-

Trump’s Defamation Suit Against the Wall Street Journal Survives — But Just Barely

Read more: Trump’s Defamation Suit Against the Wall Street Journal Survives — But Just BarelyThe ruling is a split decision: the case survives, but just barely, and only on a conditional basis.

-

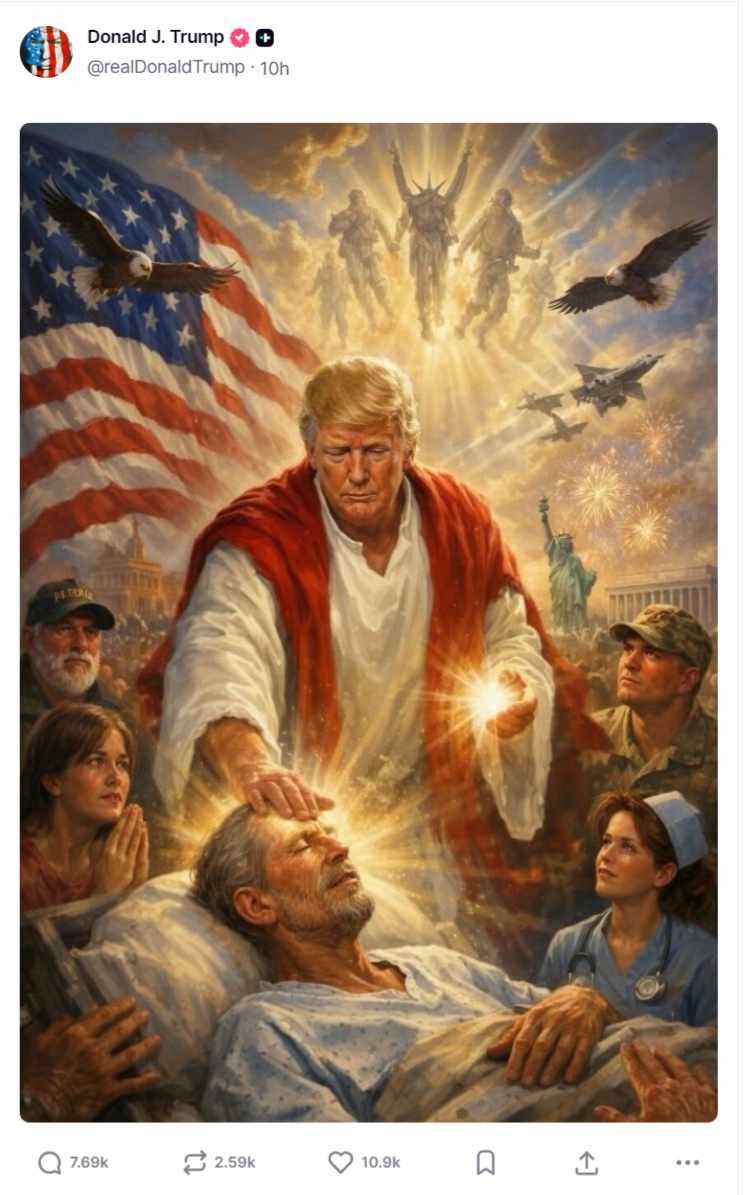

Trump as Jesus: A Visual Rhetoric and Psychological Analysis of the AI Messiah Image

Read more: Trump as Jesus: A Visual Rhetoric and Psychological Analysis of the AI Messiah ImageWhen a sitting president posts an AI-generated image depicting himself as Jesus Christ performing miracles, it warrants more than outrage. This analysis breaks down the visual semiotics, psychological patterns, and influence strategies embedded in the image — and why the sacralization of political authority is the detail that matters most.

-

Wichita City Council November 6, 2025: Lodging Licenses, Foster Youth Housing, and Event Center Capacity

Read more: Wichita City Council November 6, 2025: Lodging Licenses, Foster Youth Housing, and Event Center CapacityThe Wichita City Council met November 6, 2025, passing a new lodging establishment license ordinance targeting problem motels on South Broadway, deferring a foster youth housing project using shipping containers, and approving a modified event center capacity amendment at 3207 East Douglas. Full coverage inside.

-

Wichita City Council March 24, 2026: Road Project $3.9M Over Budget, Board Appointments, and Civility Resolution Proposed

Read more: Wichita City Council March 24, 2026: Road Project $3.9M Over Budget, Board Appointments, and Civility Resolution ProposedThe Wichita City Council met March 24, 2026, debating a 143rd Street reconstruction project that came in $3.92 million over budget with only one bidder. The council approved it 5-2 over Mayor Wu’s objection, made dozens of civic board appointments, and discussed a proposed civility resolution. #ICT

-

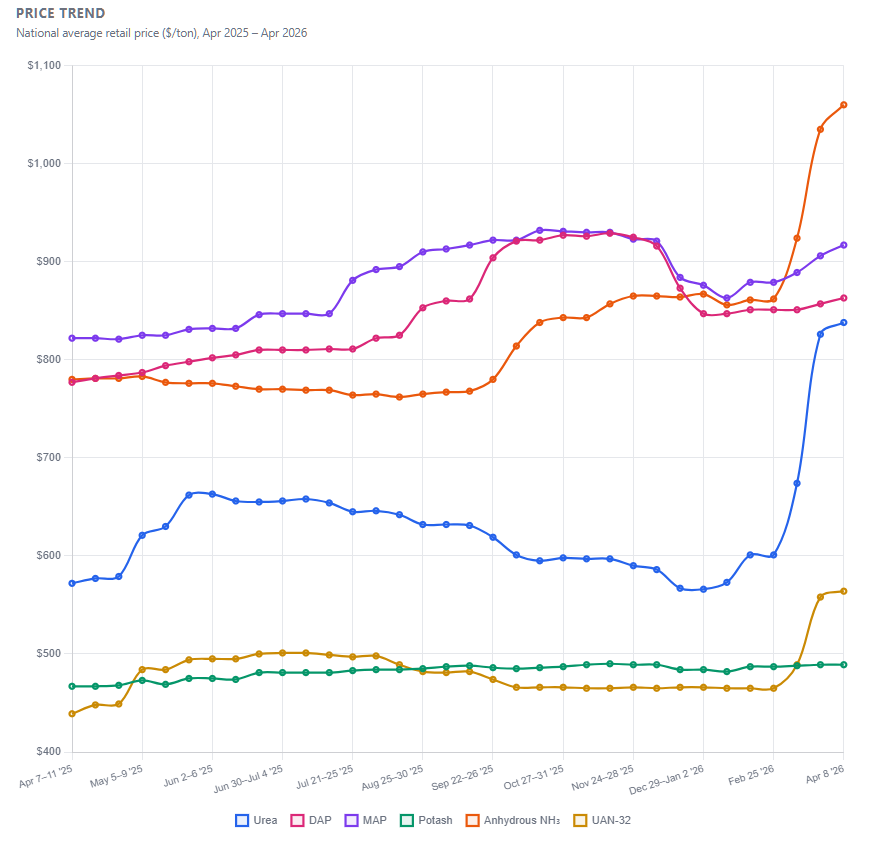

US Fertilizer Price Dashboard

Read more: US Fertilizer Price DashboardUS Fertilizer Price Dashboar

-

Trump’s 2026 State of the Union: Psychological & Rhetorical Analysis of Influence Techniques

Read more: Trump’s 2026 State of the Union: Psychological & Rhetorical Analysis of Influence TechniquesA systematic psychological and rhetorical analysis of Trump’s February 2026 State of the Union address, examining personality patterns, cognitive framing, victim testimony as persuasion infrastructure, and influence techniques targeting core audience psychological needs.

-

Melania Trump Denies Epstein Ties, Calls for Congressional Hearings in Unscheduled April 2026 Remarks

Read more: Melania Trump Denies Epstein Ties, Calls for Congressional Hearings in Unscheduled April 2026 RemarksIn unscheduled remarks on April 9, 2026, Melania Trump categorically denied any relationship with Jeffrey Epstein or Ghislaine Maxwell, cited legal victories against named accusers, and called on Congress to hold public hearings for Epstein’s surviving victims. Full transcript included.

-

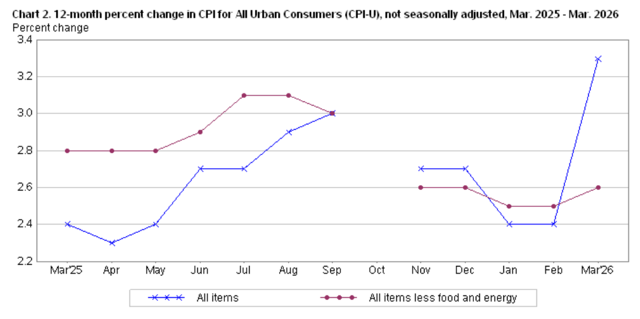

Inflation Surged in March 2026 as Gasoline Prices Drove the Biggest Monthly Jump in Nearly Four Years

Read more: Inflation Surged in March 2026 as Gasoline Prices Drove the Biggest Monthly Jump in Nearly Four YearsInflation surged 0.9% in March — the biggest monthly jump since June 2022 — as gasoline prices posted their largest single-month increase on record. The annual rate climbed to 3.3%, well above February’s 2.4%.

-

Fact-Check: Karoline Leavitt White House Press Briefing — April 8, 2026

Read more: Fact-Check: Karoline Leavitt White House Press Briefing — April 8, 2026Most of Leavitt’s specific factual claims are accurate or consistent with official government records, but several involve significant overstatement, contested framing, or assertions that cannot be independently verified outside government sources.

-

FACT-CHECK: JD Vance & Viktor Orbán — Budapest Political Rally, April 7, 2026

Read more: FACT-CHECK: JD Vance & Viktor Orbán — Budapest Political Rally, April 7, 2026VP JD Vance appeared alongside Hungarian PM Viktor Orbán at a Budapest rally just two days before Hungary’s parliamentary elections — with President Trump phoning in live to endorse Orbán before 5,000 supporters. Transcript, key quotes, and fact-check.

-

VP Vance Rallies Alongside Hungary’s Viktor Orbán in Budapest, Calls for His Reelection Two Days Before Hungarian Vote

Read more: VP Vance Rallies Alongside Hungary’s Viktor Orbán in Budapest, Calls for His Reelection Two Days Before Hungarian VoteVP JD Vance appeared alongside Hungarian PM Viktor Orbán at a Budapest rally just two days before Hungary’s parliamentary elections — with President Trump phoning in live to endorse Orbán before 5,000 supporters. Transcript, key quotes, and fact-check.

-

FACT-CHECK: Trump White House Press Conference on Operation Epic Fury

Read more: FACT-CHECK: Trump White House Press Conference on Operation Epic FuryWe fact-checked 16 claims from Trump’s April 6 White House press conference on Operation Epic Fury. Key findings: “defeated ISIS in four weeks” is false; the JCPOA “road to a nuclear weapon” framing is disputed by experts; “ended eight wars” is exaggerated.