equitable for business firms to pay no sales tax, while low-income families pay sales tax on groceries?

-

Cash incentives in Wichita, again

The City of Wichita says it does not want to use cash incentives for economic development. But a proposal contains just that.

-

Won’t anyone develop in downtown Wichita without incentives?

Action the Wichita City Council will consider next week makes one wonder: If downtown Wichita is so great, why does the city have to give away so much?

-

In Wichita, developer welfare under a cloud

A downtown Wichita project receives a small benefit from the city, with no mention of the really big money.