Tag: Federal Reserve System

-

Bessent Briefing: Trump Accounts, Iran Talks, Economy

Treasury Secretary Scott Bessent unveiled the Trump Accounts children’s savings app, outlined three firm red lines in Iran nuclear talks, and disclosed his first meeting with new Fed Chair Warsh — all in one jam-packed White House briefing.

-

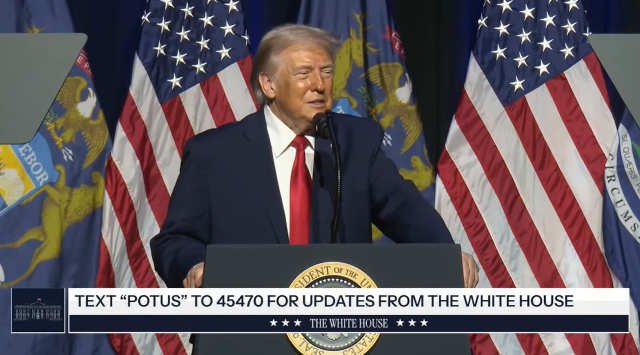

Trump Returns to Detroit Economic Club: Defends Economic Record, Attacks Welfare Fraud, and Promises Major Healthcare Changes

President Trump addressed the Detroit Economic Club on January 13, 2026, claiming historic economic achievements including $18 trillion in new investment and record-low inflation. The speech featured major announcements on welfare fraud enforcement targeting Somali communities, upcoming healthcare reforms with drug price reductions up to 600%, and housing affordability policies to be detailed at Davos,…

-

Kansas and Wichita quick takes: Wednesday June 29, 2011

Today: We have tried that before; How can the Fed be so clueless?; Deficit is probably worse than thought; Blue pill or red pill?

-

Quantitative easing: another round?

Another round of expansionist monetary policy in the form of quantitative easing 3 could be on the way.

-

Kansas and Wichita quick takes: Sunday March 13, 2011

Today: Wichita city council this week; how attitudes can differ; private property and the price system; toward a free market in education; are lottery tickets like a state-owned casino?; money, banking and the Federal Reserve; Wichita-area legislators to meet public; Pompeo to meet with public; losing the brains race; Teachers unions explained.

-

Response to economic crisis to be subject of Wichita lecture

Tomorrow night at Friends University Dr. Brian Domitrovic of Sam Houston State University will speak on some of the key people and principles in his book Econoclasts: The Rebels Who Sparked the Supply-Side Revolution and Restored American Prosperity.

-

Money, Banking and the Federal Reserve

Events over the last year have placed our nation’s monetary system in focus. Or, at least it should be in sharp focus, as U.S. monetary policy and the Federal Reserve System bear much responsibility for the financial crisis and the accompanying recession. Few politicians, Ron Paul being one, are looking in the right places for…

-

It’s time to audit the Federal Reserve Bank

The secretive FR [Federal Reserve] is a monetary oligarchy and an unelected monopoly that has control of credit, interest, volume and value of our currency. Until the people regain control of their money, bankers and not the government, will control the situation and our property,” says Al Terwelp, Vice Chair of the Libertarian Party of…