Tag: Economics

-

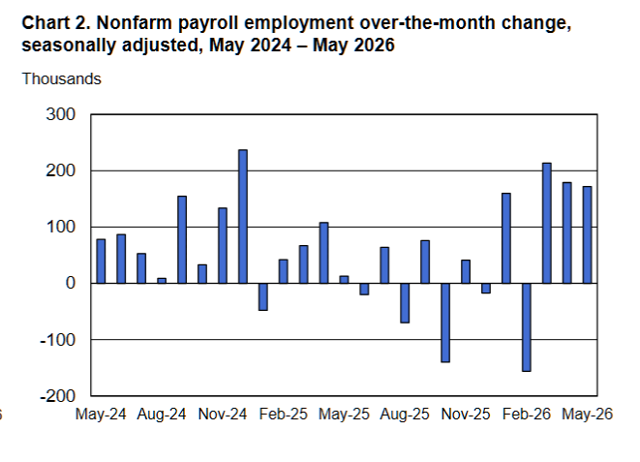

May 2026 Jobs Infographic

The May 2026 jobs report delivered a major upside surprise: 172,000 jobs added against forecasts of 80,000–105,000.

-

May 2026 Jobs Report: Economy Adds 172,000 Jobs

The May 2026 jobs report delivered a major upside surprise: 172,000 jobs added against forecasts of 80,000–105,000. Prior months were also revised up by a combined 93,000. Here’s a plain-English breakdown of who’s hiring, who’s losing ground, and what it means for interest rates.

-

Hassett Defends Economy, Touts Tax Cuts, and Vouches for Pulte as DNI in White House Gaggle

Trump economic adviser Kevin Hassett made sweeping economic claims outside the West Wing on June 2. Our fact-check finds his GDP figure off by 2.5×, his $3,000 wage gain disputed, and his Bill Pulte DNI defense dodges credentials.

-

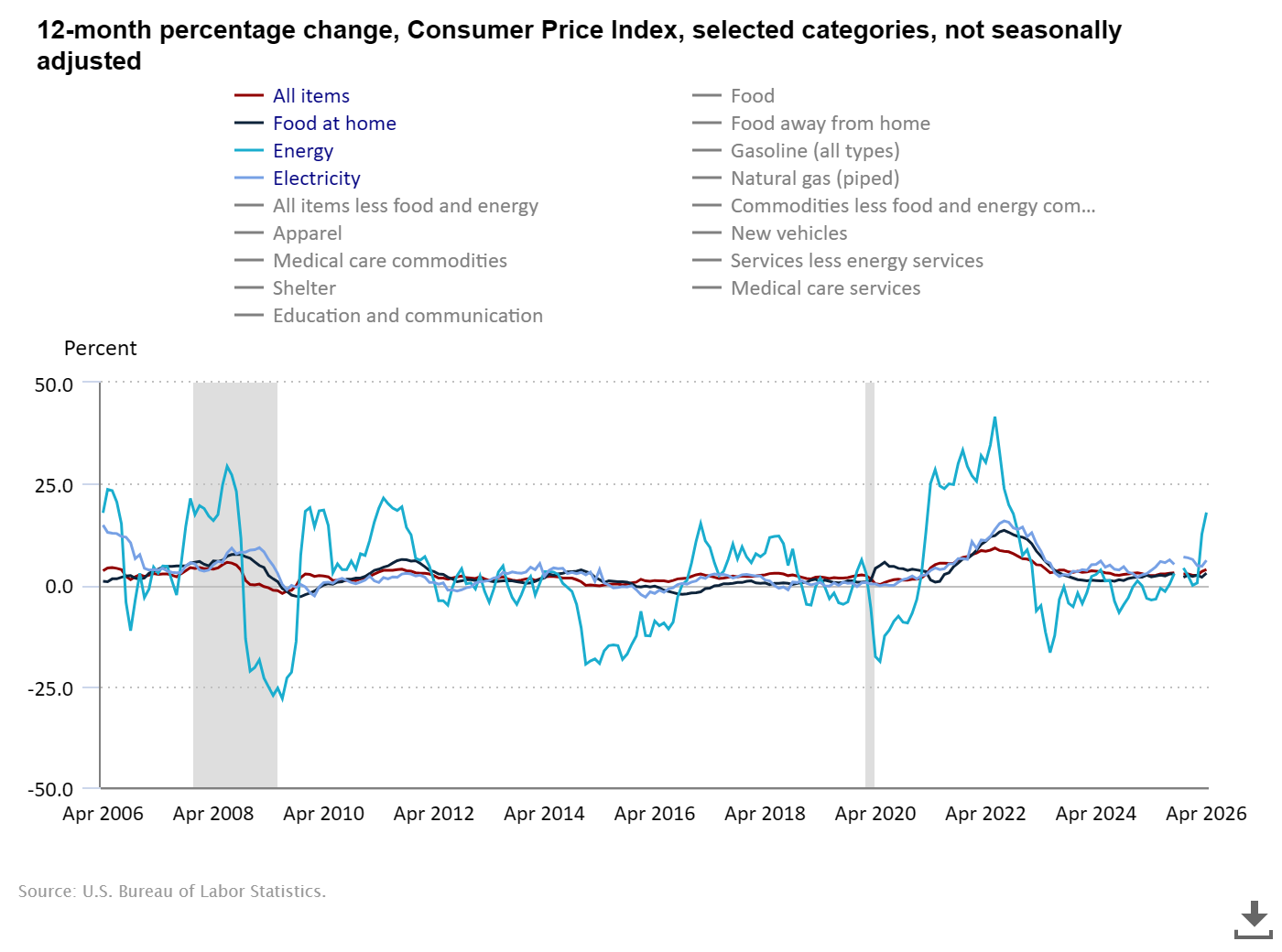

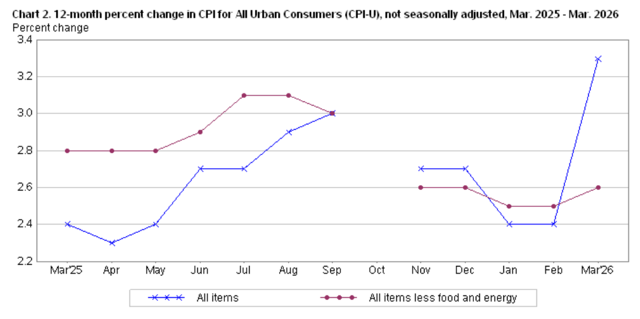

Inflation Accelerated in April 2026: Energy Prices Drive CPI to 3.8% — Highest in Three Years

Inflation accelerated sharply in April 2026, with consumer prices rising 3.8% over the past year — the fastest pace since May 2023. Energy costs, led by a 28.4% annual surge in gasoline, drove more than 40 cents of every dollar of monthly price growth.

-

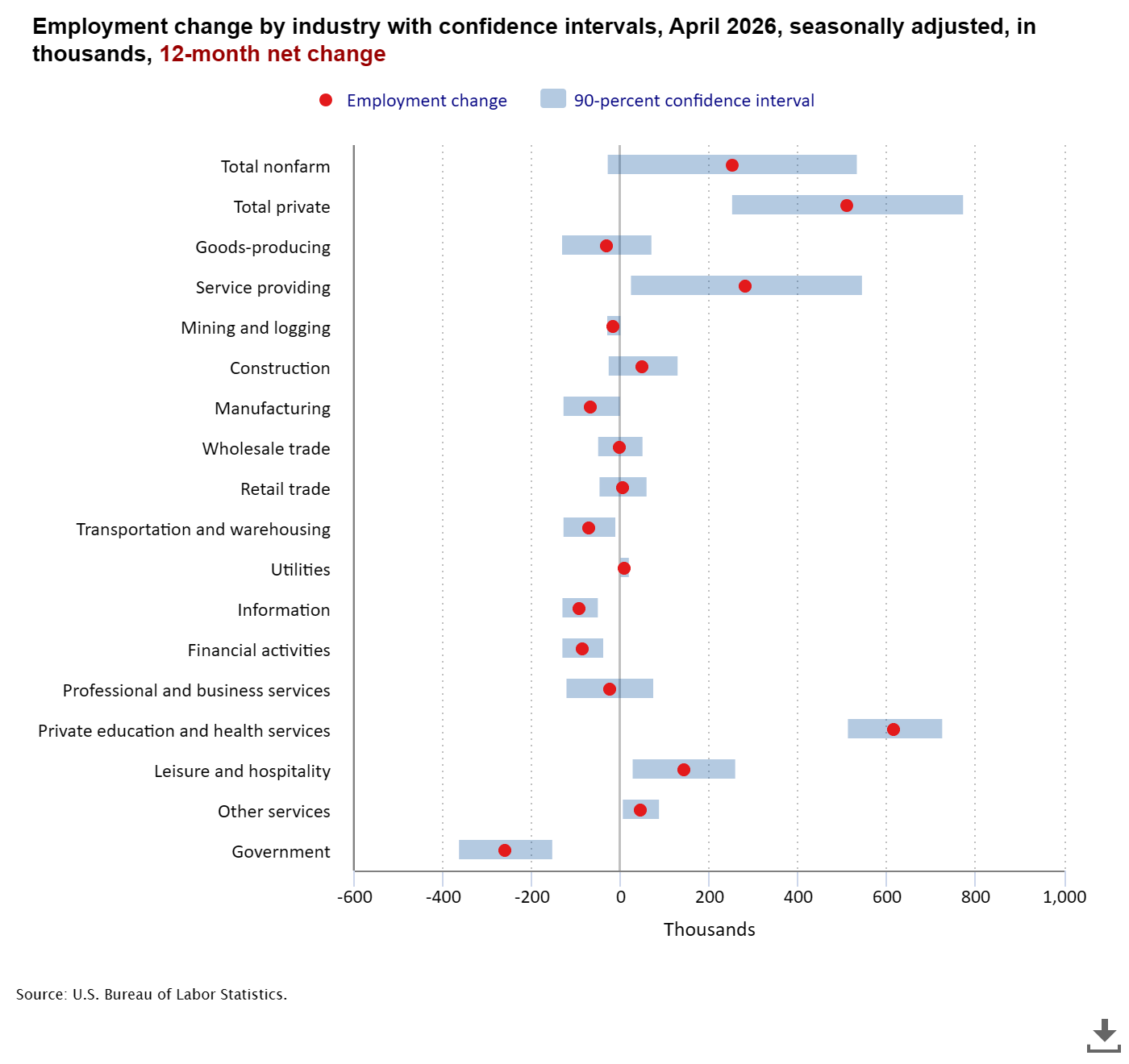

April 2026 Jobs Report: Hiring Slows Sharply as Federal Cuts Mount

The April 2026 jobs report delivered a clear warning: U.S. hiring is slowing fast. Employers added only 115,000 jobs last month, well short of expectations, while the three-month average has tumbled to just 48,000 — the weakest sustained pace in years.

-

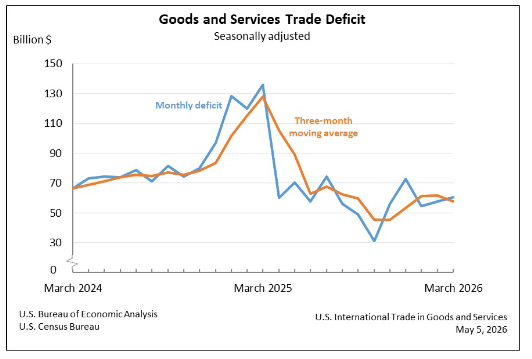

Trade Deficit Rose to $60.3 Billion in March, but the Year-Over-Year Story Is Dramatic

The U.S. trade deficit widened modestly to $60.3 billion in March 2026, but the headline number obscures a remarkable year-over-year story: the gap is 55% smaller than a year ago, as importers no longer need to front-run tariffs.

-

Kevin Hassett Fact-Check: Iran War Claims & Economic Data

White House economic advisor Kevin Hassett made a string of economic claims on Face the Nation — some accurate, some misleading, and one outright false. This fact-check grades each one against primary sources, from IRS filing data to historical GDP records.

-

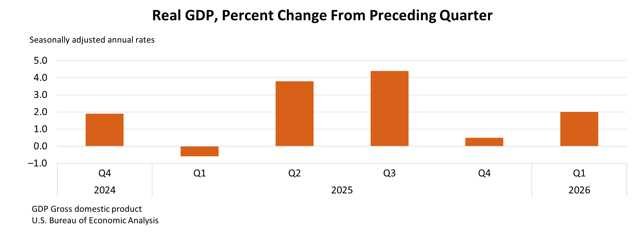

U.S. GDP Q1 2026: Growth Rebounds but Inflation Surges to 4.5%

The U.S. economy appears to have rebounded strongly in early 2026, growing at a 2.0% annual rate after nearly stalling in late 2025. But beneath that headline lies a harder story: inflation is surging back, consumers are pulling back, and much of the growth may be a statistical mirage.

-

Inflation Surged in March 2026 as Gasoline Prices Drove the Biggest Monthly Jump in Nearly Four Years

Inflation surged 0.9% in March — the biggest monthly jump since June 2022 — as gasoline prices posted their largest single-month increase on record. The annual rate climbed to 3.3%, well above February’s 2.4%.

-

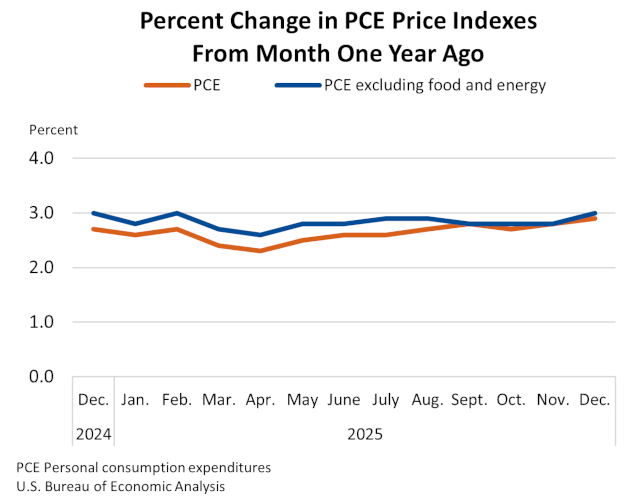

December 2025 PCE Report: Inflation Ticks Up, Savings Drop, and Spending Holds On

The BEA’s December 2025 Personal Income and Outlays report shows inflation rising to 2.9% annually while Americans dip into savings to keep spending. Here’s what it means for your wallet and the Fed’s next move.

-

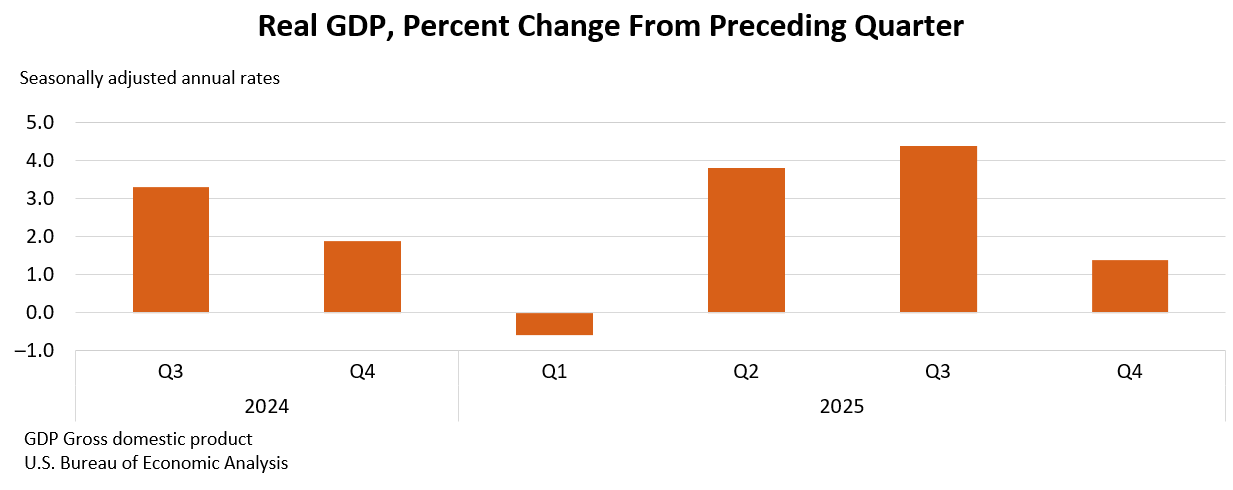

Q4 2025 GDP: Why the 1.4% Growth Rate Is Misleading — And What the Real Number Is

The government reported 1.4% GDP growth for Q4 2025, a sharp drop from summer’s 4.4% pace. But a six-week federal shutdown distorted the numbers. Strip that out and the private economy grew 2.4% — a healthy pace. Here’s a plain-English breakdown of what really happened.

-

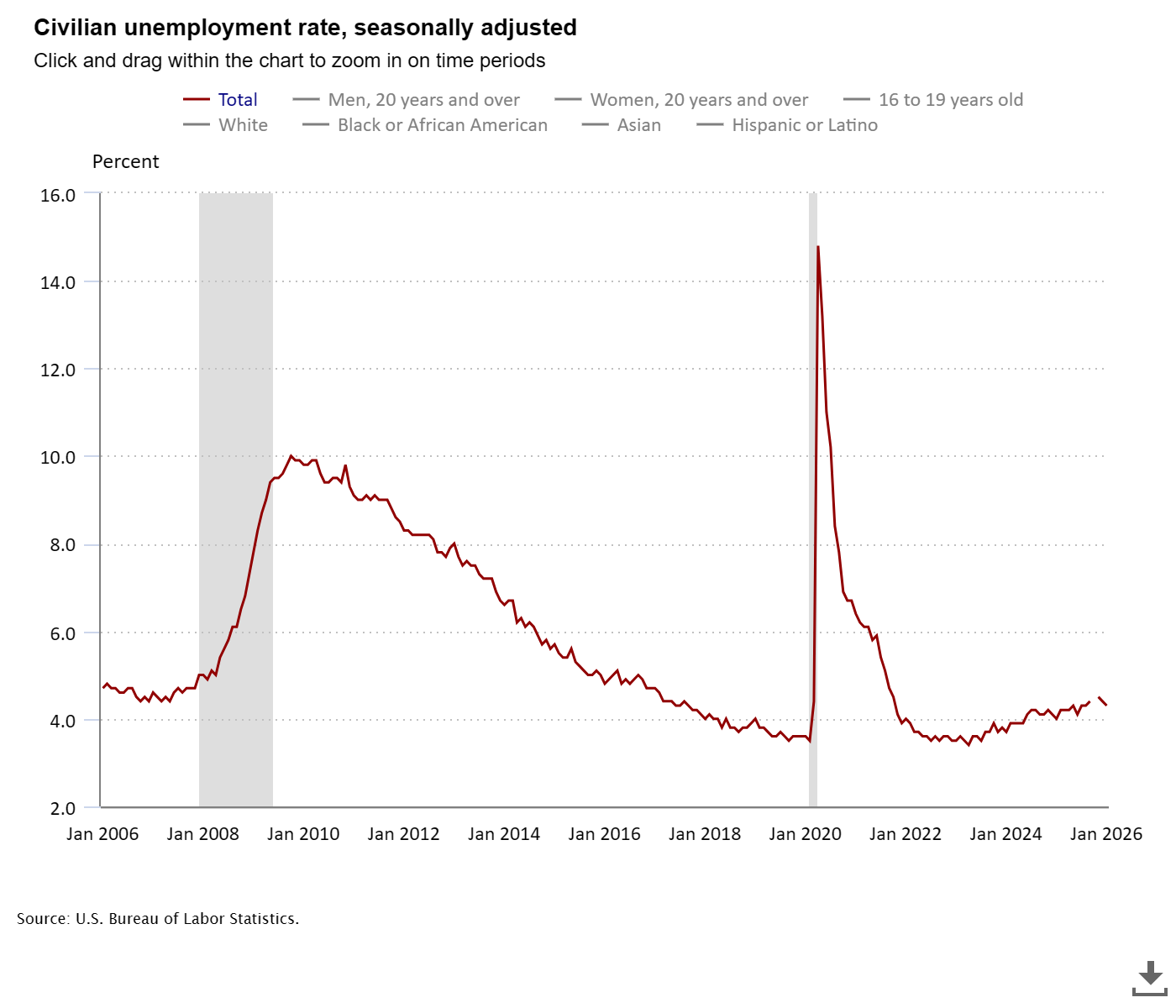

January 2026 Jobs Report: 130K Jobs Added, But Massive Revisions Reveal 2025 Was Far Weaker Than Reported

The U.S. added 130,000 jobs in January 2026 while the unemployment rate held steady at 4.3%. Health care, social assistance, and construction led gains, while federal government and financial activities cut jobs. Benchmark revisions sharply reduced 2025 job growth totals.