Tag: Interventionism

-

Swamp refilling itself

Although there has been progress, cronyism and the swamp may be renewed in Washington.

-

More Wichita planning on tap

We should be wary of government planning in general. But when those who have been managing and planning the foundering Wichita-area economy want to step up their management of resources, we risk compounding our problems.

-

More TIF spending in Wichita

The Wichita City Council will consider approval of a redevelopment plan in a tax increment financing (TIF) district.

-

Tax benefits for education don’t increase education

Here’s evidence of a government program that, undoubtedly, was started with good intentions, but hasn’t produced the intended results.

-

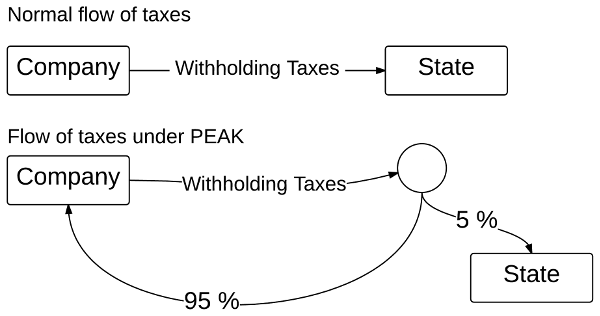

PEAK, or Promoting Employment Across Kansas

PEAK, a Kansas economic development incentive program, redirects employee income taxes back to the employing company.

-

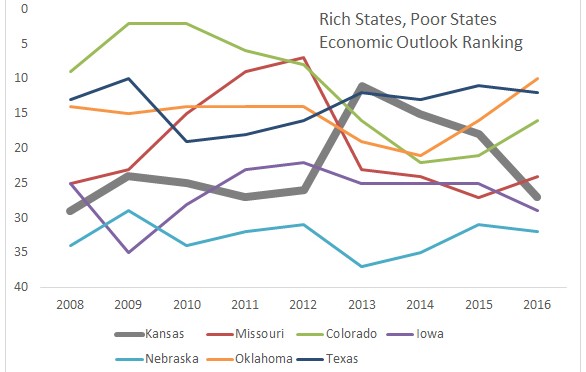

Rich States, Poor States, 2107 edition

In Rich States, Poor States, Kansas improves its middle-of-the-pack performance, but continues with a mediocre forward-looking forecast.

-

Kansas economic development programs

Explaining common economic development programs in Kansas.

-

Rich States, Poor States, 2106 edition

In Rich States, Poor States, Kansas continues with middle-of-the-pack performance, and fell sharply in the forward-looking forecast.

-

Wichita TIF district disbands; taxpayers on the hook

A real estate development in College Hill was not successful. What does this mean for city taxpayers?

-

Bombardier can be a learning experience

The unfortunate news of the cancellation of a new aircraft program can be a learning opportunity for Wichita.

-

Export-Import Bank threatens a revival

Business groups and government agencies usually favor Ex-Im. Free-market and capitalism advocacy groups are almost universally opposed.

-

WichitaLiberty.TV: Jeffrey Tucker and ‘Bit by Bit: How P2P Is Freeing the World’

Jeffrey Tucker talks about his most recent book “Bit by Bit: How P2P Is Freeing the World” and how Bitcoin and other distributed technologies are affecting the world.