Tag: Economic development

-

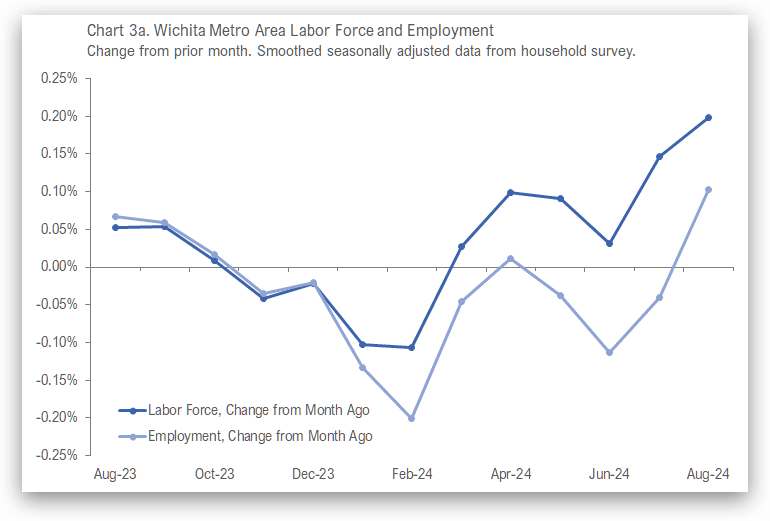

Wichita Employment Situation, August 2024

For the Wichita metropolitan area in August, most employment indicators improved slightly from the prior month. Wichita continues to perform poorly compared to its peers.

-

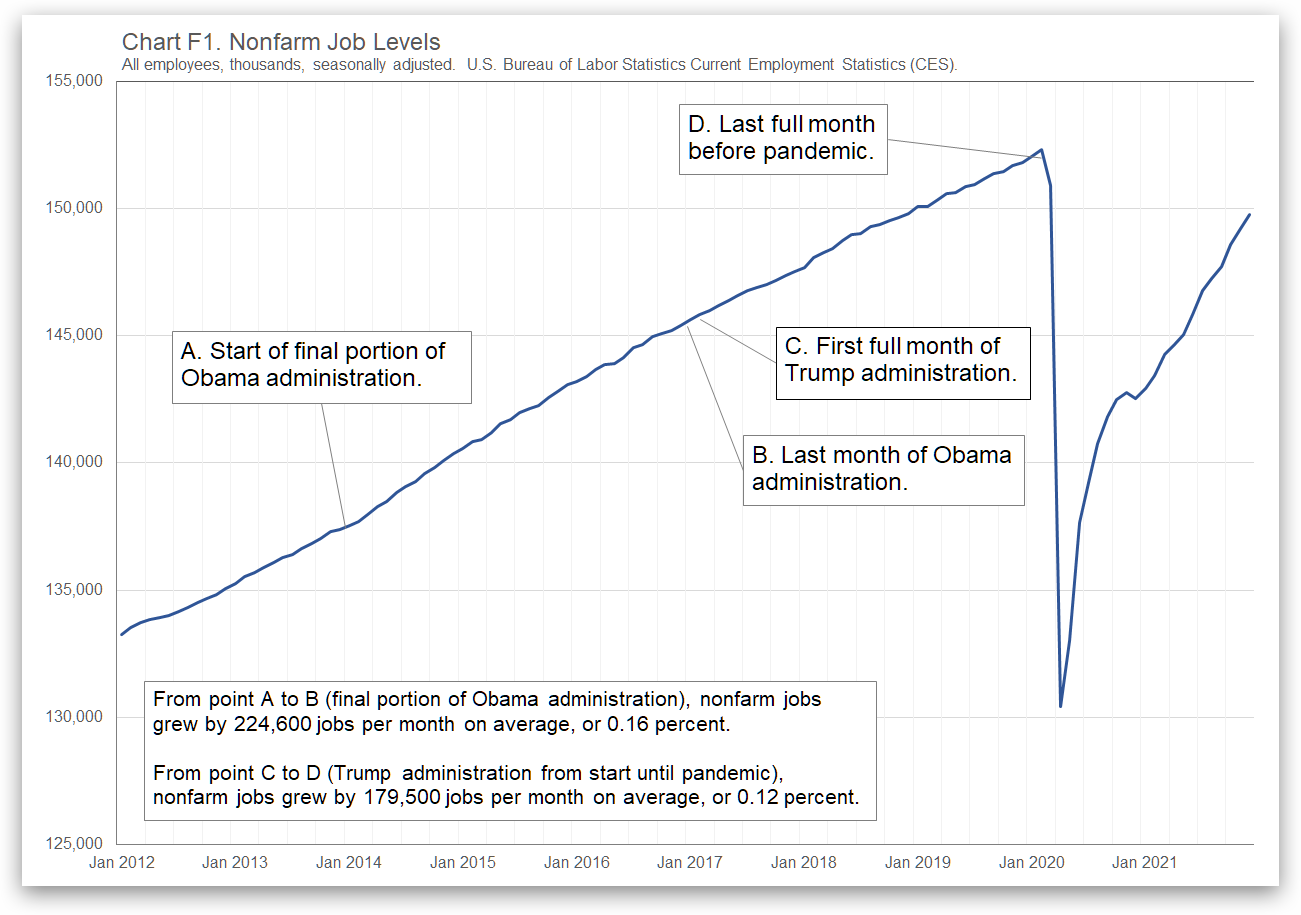

Comparing Obama and Trump Economies on Jobs

Many jobs were gained during the Trump administration until the pandemic struck. How did this growth compare to the prior administration?

-

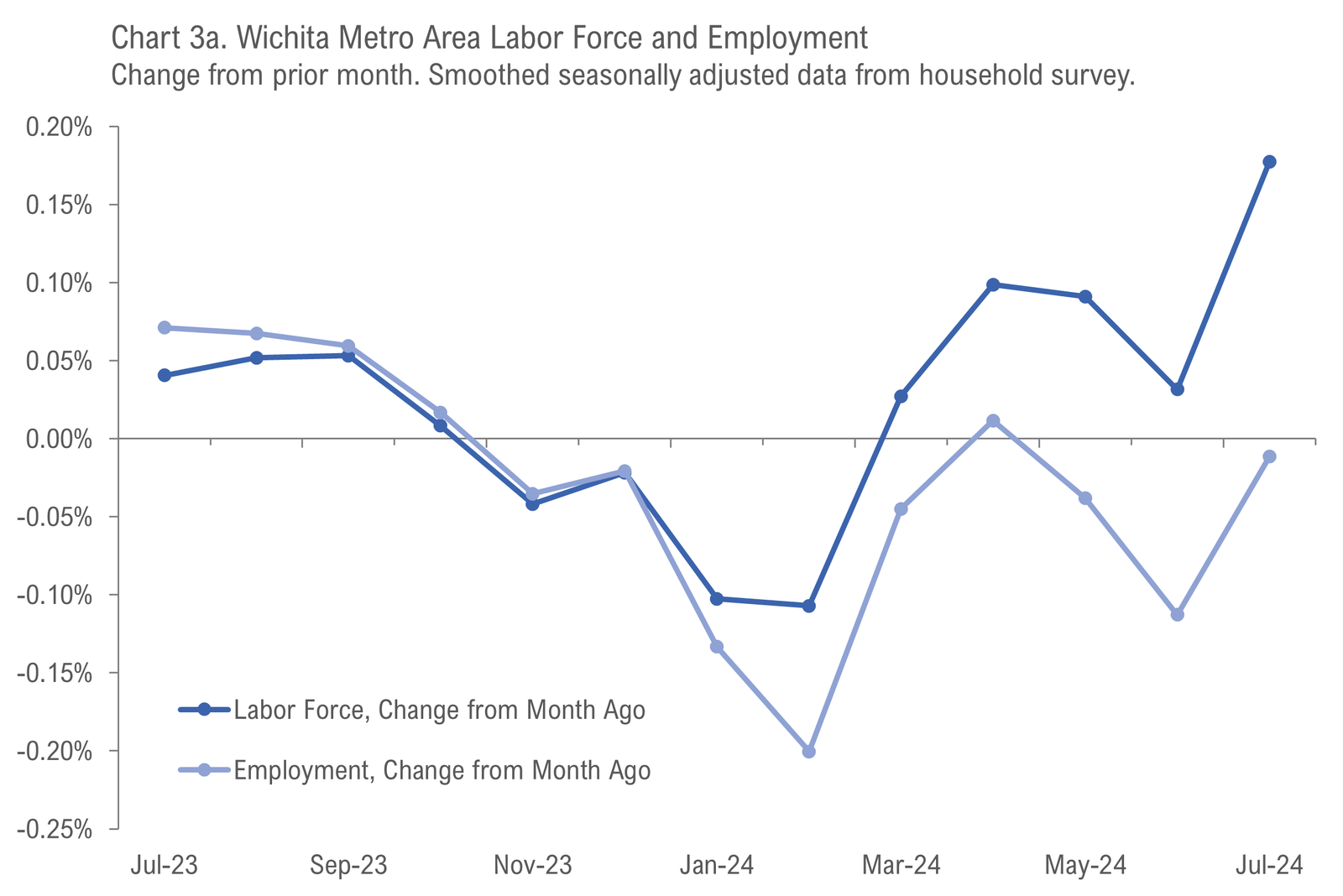

Wichita Employment Situation, July 2024

For the Wichita metropolitan area in July, most employment indicators worsened from the prior month. Wichita continues to perform poorly compared to its peers.

-

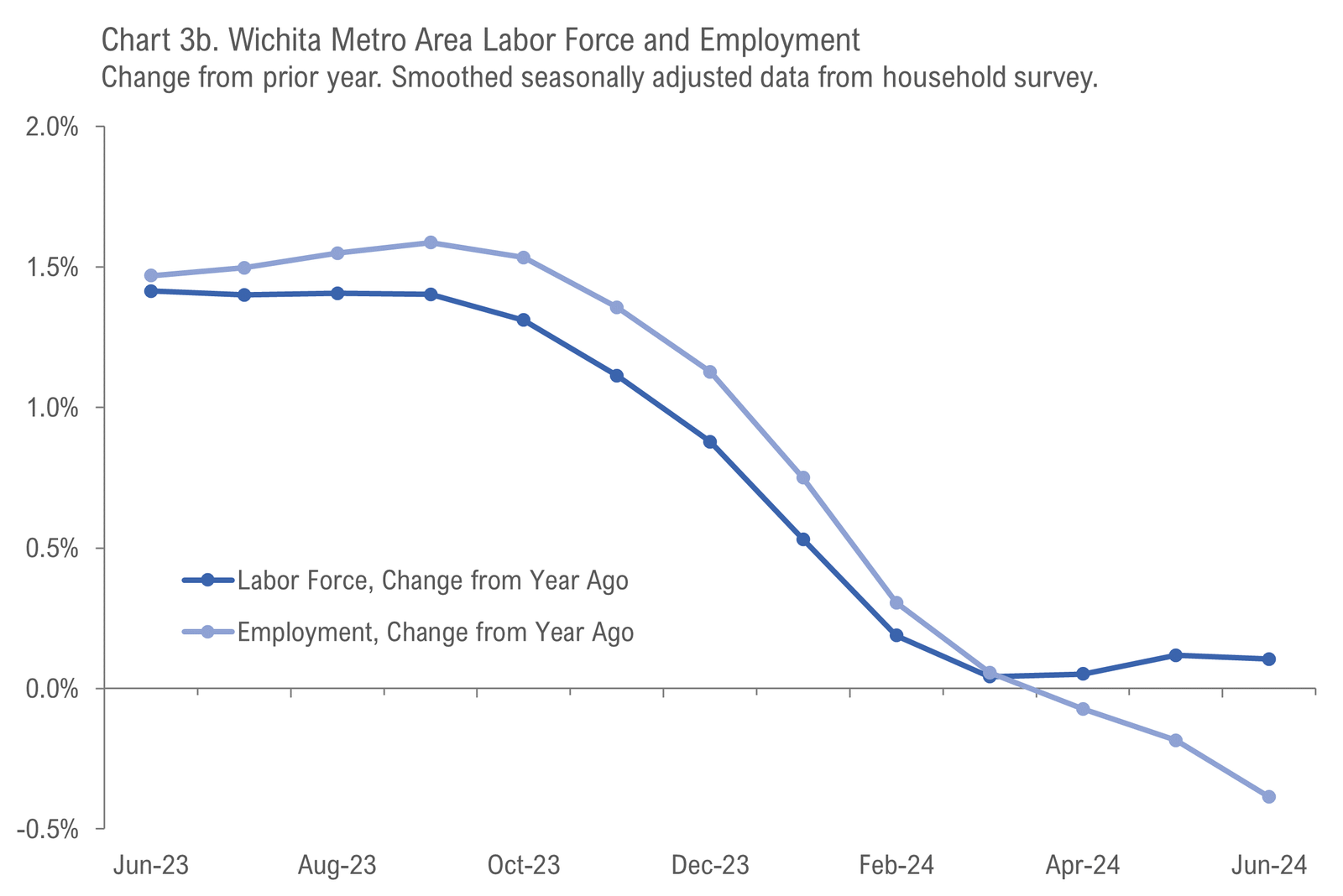

Wichita Employment Situation, June 2024

For the Wichita metropolitan area in June, most employment indicators worsened from the prior month. Wichita continues to perform poorly compared to its peers.

-

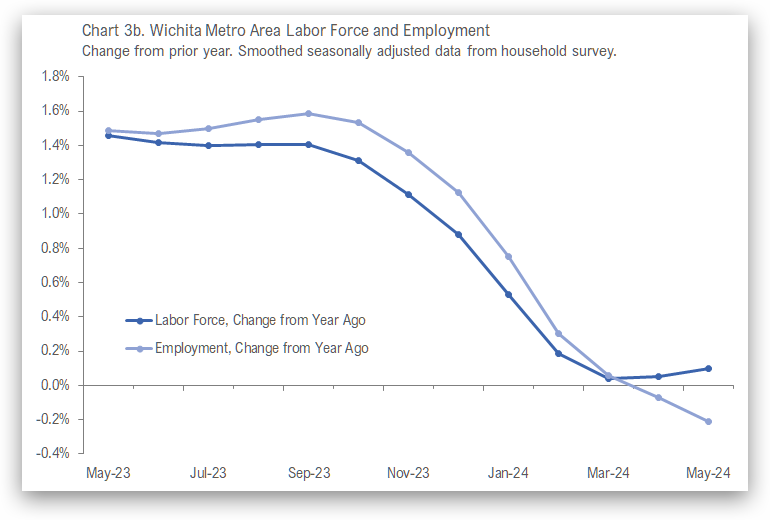

Wichita Employment Situation, May 2024

For the Wichita metropolitan area in May, most employment indicators changed only slightly from the prior month. Wichita continues to perform poorly compared to its peers.

-

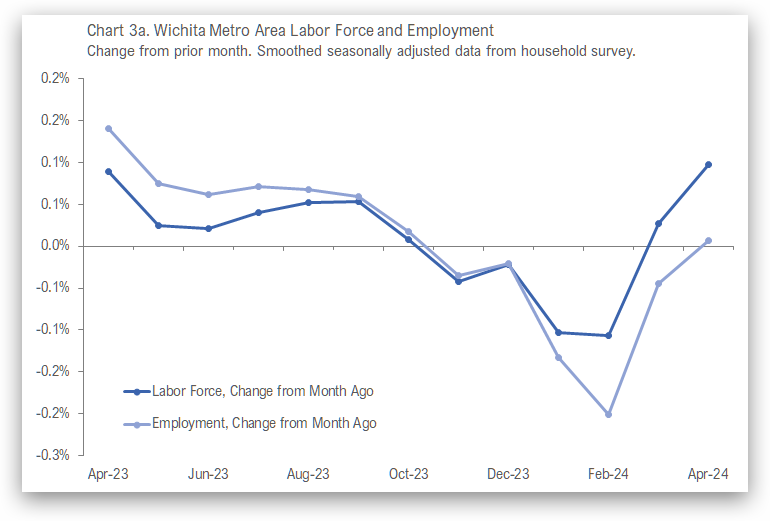

Wichita Employment Situation, April 2024

For the Wichita metropolitan area in April 2024, most employment indicators changed only slightly from the prior month. Wichita continues to perform poorly compared to its peers.

-

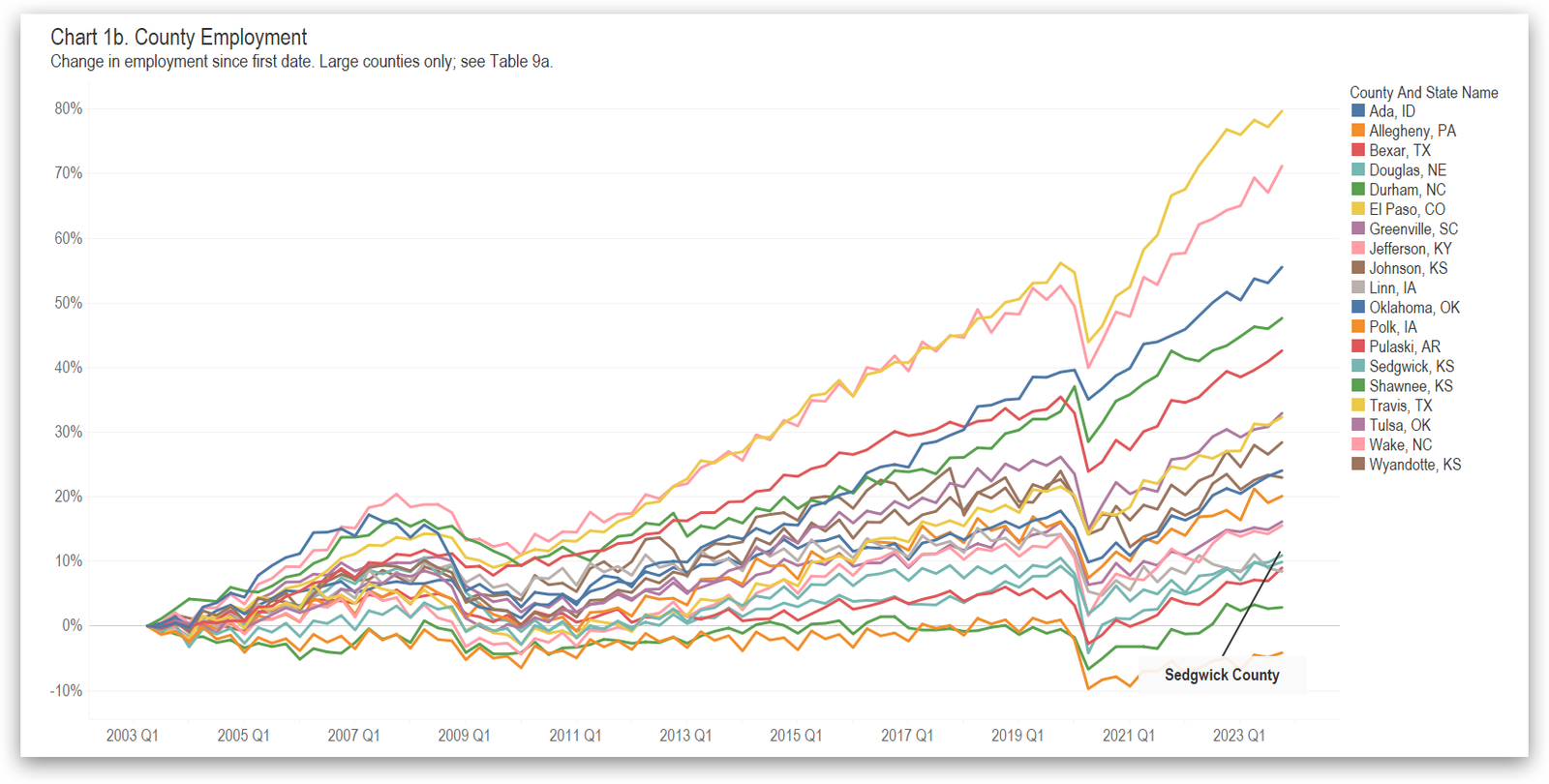

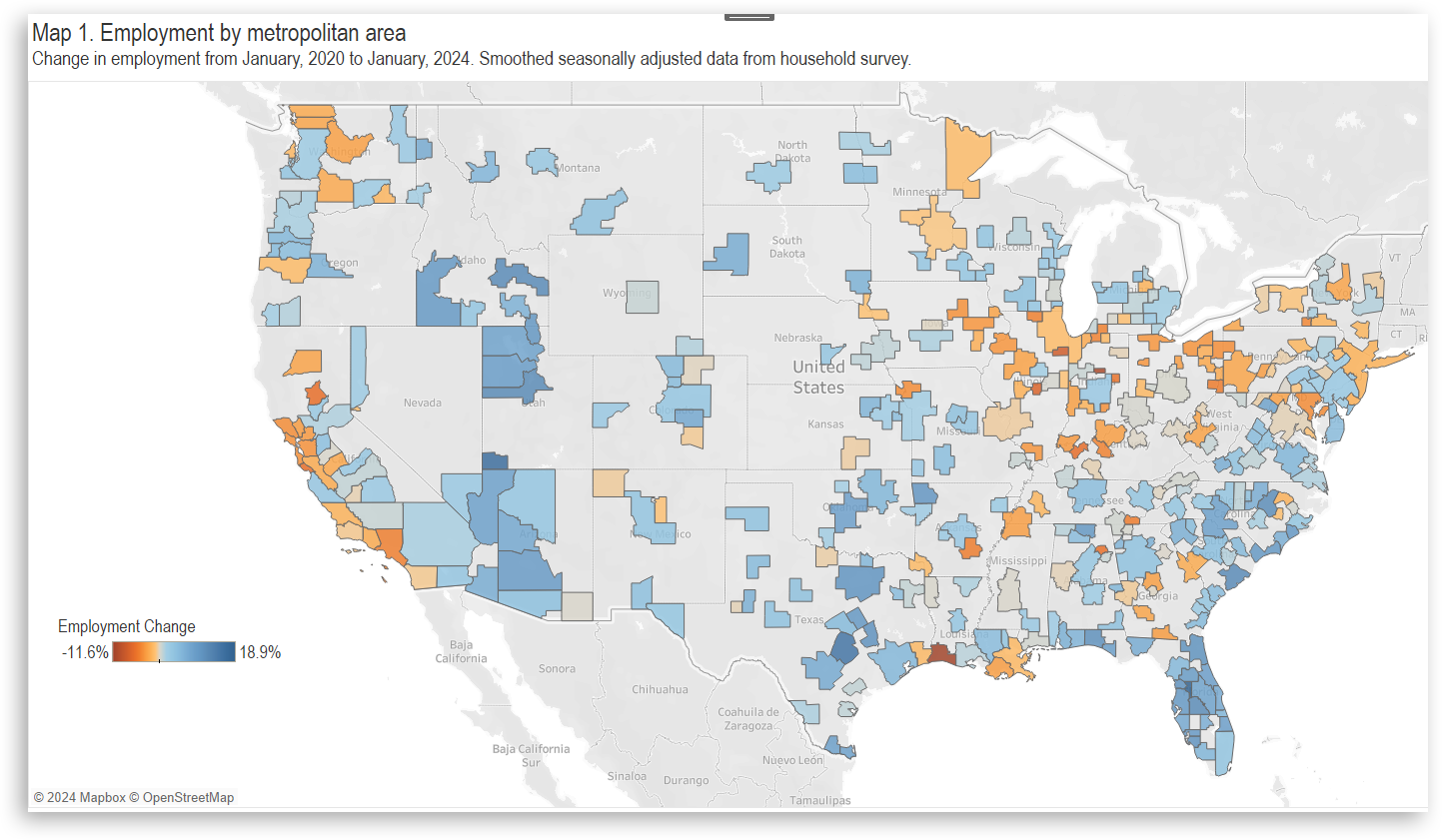

Large County Employment, Fourth Quarter 2023

Employment in large counties, including Sedgwick County and others of interest.

-

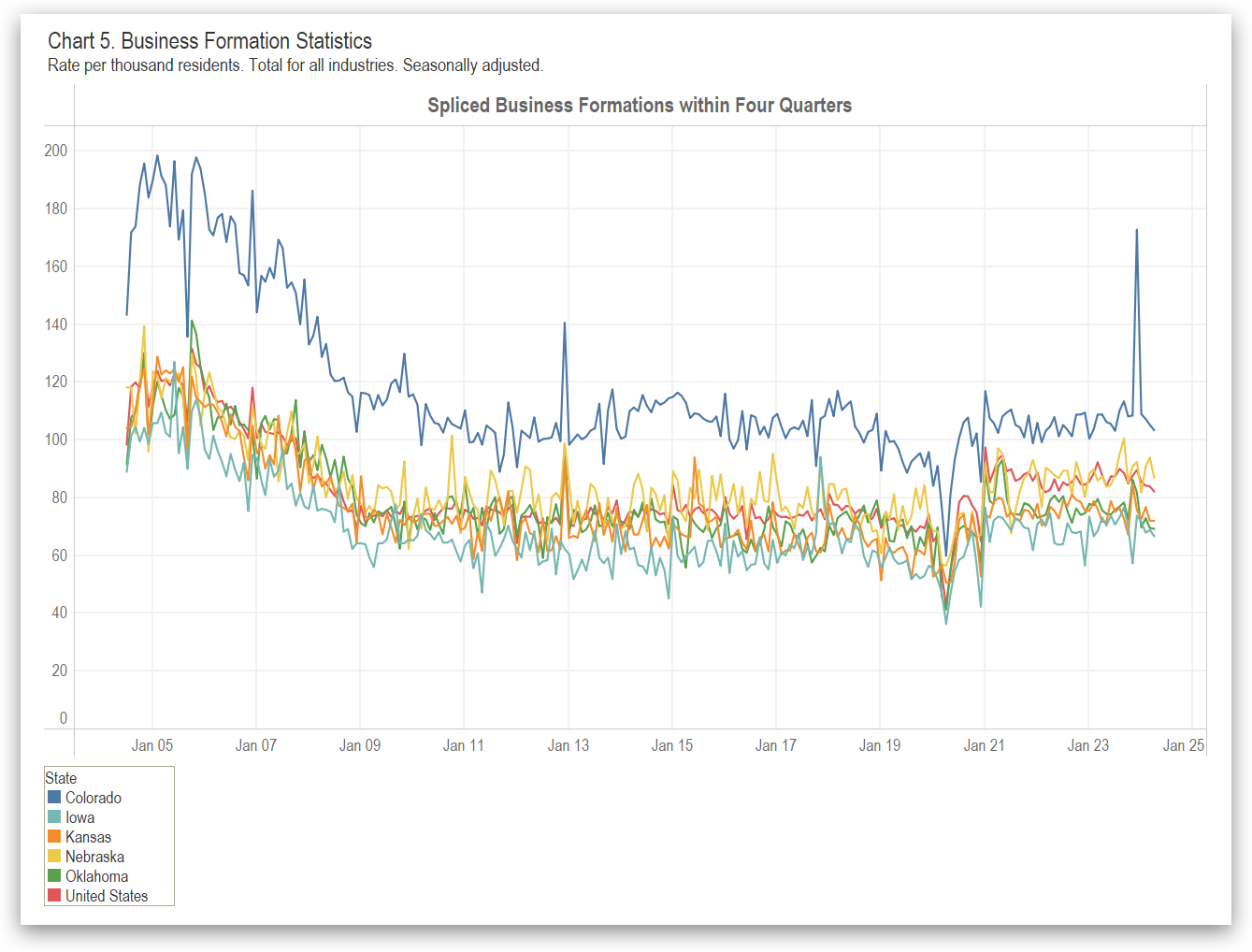

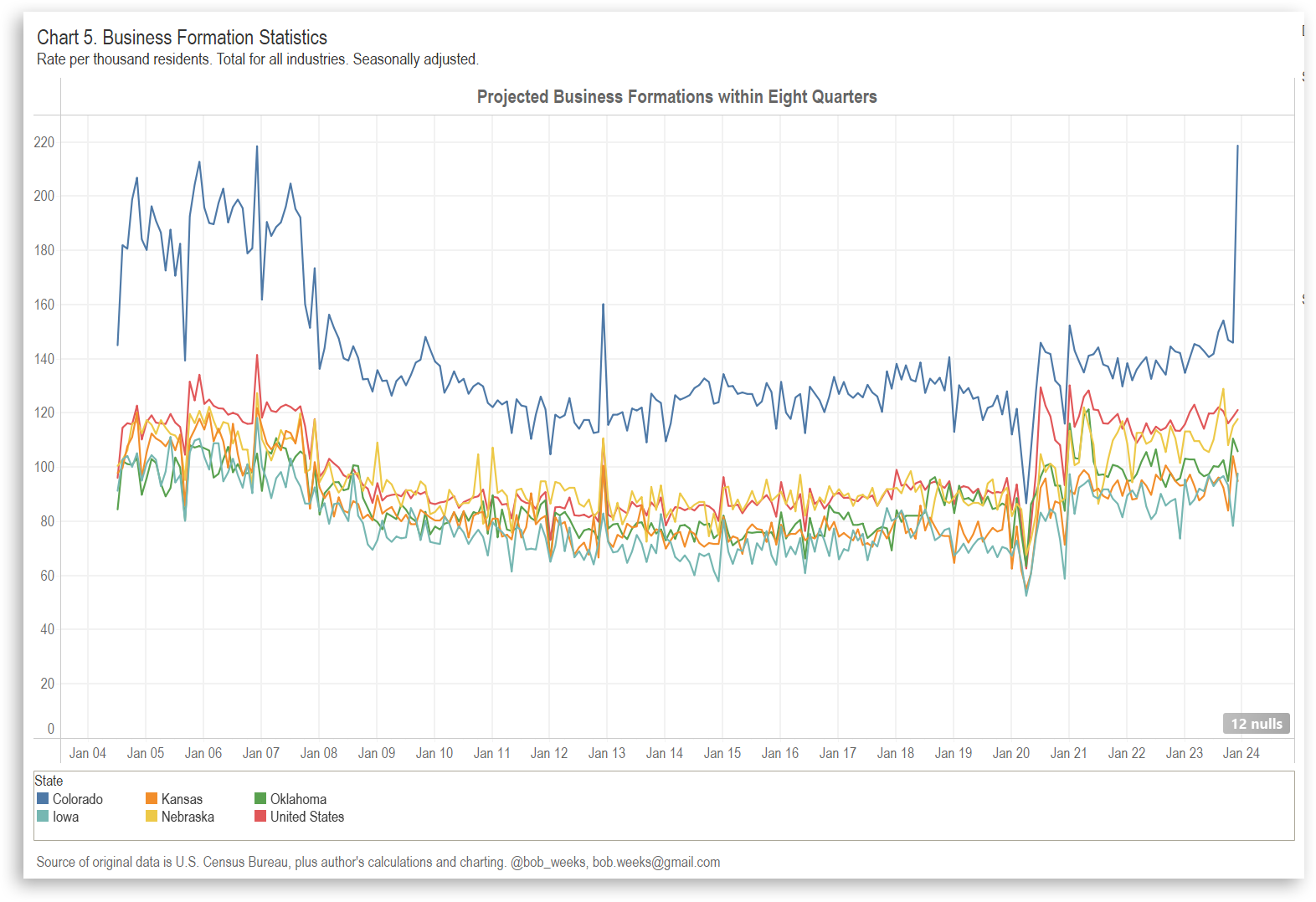

Business Formation in States

For both business applications and business formations, Kansas does better than some states, but lags many states and the nation.

-

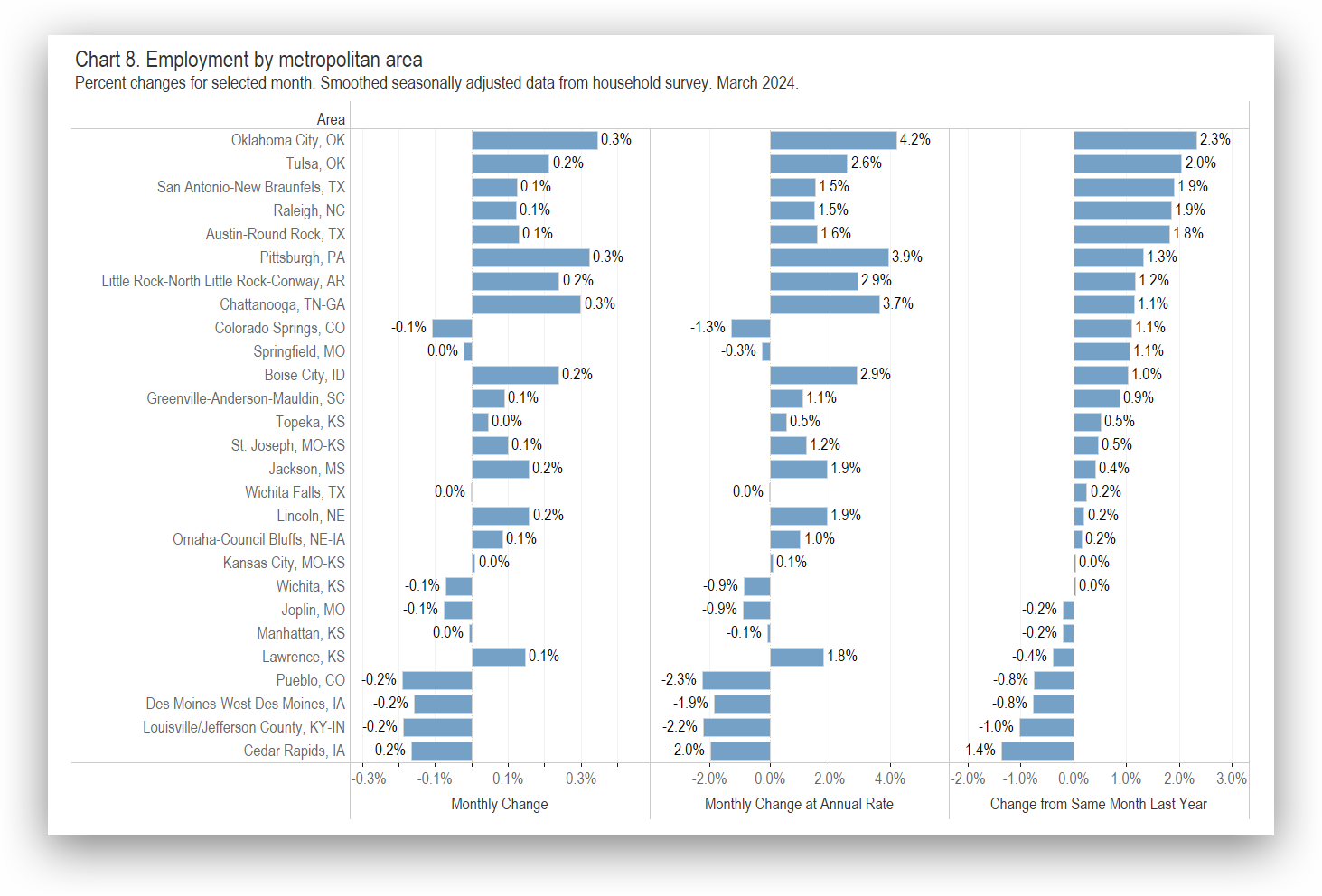

Wichita Employment Situation, March 2024

For the Wichita metropolitan area in March 2024, most employment indicators changed only slightly from the prior month. Wichita continues to perform poorly compared to its peers.

-

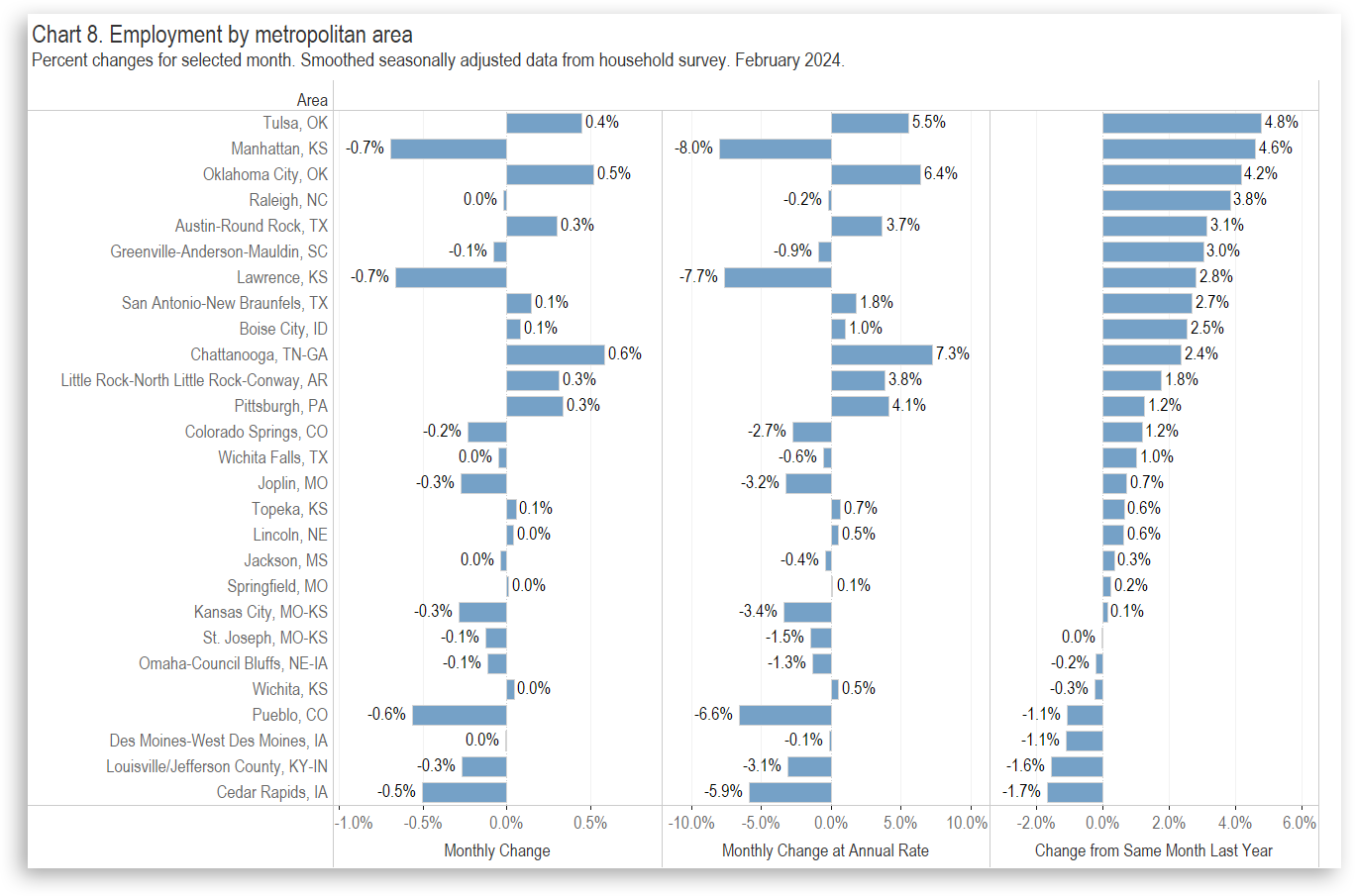

Wichita Employment Situation, February 2024

For the Wichita metropolitan area in February 2024, most employment indicators changed only slightly from the prior month, and the unemployment rate did not change. Wichita continues to perform poorly compared to its peers.

-

Wichita Employment Situation, January 2024

For the Wichita metropolitan area in January 2024, most employment indicators declined slightly from the prior month, and the unemployment rate did not change. Wichita continues to perform poorly compared to its peers.

-

Business Formation in States

For both business applications and business formations, Kansas does better than some states, but lags many states and the nation.